Head of Investments China

概要

- National People’s Congress in March to confirm growth focus

- We are positioned for consumption to lead the economic revival

- Geopolitical tension is back and will continue to generate volatility but is largely priced-in, in our view

China has been a crowded trade at the start of 2023 but the bullish sentiment has dissipated somewhat in February. Negative news stories on China are dominating in western media, led by the shooting down of the ‘spy balloon’ by US forces, which caused the scheduled visit of US Secretary of State Blinken to China to be postponed.

From our perspective the geopolitical tension will wax and wane with the US and China now strategic competitors, but it’s an ongoing risk factor rather than something that will directly influence equity valuations in the short to medium term in the key sectors we focus on.

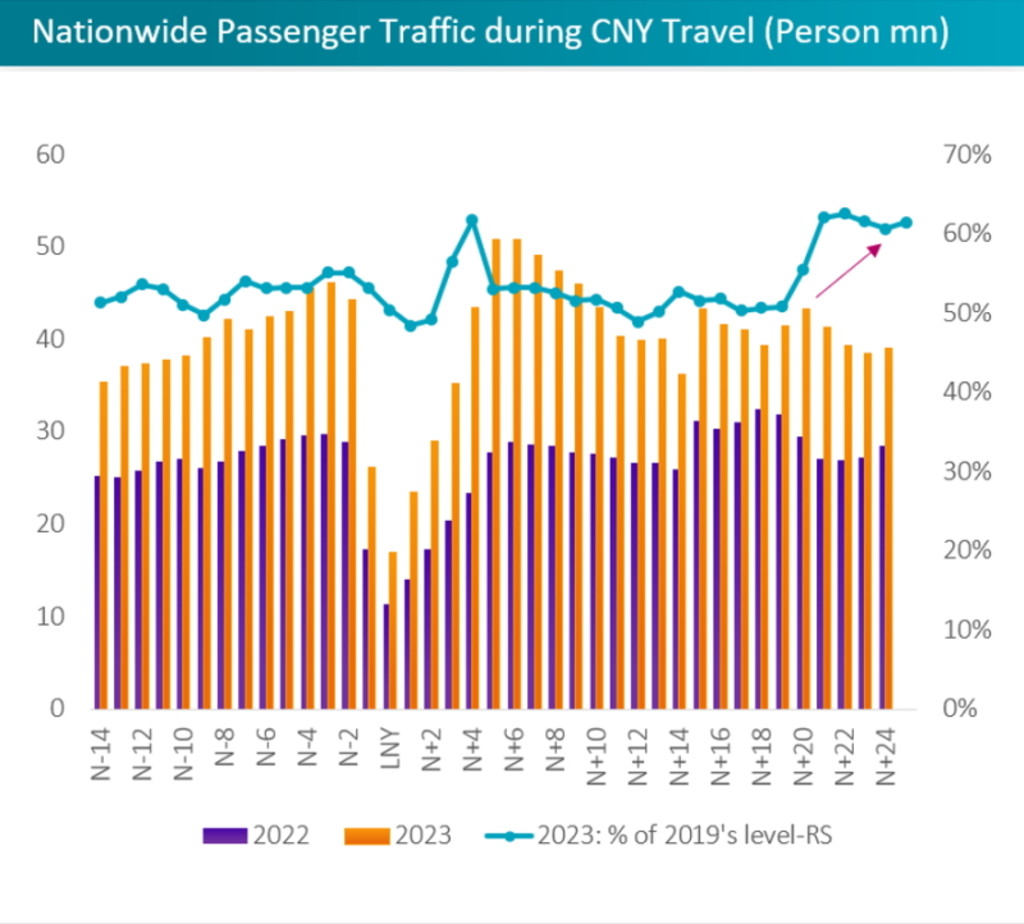

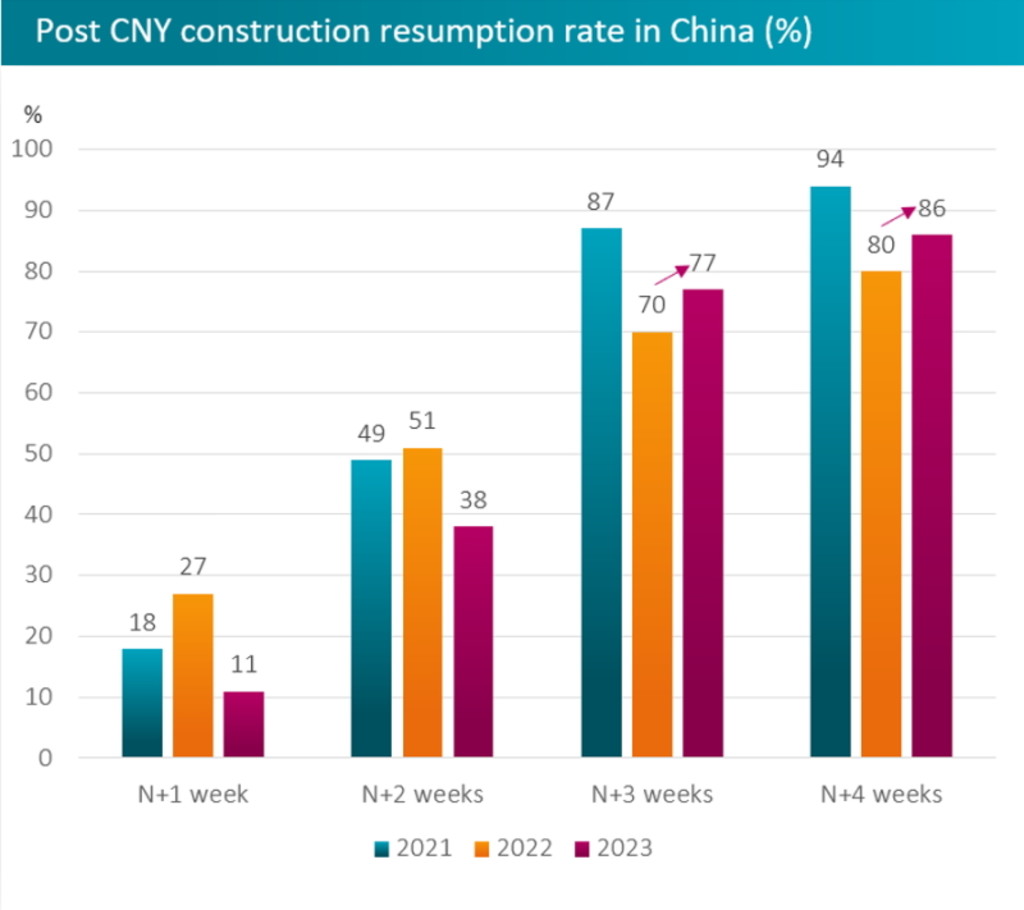

Data indicators like traffic flows show that China’s re-opening has gathered pace since the Lunar New Year holiday, which is positive news1. With rural migrant workers gradually back to the cities after the Lantern Festival (15th day of Chinese New Year) this year, the resumption rate for construction activities showed a strong year-on-year sequential rebound. Inflation remains subdued at 2.1% YoY while China’s PMI surprised on the upside in January2, which will hearten policymakers as they formally announce growth targets for the year at the National People’s Congress in early March.

Figure 1: The rebound is real

Source: Goldman Sachs Research as of Feb 15, 2023. N is the first day of Lunar New Year Day of the respective years.

Source: 100NJZ, February 23, 2023. N is the first day of Lunar New Year Day of the respective years.

However, the all-important property market remains subdued with signs of stabilization but no firm revival as yet, despite being a primary focus of policy action since October. China’s developers saw home sales fall 33% YoY in January according to CRIC data. Iron ore prices have rallied in February though, anticipating a construction rebound.

Now the initial excitement of Chain’s re-opening is over investors will start to focus on the earnings trend and policy actions from central government. Next on the agenda is the first session of the 14th Chinese People’s Political Consultative Conference (CPPCC) and the first session of the 14th National People’s Congress (NPC), known colloquially as the ‘Two Sessions’, which take place in early March and is likely to reiterate the pro-growth policy framework established at the end of 2022.

Our expectations for the meeting are straightforward. According to reports of a February 21 CCP politburo meeting3 the focus remains on growth and raising the quality of growth so we don’t expect any departure from that script. That means a GDP growth target well above 5% which we believe is realistic. In terms of new policy announcements we also don’t expect anything dramatic but an allowance for a wider budget deficit to support the growth target. More encouragement for a further loosening of monetary conditions is also possible, aimed at supporting the property market. The already accommodative monetary stance is being reflected in loan growth data which saw a jump of 23% YoY in January4, backing up December’s strong data.

Consumption will lead the economic revival

We don’t expect any particular catalysts to excite investors from the ‘Two Sessions’. The market requires real evidence that the re-opening is starting to be reflected in earnings to move higher. Another possible catalyst would be evidence the property market is normalizing.

We are however confident that the government’s support for domestic demand will drive increased economic activity and this in turn could stimulate renewed entrepreneurial zest in China, which is the key to China’s long term growth. This will be initially reflected in retail sales but we believe the wider economy, including the property market will gather momentum as 2023 unfolds. With this in mind we have positioned for a consumption revival while continuing to favour long-term themes where we believe value lies, including the green economy, technology innovation, and the technological upgrade of China’s industrial base. China’s equity market is trading at attractive valuations below its historical average level, and earnings revisions could be a driver going forward.

Footnotes

1 https://www.bloomberg.com/news/articles/2023-02-21/china-s-clogged-roads-show-economic-recovery-gathering-pace

2 https://think.ing.com/snaps/china-pmi-surprises-the-market/

3 https://www.bloomberg.com/news/articles/2023-02-21/china-pledges-to-meet-economic-goals-as-recovery-takes-hold

4 https://www.reuters.com/article/china-banks-idINL1N350059

重要資料

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。