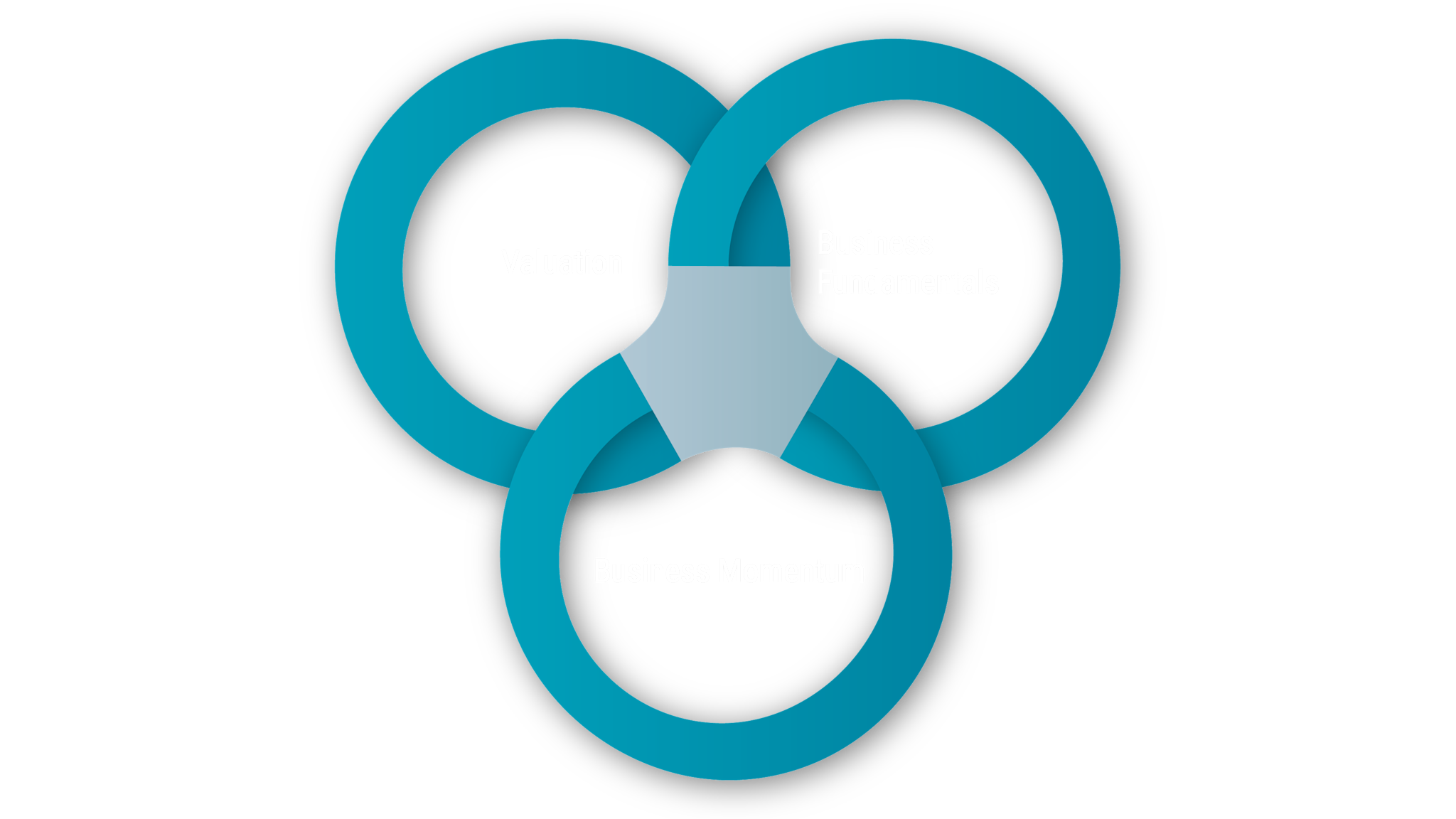

A time-tested approach

Boston Partners uses the tried and tested ‘three circles’ philosophy to find the best stocks across all capitalization sizes. A company must have good fundamentals, strong business momentum, and a valuation that allows for upside, to be eligible for inclusion in portfolios.