Portfolio Manager

• Monthly outlook

The new scarcity: Diversification

Diversifying portfolios is becoming more difficult as asset classes move in the same direction, and while equities are dominated by Big Tech, Robeco’s multi-asset team says.

Authors

Client Portfolio Manager

Top keywords

Summary

- The negative correlation between equities and bonds has disappeared

- Investors should blend quant and fundamental techniques to find winners

- Consider alternative sectors like commodities, small caps, and EMD

A high correlation between stocks and bonds means switching from one to the other does not offer the risk/return diversification that it once did, says Mathieu van Roon, Portfolio Manager with the Investment Solutions Multi-Asset team.

Meanwhile, the mega-cap concentration within stocks, as only a handful of Magnificent Seven and other tech companies account for the bulk of market returns, presents poor diversification opportunities within the same asset class.

Instead, investors should look at the more unloved parts of the market, including private equity replication strategies, commodities, small-caps, and emerging market debt, Van Roon says.

“For decades, multi-asset investing meant balancing equities and bonds in a traditional 60-40 portfolio,” Van Roon says. “This also proved useful when equities and bonds moved in different directions; when stocks went down, bonds went up, and vice versa. That worked when diversification was abundant and economic regimes were stable.”

“Today, geopolitical uncertainty, inflation and technological disruption mean investors can no longer rely on a simple two-asset portfolio. Even as markets reach new highs, portfolios have become increasingly concentrated around a narrow set of risk drivers.”

“Technology dominates global equity markets. A handful of mega-cap companies drive an ever-larger share of developed market returns, while emerging markets are increasingly exposed through semiconductors, AI infrastructure and digital platforms. As a result, many investors may be less diversified than they realise.”

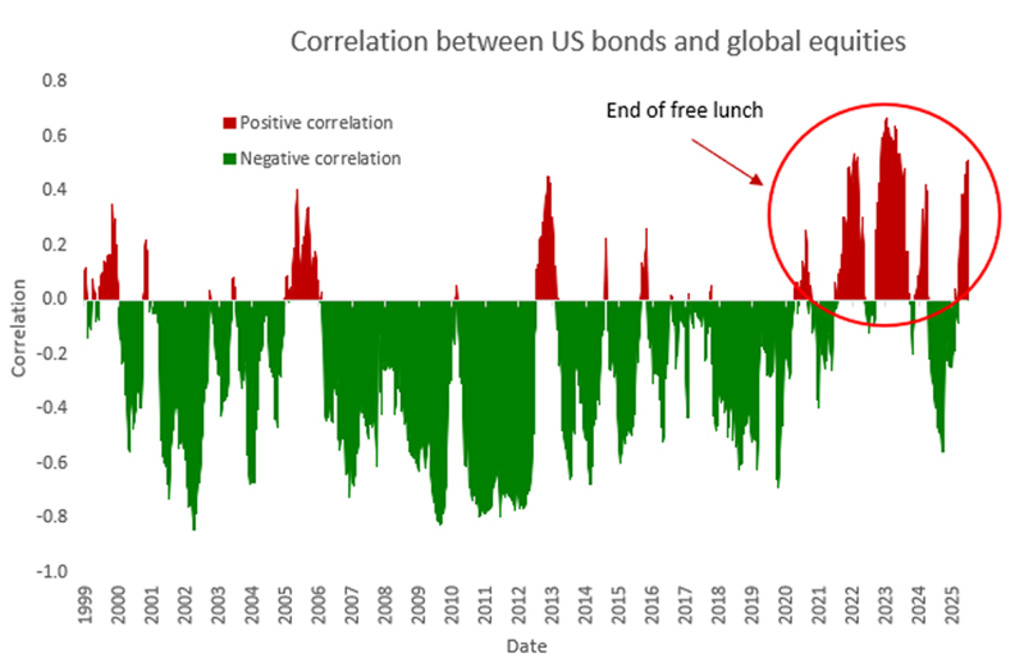

Moving together in tandem

The negative correlation between equities and bonds has not been present in recent years, particularly since the war in Ukraine began in 2022, remaining a positive correlation until 2025. The negative correlation resumed in 2025 but it has now turned positive again in 2026.

Figure 1: The relationship between global equities and US Treasuries since 2000

Source: Robeco, Bloomberg, July 2026

“Meanwhile, globalization is giving way to geopolitical rivalry, supply-chain reshoring and greater policy fragmentation,” Van Roon says. “Corporate credit spreads also remain close to historic lows, leaving investors with limited compensation for taking additional credit risk.”

“There is no silver bullet, but investors can take steps to reduce portfolio concentration. Core equity and credit allocations can be worked harder to deliver more consistent returns, rather than the traditional method of merely mixing various investment styles.”

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Combining quant with fundamental

Instead of simply blending equity and credit styles between value and growth, a new paradigm is emerging – combining quantitative and fundamental investing – says Jonathan Arthur, Client Portfolio Manager with the team.

“Quant investing identifies opportunities across large datasets, while fundamental investing provides forward-looking insights and economic judgement,” he says. “Together, they create a more balanced risk/return profile across market cycles with less tail risk. This ‘dual alpha’ approach can strengthen both core equity and core credit portfolios.”

“Next, investors more than ever need to look beyond today’s high-momentum trades and have the conviction and open mindedness to search for longer-term winners. This naturally broadens the investment universe beyond traditional equity and bond allocations to include more outspoken regional tilts, and by adding emerging market debt, small caps, commodities, and alternative return sources.”

Core and satellite allocations

The multi-asset team does this for Robeco portfolios by implementing satellite allocations around a core portfolio structure. The core provides broad market exposure and forms the long-term foundation of the portfolio. Around that foundation, satellite allocations introduce differentiated sources of return that can complement traditional stock and bond holdings.

“Examples of these satellites include listed private equity replication strategies, which seek to capture many of the attractive characteristics of private markets while maintaining the liquidity and transparency of public markets,” Arthur says.

“Commodities have helped during recent periods of inflation surprises or supply disruptions, and we believe they are a main stay of the portfolios during various market cycles. Emerging market debt provides exposure to different growth dynamics and income opportunities, with a risk profile that is much more corporate credit-like, but with returns that are comparable to high yield.”

Targeting long-term themes

“Global small caps trade at historically attractive valuations, and the recent softening in rate-path expectations may act as a catalyst for greater investor interest in this somewhat unloved part of the market.”

Satellite allocations can also target long-term structural themes, Van Roon says. “While AI and digitalization dominate investor attention today, thematic leadership rarely remains constant,” he says.

“Clean technology, for example, has regained momentum as policy support during the recent Iran crisis when oil supply routes were shut off, lower financing costs and rising electricity demand have improved its outlook.”

Seeking multiple return sources

“Other overlooked themes may follow. Water infrastructure benefits from increasing scarcity and aging networks, while healthcare innovation is driven by demographic trends and scientific breakthroughs. The objective is to maintain exposure to multiple long-term trends as leadership evolves over time.”

“The years ahead are unlikely to be defined by one region, asset class or technology theme,” Arthur adds. “Instead, investors face greater uncertainty, wider performance dispersion and more frequent market rotations.”

“Portfolios with multiple sources of return are likely to be better positioned to capture opportunities and manage risk. Looking forward, diversification may become one of the most important drivers of investment success.”