Strategist

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

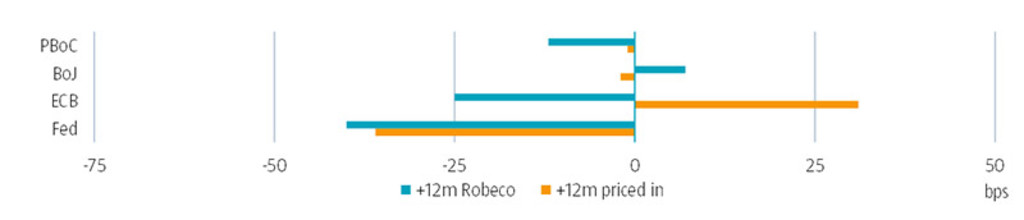

There’s no mountain high enough to bring inflation back under control. That’s the message from many of the main DM central banks, including the Fed and ECB. That message has been deemed credible if judged by the relative stability of the market’s medium to long-term inflation expectations. But it also comes at a cost.

By continuing to hike rates further into restrictive territory in an environment where overall inflation has already started to come down meaningfully, they deliberately run the risk of overtightening. This is seen as a risk worth taking, because rate hikes are more easily reversed than long-term inflation expectations. We expect the BoJ to join the camp of central banks’ tightening policy, but only slowly. This corresponds with the gradual pace with which Japanese inflation and wage data have been rising as of late.

While we see hiking cycles for many DM central banks being extended till the end of Q3, the PBoC is in an entirely different situation. Chinese growth is stagnating, despite the post-Covid reopening and policymakers having been easing conditions to stimulate the economy. Ain’t no mountain high enough indeed has a different meaning for individual central banks.

Subscribe to our newsletter for investment updates and expert analysis.