Researcher

• 市場觀點

How Value investors can avoid the climate traps

Successful value investing and the decarbonization of portfolios are typically considered difficult to reconcile. This is especially the case after the recent comeback made by stocks from the energy sector, which often fall in the value camp. But we show it would have been possible to achieve both strong exposure to the value factor and a substantially lower carbon footprint than conventional value strategies.

概要

- Conventional Value investing exposes investors to climate traps

- Value strategies can be ‘decarbonized’ effectively

- Decarbonized Value remains attractively valued

Investors often face a dilemma when trying to both decarbonize their portfolio and get exposure to the value factor. The reason is that conventional value strategies tend to have high environmental footprints, including greenhouse gas (GHG) emissions, and are therefore typically exposed to what we call ‘climate traps’.

Such stocks may look cheap using common valuation metrics, but this is mainly because their environmental footprints are not well reflected in accounting numbers. Also, with the rise of sustainable investing, high-footprint stocks are expected to show structurally lower valuations. These stocks will turn increasingly attractive based on simple value metrics, implying that such metrics may no longer be adequate.

Effective value investing requires adjusting valuation models for future carbon costs

Effective value investing therefore requires adjusting valuation models for these future carbon costs. Considering this, we designed an innovative methodology to derive a ‘decarbonized value’ signal in 2019.1 This methodology adjusts the valuations of high-polluting firms, making them less attractive based on their environmental footprints and works, economically speaking, similarly to a pollution tax. 2

Our research shows that this approach would have effectively reduced the carbon footprint of value strategies over the 1986-2023 period, without giving up exposure to the value factor. Indeed, simulations suggest that the adjustments made do not cause major changes in terms of value exposure at portfolio level. As a result, decarbonized value can have a value exposure comparable to the conventional one.

In fact, we see that while some performance differences did appear over shorter periods of time, the correlation between the two value strategies generally remained very high over the past three and a half decades, and both performances tracked each other closely over the long run. Importantly, decarbonized and conventional value exposures offered comparable historical returns.

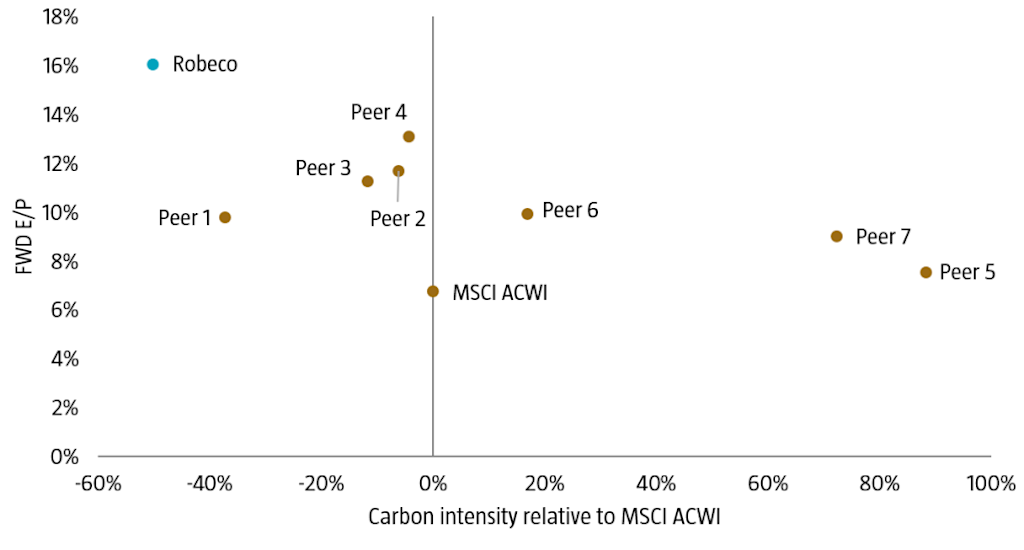

Moreover, we find that this holds true not just for simulated portfolios, but also in practice for real portfolios. Figure 1 plots these two measures for a set of value managers, including our Robeco QI Global Value Equities strategy, that implements our decarbonized value approach. The x-axis shows the relative carbon intensity, while the y-axis shows the forward price-to-earnings ratio.

Figure 1: Value exposure versus carbon footprint of set of Value

Source: Robeco, Morningstar, Refinitiv, I/B/E/S. The chart shows the forward earnings-to-price ratio (FWD E/P) and the carbon intensity relative to MSCI ACWI Index for a sample of global fundamental and quantitative value managers from Morningstar as of December 2022.

As the chart illustrates, most value managers have a larger or similar carbon footprint compared to the index, while two value managers – including Robeco – have a footprint below the index. At the same time, the value metrics of the portfolio remain high on our portfolio, showing that high value exposure is combined with a low carbon footprint, and low exposure to climate traps.

Value remains very attractive from a valuation perspective

Finally, we find that despite the significant market rotation seen since November 2020 and the related value comeback, both conventional and decarbonized value approaches continue to trade at attractive valuation spreads. More specifically, for both strategies, the valuation spread between value and growth stocks is much wider at the end of March 2023 than at the beginning of the value winter in 2018.

Conventional and decarbonized value approaches continue to trade at attractive valuation spreads

In fact, current spreads are still at levels close to those seen at the peak of the dot-com bubble in 2000, meaning that both conventional and decarbonized value continue to trade at very attractive valuation levels, from a historical perspective. Despite the strong rebound of value stocks over the past couple of years, conventional and decarbonized value approaches still have significant upside potential.

Footnotes

1 Swinkels, L., Ūsaitė K., Zhou, W., and Zwanenburg, M., October 2019, “Decarbonizing the Value factor”, Robeco article.

2 Cf., Blitz, D., and Hoogteijling, T., April 2022, “Carbon-Tax-Adjusted Value”, Journal of Portfolio Management.

探索量化價值

訂閱我們的電子報,獲取尖端的量化策略和見解。

重要資料

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。