Head of Conservative Equities and Chief Quant Strategist

獲取最新市場觀點

訂閱我們的電子報,時刻把握投資資訊和專家分析。

Conventional wisdom has it that long-term outperformance is often a matter of limiting losses in down markets. One way conservative investors seek to mitigate losses in down markets is to keep a part of their portfolio in gold. But is this really the most effective strategy? Our research shows there are alternative options available.

Warren Buffet’s first rule of investing is to never lose money; his second is to never forget the first rule. This golden rule is key for long-term capital protection and growth. One oft-used strategy to limit losses in turbulent markets is an allocation to gold. Gold investing is widely regarded as a safe haven during extreme macroeconomic downturns in periods of war, hyperinflation, or major recessions.

But do such allocations to gold really provide the expected protection in practice? And even if so, are there any better ways to mitigate risks? To answer these questions, we revisited the strategic role of gold in investment portfolios and focused on its marginal downside risk reduction benefits relative to bonds and equities.

Our analysis, featured in a new research paper, focuses on annual real returns starting in 1975, when gold became truly tradeable. We took the perspective of a US investor who could strategically invest in equities, bonds, and gold and would care about a wide range of downside risk measures, including downside volatility, loss probability and expected loss.

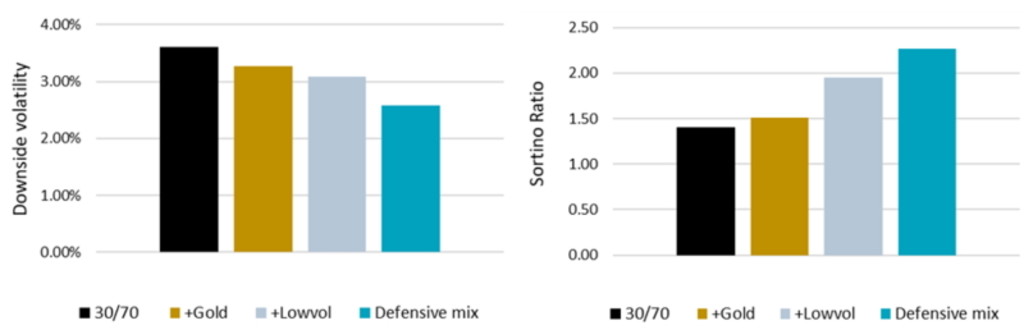

The key findings of our empirical study are that a modest gold allocation in a traditional mix of equities and bonds reduces the risk of capital losses by around 10% across a wide range of equity-bond allocations. Still, this also reduces the return, leading to a small increase in the return/risk ratio as shown in Figure 1 summarizing the main findings of this study.

Source: Lohre, H., and Van Vliet, P. (2023) “The golden rule of investing”, working paper.

訂閱我們的電子報,時刻把握投資資訊和專家分析。

Importantly, however, our simulations show that the downside volatility can be reduced further by adopting a low volatility style in the equity investment and letting this defensive equity allocation replace part of the bond allocation. The portfolio with the lowest downside volatility on a one-year horizon consists of 45% bonds, 45% low-volatility stocks and 10% gold.

Our simulations show that the downside volatility can be reduced further by adopting a low volatility style

As a result, this defensive mix has significantly lower downside risk than a traditional equities/bonds portfolio, with higher returns leading to a large increase in the Sortino ratio. This defensive strategy therefore proves to be an effective way for investors to adhere to Buffet’s golden rule, while still delivering long-term capital growth.

Moreover, additional simulations and robustness checks show that these key findings hold not just for the one-year returns initially considered, but also for a wide range of investment horizons, ranging from one month up to 36 months. While these results are robust when gold futures are used instead of a direct gold investment, adding gold mining stocks is less effective in reducing the downside risk of a low-volatility equity portfolio. Lastly, we document that, while the risk mitigation role of gold is muted in a mean-variance setup, low volatility investing is considered just as relevant as when evaluated through a downside risk lens.

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。