Head of SI Client Portfolio Management

• 市場觀點

How regulations promote sustainable investing

A raft of new EU regulations is set to promote investments that can help tackle climate change.

概要

- EU’s Sustainable Finance Action Plan changes the investing landscape

- Regulation classifies just how sustainable an investment fund really is

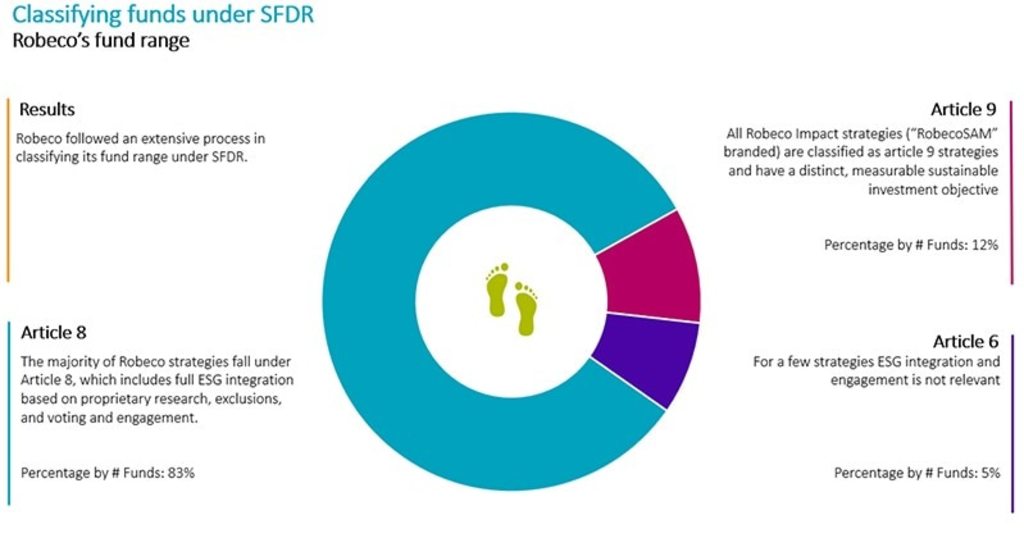

- 95% of Robeco funds meet Article 8 and 9 standards of sustainability

Investing has always been subject to regulations, to protect end-investors and maintain standards in a multi-trillion-dollar industry. What is new is a much larger commitment to promoting sustainable investing, led by the EU’s Sustainable Finance Action Plan (SFAP).

The Plan particularly aims to meet the climate goals of the Paris Agreement and the European Green Deal. Part of it will be embodied in new rules such as the Sustainable Finance Disclosure Regulation (SFDR), which clarifies what constitutes sustainable investment funds, and the Taxonomy Regulation, under which asset managers have to disclose what impact (positive and negative) they are making.

The SFAP has three main objectives. The first is to reorient capital flows towards sustainable investment and away from sectors contributing to global warming such as fossil fuels. Second, it aims to manage financial risks stemming from climate change, resource depletion, and environmental degradation. Finally, it seeks to foster transparency and long-termism in financial and economic activity.

The SFDR aims to make the sustainability profile of funds more comparable and better understood by end-investors, using pre-defined metrics for ESG characteristics used in the investment process. As its name suggests, much more emphasis will be placed on disclosure, including new rules that must identify any harmful impact made by the investee companies.

Robeco has committed a dedicated project team of over 40 people to embed all aspects of the SFAP, which will come into effect in phases. The first important deadline of 10 March 2021 for the categorization of funds and disclosures required in fund prospectuses and on websites passed without a hitch.

Landmark agreements

The SFAP was first laid out by the European Commission in March 2018 in response to the landmark signing of the Paris Agreement in December 2015, and to the United Nations 2030 Agenda for Sustainable Development earlier in 2015, which created the Sustainable Development Goals. It is also aligned with the European Green Deal, which aims to see the EU carbon neutral by 2050.

The scope of the regulation is very broad and applies to asset managers, pension funds, EU banks and insurers, among others. A very visible and impactful element in the new regulation is the classification of funds and mandates in three categories, as described in Articles 6, 8 and 9 of the SFDR.

Levels of fund sustainability

Article 6 funds are those which do not integrate any kind of sustainability into the investment process.

Article 8 applies “… where a financial product promotes, among other characteristics, environmental or social characteristics, or a combination of those characteristics, provided that the companies in which the investments are made follow good governance practices.”

Article 9 covers products targeting bespoke sustainable investments and applies “… where a financial product has sustainable investment as its objective and an index has been designated as a reference benchmark.”

Some 95% of Robeco’s funds are classified as either Article 8 (83%) or Article 9 (12%) and just 5% as Article 6. Article 8 funds encompass the Sustainability Inside and Sustainability Focused ranges of strategies. Article 9 funds are the Impact Investing range and are labelled as RobecoSAM. Only a handful of funds such as those using derivatives, or cash accounts, do not integrate ESG.

Prioritising adverse impacts

Adverse impact statements will be required from July 2021. Every asset manager will have to describe its due diligence policy on how it will take the principal adverse impacts of investee companies into account when making investment decisions. It must also describe the actions it is taking to mitigate these adverse impacts.

This will be monitored using a system of 64 adverse impact indicators, of which 18 will be mandatory to report, and 46 will be voluntary. While detailed requirements have only recently become available, Robeco has dedicated efforts to make sure it is prepared, for example by creating adverse impact prototype tooling to assess the impact of the regulation.

EU Taxonomy

Another impactful element of the SFAP is the proposed EU taxonomy, which aims to create a harmonized understanding of what actually consitutes ‘green activities’. The EU has defined minimum criteria that economic activities should comply with in order to be considered environmentally sustainable.

In short, such activities should contribute substantially to one or more of the following six environmental objectives: climate change mitigation and adaption, protecting marine and water resources, transitioning to a circular economy, preventing pollution, and protecting or restoring biodiversity and ecosystems.

SFDR regulation

SFDR is an evolving set of EU rules aiming to create a level playing field for how sustainable investment strategies are classified by asset managers. It helps to clarify the definition of a ‘sustainable fund’ and combat the growing threat of greenwashing.

重要資料

本網站僅供《證券及期貨條例》(香港法例第571章)及其附屬法例所界定之專業投資者瀏覽及使用。 投資涉及風險。過往表現並不代表未來表現。本網站所載資料僅供參考之用,並不構成任何投資建議,亦非作出買賣任何證券或採納任何投資策略之要約或招攬。投資者不應僅憑本網站提供之資料作出投資決定,在作出任何投資決定前,應徵詢獨立意見(包括有關稅務影響之意見)。投資者應確保完全理解投資產品的相關風險,亦應考量自身投資目標及風險承受水平。投資乃閣下之個人決定。除非銷售投資產品的中介人已向閣下告知該投資產品適合閣下,並已解釋其符合閣下投資目標之原因,否則閣下不應投資。請參閱相關發售文件或其他法律文件,以獲取包括風險因素在內的進一步詳情。 本網站由荷寶投資管理香港有限公司發布,該公司受香港證券及期貨事務監察委員會(「證監會」)規管(中央編號:APU851)。本網站未經證監會審閱。 無法保證任何投資產品可實現其投資目標。概不就任何投資產品之表現或投資回報作任何聲明或承諾。投資的價值或會波動。本網站所載過往表現、推算或預測,均不應視作未來表現之保證或指標,且概不提供任何明示或暗示之保證。本網站內容建基於相信為可靠之來源,惟因應資料傳遞技術特性及須採用多項數據來源(包括第三方內容),故概不保證其準確性。所述觀點僅乃截至上述日期,或會隨市況變化而改變,可予更改而毋須另行通知。該等意見可能有別於其他荷寶投資專業人士之意見。因使用本材料或當中所載任何評論、意見或估算而引致之直接、間接或相應損失,荷寶概不承擔法律責任。荷寶並無責任更新本網站或任何網站內容。未經荷寶事先書面許可,不得複製、分發或刊發本網站任何材料。 除非另有說明,資料來源:荷寶。