Head of Multi Asset & Equity Solutions, Co-Head Investment Solutions

• Insight

Markets are a voting machine, investing is a weighing machine

Weighing up the long view has never been more important as turbulence continues to hit markets, says multi-asset investor Colin Graham.

Authors

Equities have plummeted in recent weeks on the perfect storm of the Ukraine conflict, record inflation that has caused central banks to raise rates higher than was expected, and new outbreaks of Covid-19 that led to lockdowns in China.

Investors would therefore do well to remember a famous quote that “In the short term the stock market behaves like a voting machine, but in the long term it acts as a weighing machine", says Graham, Head of Multi-Asset Strategies at Robeco.

The phrase was coined by his namesake, the British economist Benjamin Graham, who is considered the father of value investing and was once the boss of Warren Buffett. It means that in the short run, the market votes on which firms are popular and sends stock prices up and down accordingly. But in the long run, the market has to assess the underlying fundamentals of a company to give its true weight, or value.

Voting or weighing?

Graphic by Robeco, May 2022

“From our vantage point, the future is more uncertain now than it's been for many years,” Robeco’s Graham says. “Therefore, we've got to really dig down deep into our investment decisions and think about what we're doing, but also try and step away from the day-to-day noise around a lot of the movements in markets.”

“We need to really think about what is the outlook, and where are we going to be towards the end of this year and the beginning of next year?”

“At the end of March, the multi-asset team had positions on long equity, short duration, short spread, long dollar and slightly non-cash as a balancing item. And what we've done is basically take off the positions in short duration, the spread and the dollar. So we have very few active positions on at the moment, reducing the risks while we assess the opportunities.”

The short-term turbulence was clearly seen in the second week of May, in which the S&P 500 Index went up by 4% on one day, went down by 5% on another, and ended the week flat. This is clear voting machine territory, and it is set to continue, Graham says.

The genie has escaped

“Monetary policy is still tightening – we’ve seen 75 basis points of rises in the US, rates also raised in Australia and the UK, and at various other central banks as well,” he says.

“The inflation genie has escaped and we're starting to see the second-round effects in higher wage demands, which for me is where the red lights are starting to flash, because this means that the inflation is getting embedded and you need a much bigger slowdown to contain it.”

“On the other side of the scales, we are already seeing a drag on aggregate demand through rising commodity prices and a much stronger US dollar, and tightening financial conditions for the consumer.”

“And we're also seeing a second trade recession emanating from China's lockdown. China’s PMIs and Services surveys are below 50, signaling a contraction, which is going to cause problems for emerging markets. So, if you think about it from a voting machine perspective, then it's pretty much negative territory at the moment.”

Weighing it all up

This is where the weighing machine can start to kick in. “Looking out over the next 12 months, growth will be slower, but it's still going to be positive,” Graham says. “We think that fiscal support will remain in Europe and in China.”

“Corporate earnings are still delivering while monetary policy remains accommodative, and so we shouldn't forget that central banks have the tools to control inflation. This is one of the key elements. If we start to see a topping out of inflation, we’ll see a much calmer market.”

“Other economies are still opening up. We think that the US consumer and corporate balance sheets are in very good shape and the recession indicators are still pretty low for the next 12 months. So on balance, we think that things are still positive from a weighing machine perspective; the data, rather than the surveys, are telling you that actually things are OK.”

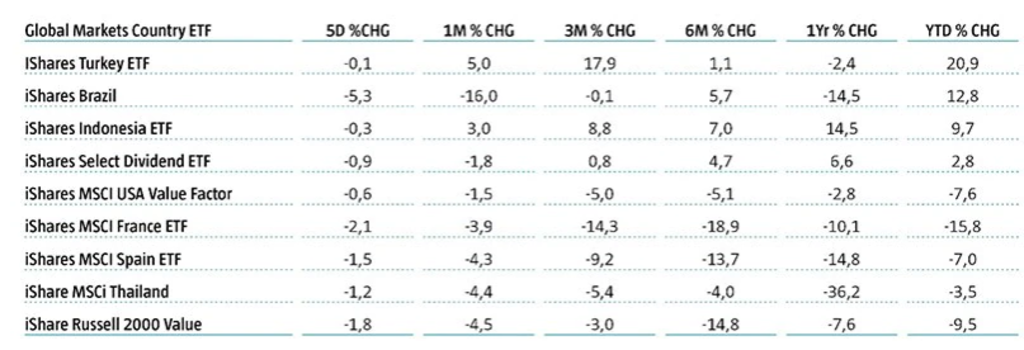

Take a bow, Turkey

And from a multi-asset perspective, Graham says turbulent market conditions often produce some surprising winners. The best-performing equity market in 2022 so far has been… Turkey.

“If anyone had asked at the start of the year that Turkey was going to be the best performing equity market at any point this year, I don't think many people would have said ‘yes’,” he says. So we have to remember that when things get sold off, they do bounce back, even if nothing else changes.”

And the prize for the best-performing market so far this year goes to… Turkey

Source: Refinitiv, Robeco May 2022

Going platinum

“South Africa is another interesting one, given their metals output and their position as one of the world’s largest exporters or platinum and palladium. Since Russia is also a significant exporter of both precious metals, but is now subject to sanctions, you can see how demand for minerals from South Africa has suddenly gone up. That's one definitely one to watch over the next three to six months.”

“We do though need to see some more calm in the credit markets in order to feel more confident about the equity markets as well. When credit spreads start to stabilize and then narrow, that for us is a good signal about the future sentiment towards risk assets.”

“In summary, we're looking to go long duration. This will work both in terms of the recession risk and the soft landing scenarios. That’s why we're sticking with our longer-term view right now. We’re weighing the market, we’re not always voting with it, and sometimes even voting against it.”