Portfolio Manager

• Insight

China: In pole position to be the globe’s first electrostate

China has rapidly scaled and expanded clean energy technologies and infrastructure within its borders, putting it in pole position in the race to become the world’s first electrostate.1 Meanwhile, Europe’s clean energy trajectory is in limbo and the US appears to be moving in reverse, promoting petrostate policies whose logic (and dominance) are challenged not only by climate concerns but also the need for political stability and economic growth.

Authors

Analyst

Summary

- China leads the world in electrification rates and clean technology scale-up

- China’s acceleration is grounded in energy security, costs and growth logic

- In comparison, the US’s pro-petrostate policies are volatile, costly and inefficient

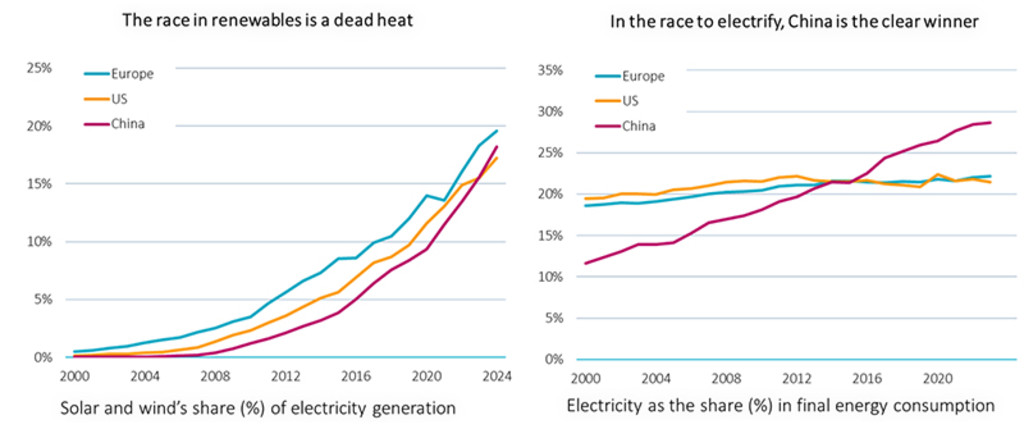

Beginning in the early 2000s, renewable power generation began rising across most major economies including Europe, the US, and China as more solar and wind capacity was added to the grid (Figure 1). While clean-energy production in these key markets continues to grow at an impressive pace, electrification rates – a measure of electricity’s share of final energy consumption – have noticeably stalled in the EU and US in sharp contrast to China where it continues to climb (Figure 2). Because electrification reflects how deeply clean electricity is penetrating end-use sectors (e.g., transport, industry and heating), it is widely regarded as a better gauge of clean energy progress.

China’s clean tech ascendancy was not initially motivated by climate change but rather economic survival. Early strategic assessments of the 1990s and early 2000s, pushed China to expand high-end manufacturing capacity, including renewables, EVs, and batteries. Energy security was also in China’s motivational mix. China is a net-importer of oil and gas leaving it vulnerable to external supply shocks from reigning petrostates. An electrified, renewable-powered economy offered a path to reduce exposure to external shocks and strengthen long-term economic competitiveness.

Figure 1 & 2 : China is surging ahead of the US and EU in the electrification of its economy

Source: Ember, IEA, 2025.

Discover emerging opportunities

For investors focused on long-term investing with real diversification, EM exposure is critical.

China’s dominance in figures

China has remained the clear global leader in energy transition investment, most recently spending USD 800 billion in 2025 (roughly 35% of USD 2.3 trillion in total global spending).2 And those investments are quickly compounding, with clean tech sectors nearly doubling in real value between 2022-25. If these sectors were a country, it would now be the eighth largest economy in the world. 3

In the first half of 2025, China made up 67% of global solar installations.4 Focusing domestically, wind and solar are on track to account for half of its installed generating capacity by the end of 2026.5 And no country comes close to China in terms of installed battery storage capacity and deployment. Given its command of battery technologies, it’s unsurprising that in 2024 nearly half of all new cars sold in China were fully electric, making it the largest domestic market for EVs. It also has the world’s largest charging network, with nearly 66% of global public chargers. 6

And China’s dominance is not just domestic; it’s also a critical global supplier of clean tech. It currently produces an estimated 70 -80% of the world’s EV battery cells and in 2024 manufactured approximately 12.4 million electric cars – accounting for over 70% of total global production.7 With 90% of battery storage applications relying on parts supplied from China, it has a power position in the battery storage supply chain. It is also the globe’s dominant manufacturer of heat pumps, producing around 40% of all units and controlling 95% of the heat pump compressor market. 8

Keep up with the latest sustainable insights

Join our newsletter to explore the trends shaping SI.

Not just cleaner but cheaper and more productive

China’s scale and vertical integration of domestic supply chains have helped it significantly reduce the cost of clean energy technologies. Solar panel prices have fallen almost 75% since 2022; wind turbine prices fell by 50% between 2022 and early 2024 (Figure 3); and battery pack prices fell by around 30% in 2024 alone. 9,10,11 Finally, China has also driven down the price of heat pumps, another critical end-use technology, such that they are now 40-60% cheaper than in the EU and US. 12

Figure 3: China is the low-cost leader in wind turbine production

Onshore wind turbine price by region.

Source: BloombergNEF, 2025.

Not only is electrification winning on economic costs, it also beats fossils when competing on pure energy productivity. Renewables avoid the massive thermal losses inherent in burning fuels, making them two to three times more efficient for producing electricity. Electric motors routinely achieve efficiencies of 80-90%, compared with roughly 20-30% for combustion engines and fossil-fuel power plants. Heat pumps deliver two to four units of useful heat per unit of electricity due to their ability to move rather than create heat, making them three to four times more efficient compared to gas boilers.13

Figure 4: Renewables and electrons are cleaner and more power-packed

Solar and wind’s 100% efficiency is based on no energy loss when converting from raw energy (primary) to secondary energy that can be practically used in end applications (e.g. heat pumps, boilers, cars and EVs). Source: RMI, (using IEA, IIASA, RMI analysis, adapted from Prof. Tomas Kaberger). 2024.

The US – leveraging petrostate power

While China accelerates renewables and electrification, current US policies are headed in reverse. Under Trump, energy and geopolitical policy have veered toward securing fossil fuel resources and protecting combustion-powered consumption. Trump has expanded oil and gas leasing, relaxed methane and power-plant emissions standards, as well as rolled back vehicle fuel efficiency standards. At the same time, Trump has used Executive Orders to prioritize US fossil fuel output and export capacity. US foreign policy has also continued to use oil supply as a geopolitical lever, most recently with the seizure of Venezuelan oil assets in January 2026.

Despite Trump’s best efforts to thwart clean energy growth, the US continues to benefit from forward-thinking energy policies of previous administrations, most notably Biden’s Inflation Reduction Act (IRA) which prompted a wave of renewable and electrification investments. These are proving critical for achieving Trump’s own objective for US leadership in AI computing and data center infrastructure – sectors that require enormous amounts of electricity. The fastest, cheapest way to meet this demand is through utility scale solar, battery storage, and modernized grid connections which is why the US EIA projects that 93% of all new-generation capacity added to the grid in 2026 will come from wind, solar and batteries. 14

Clean tech and the energy transition – environmentally, geopolitically and economically urgent

The Russia-Ukraine conflict of 2022 and the current US-Iran conflict are the latest reminders of the economic risks and instability of oil and gas markets. China recognized its economic vulnerability early and calculated that investments in renewables and electrification were the only viable way forward. As we digest energy market volatility since the start of the year, the Smart Energy strategy’s investment thesis that ‘electricity is the energy of the future’ has never been more relevant or urgent. The strategy is well positioned to benefit from intensifying energy trends impacting energy supplies as well as equally powerful trends building in energy consumption.

Its investments span the full value chain shaping the energy transition from upstream renewable power generation to transmission infrastructure and grid-scale storage. Beyond energy supplies, it also captures the shift to end-use electricity consumption through exposure to EVs and battery materials as well as electric heat pumps for heating and cooling systems. Equally significant, by investing in energy-efficient semiconductors, automation systems and power electronics, the strategy is well positioned to benefit from the mounting bottlenecks and intensifying battles for electrons as the structural shift to power-hungry AI-computing and data center buildouts accelerates. This breadth ensures the strategy benefits not only from the irrevocable rise of renewables but also from the shift to AI and the electrification of everything across the global economy as other nations follow China’s lead.

Smart Energy D EUR

- performance ytd (30-6)

- 54.65%

- Performance 3y (30-6)

- 25.47%

- morningstar (30-6)

- SFDR (30-6)

- Article 9

- Dividend Paying (30-6)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

Footnotes

1 ‘Made in China 2025,’ Center for Strategic & International Studies. June 2015.

2 Energy Transition Investment Trends 2025, BloombergNEF.

3 Center for Research on Energy and Clean Air, February 2026.

4 Ember, September 2025.

5 China’s solar power capacity on course to surpass coal this year. Bloomberg, February 2026.

6 IEA EV Outlook, 2025.

7 IEA, Global EV Outlook, 2025.

8 Is a turnaround in sight for heat pump markets?, IEA, February, 2025.

9 IEA World Energy Investment 2025

10 China solar cell exports grow in 2025. Ember, August 2025.

11 The battery industry has entered a new phase. IEA, March 2025

12 IEA World Energy Investment 2025.

13 The incredible inefficiency of the fossil energy system. RMI, June 2024.

14 Renewable energy defies Trump’s attacks, reaching a new record, Bloomberg, February 2026.