Strategist

• Monthly outlook

REITs: playing in extra time?

They’ve long been seen as defensive, since traditional bricks and mortar can usually survive any downturn. But investors should be cautious about relying on Real Estate Investment Trusts (REITs) if the current macro headwinds lead to a recession, says strategist Peter van der Welle.

Authors

Top keywords

Summary

- REITS are a widely favored cash-generative defensive play

- Headwinds range from Ukraine war to Fed monetary tightening

- Sweet spot has passed but still some upside amid high inflation

REITS – a form of mutual fund which invests in anything from shopping malls and skyscrapers to new housing projects – are a perennial favorite among more defensively minded investors. Not only are they backed by real estate infrastructure, they also generate reliable rental streams.

However, the recent perfect storm of significantly higher inflation, rate hikes and quantitative tightening combined with geopolitical factors led by the war in Ukraine call for a more cautious approach, says Van der Welle, strategist with the Robeco multi-asset team.

“Although macroeconomic data releases in developing economies have remained overall positive compared to prior expectations, a growth scare has been building lately, as risks that could derail this expansion further down the road are easy to spot,” he says.

“This sentiment shift is evidenced by steep downgrades for 2022 global real GDP growth by official institutions such as the IMF and World Bank, which downgraded real GDP growth forecasts to 3.6% and 3.2% respectively. It can also be seen in the latest fund manager survey by the Bank of America Merrill Lynch which saw a steep rise in growth pessimism to levels last seen during the global financial crisis.”

“While we expect the current economic expansion to continue for another 6-12 months, since the US Federal Reserve has not yet entered excess liquidity tightening territory and household cash piles as well as developed market corporate balance sheets look pretty decent, we acknowledge that the risks to our base case are tilted to the downside.”

Van der Welle cites four reasons why economic deterioration may creep up on investors. “Firstly, as the conflict in Ukraine drags on, the elevated probability of a fully-fledged EU boycott of Russian energy leaves a fat tail risk of an immediate Eurozone recession,” he says.

“Secondly, central bankers have gotten their wake-up call as inflation has kept on surprising to the upside in both its speed and breadth. Forthcoming aggressive monetary tightening by the Fed to catch up with (cyclical) inflation pressures could deteriorate financial conditions and cause a further derating of asset prices beyond what is warranted by a typical mid-cycle correction.”

“Thirdly, a very flat Treasury yield curve signals that we are approaching the slowdown phase of the business cycle, with peak corporate pricing power around the corner, as the ability to raise net selling prices is outpaced by stubborn input cost rises.”

“Lastly, the recent growth slowdown in China on the back of elevated lockdown intensity in key manufacturing hubs could have global growth repercussions in the next few quarters, either via supply chain disruptions or through renminbi depreciation.”

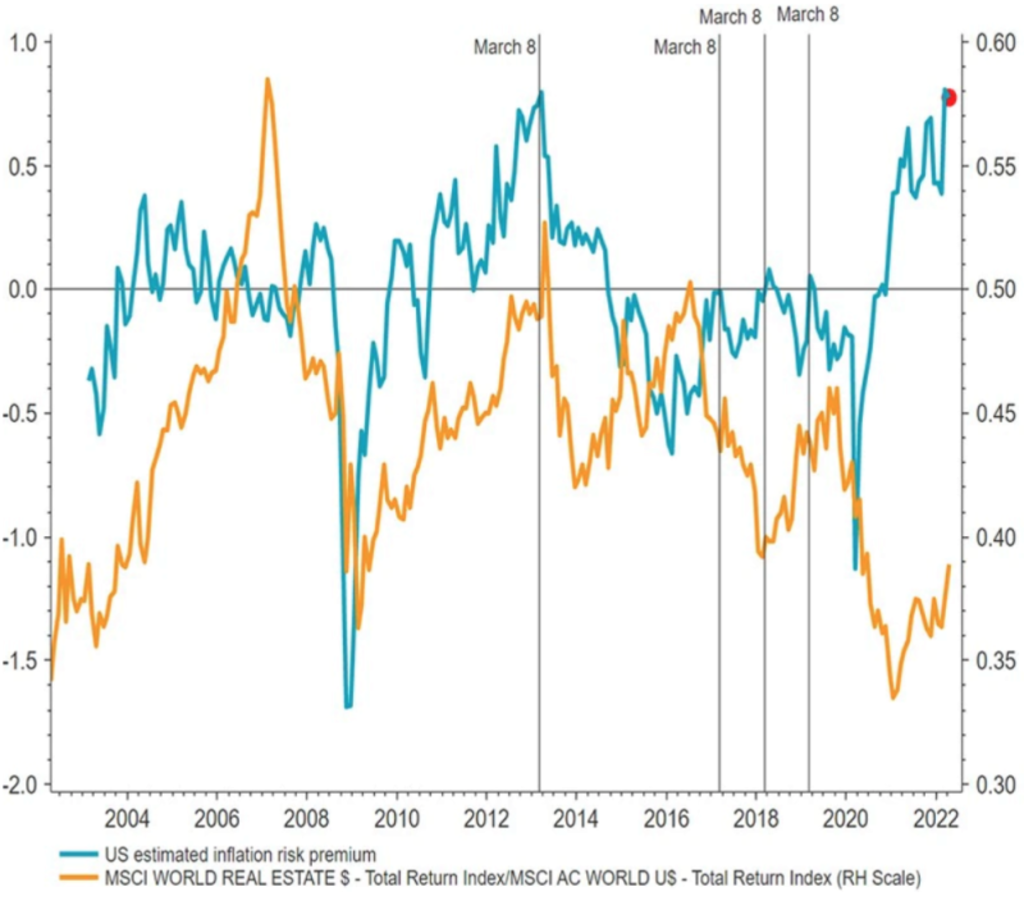

Recent REITs performance has lagged the higher inflation risk premium demanded in bond markets

Source: Refinitiv Datastream, Robeco

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Paving the way for de-risking

So, how to navigate these risks? “The current growth scare could pave the way to profit taking and/or de-risking as well as the quest for enhanced diversification among investors as the tide of excess liquidity recedes just as equity seasonality turns negative,” Van der Welle says.

“In addition, as the ‘there is no alternative’ (TINA) narrative starts to be challenged by the recent surge in sovereign yields, investors are likely to tactically shift down the risk curve. They’ll start looking for asset classes that have a lower beta (relative risk versus the index they follow) but which still offer decent excess return potential over Treasuries, so long as the expansion remains on track.”

“Indeed, we already note that momentum in the last month has shifted to sectors with defensive characteristics such as consumer staples, health care, utilities, and especially REITs. In addition, investors are on the lookout for assets that can maintain their pricing power as inflation likely transitions towards a key inflection point in the second half of 2022.”

The sweet spot has passed

Are REITS still a ‘safe bet’ then? “The sweet spot for REITs’ performance has passed, in our view, though as long as the stagflationary twist in the current macro environment does not culminate in the outright contraction of real activity, there is still some juice left in the asset class,” Van der Welle says.

“A growth/inflation mix of decelerating activity momentum during economic expansion and inflation running above 3% (the composition we anticipate in the next 6-12 months) typically sees REITs outperform global equities.”

“This return pattern confirms the consensus view that REITs are a more defensive play, with inflation-hedging capabilities. Yet, judging from the significant positive correlation with the relative performance of cyclicals compared to defensives, REITs behave more like a cyclical asset in practice. They therefore have a high beta to economic activity, which leaves them vulnerable to economic contractions, especially those that morph into recessions.”

The threat of rising rates

Another issue is that most real estate relies on funding – from common mortgages to the corporate bonds issued to build shopping malls or skyscrapers – and interest rates are rising.

“While financing costs are expected to increase for the asset class, we judge that this will be a more gradual process,” says Van der Welle.

“The extension of debt maturities during the recent years of exceptionally low interest rates have lowered REITs’ susceptibility to a sudden surge in financing costs. And their ability to weather a higher interest burden in the near term is still there, given their decent underlying cashflow generation.”

“Global REITs’ leverage is currently not excessive: the net debt to equity ratio is 0.85. Moreover, their ability to service a rising debt burden is currently strong, with an interest coverage ratio of 4.5. Looking at standalone valuation metrics like the discount to net asset value, the asset class is fairly valued.”