Portfolio Manager

• Perspectiva mensual

La concentración pone a prueba la diversificación

Diversificar las carteras resulta cada vez más difícil, debido a que las clases de activos evolucionan en la misma dirección y el mercado de renta variable está dominado por las Big Tech, según afirma el equipo multiactivo de Robeco.

Autores/Autoras

Client Portfolio Manager

Top keywords

Resumen

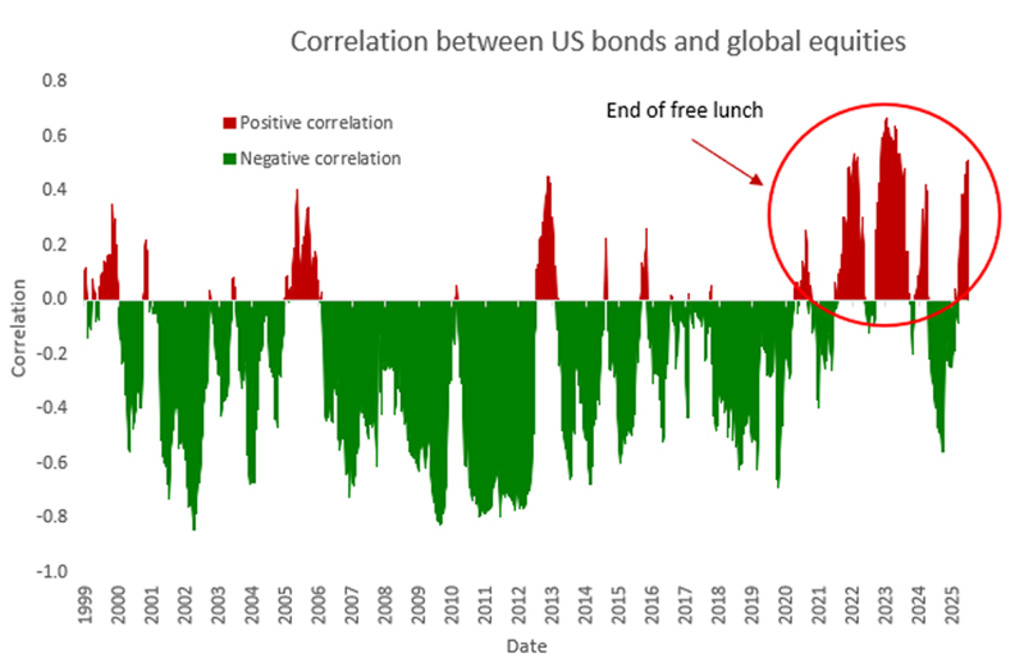

- La correlación negativa entre las acciones y los bonos se ha desvanecido

- Combinar análisis cuantitativo y fundamental puede ayudar a identificar oportunidades de asignación más atractivas

- Materias primas, small caps y deuda de mercados emergentes ofrecen nuevas vías para diversificar las carteras

Una elevada correlación entre las acciones y los bonos implica que pasar de unos a otros ya no ofrece el mismo grado de diversificación del perfil de rentabilidad/riesgo que en el pasado, afirma Mathieu van Roon, Portfolio Manager del equipo multiactivo de Robeco Investment Solutions.

Mientras tanto, la concentración de las compañías mega caps en el mercado bursátil ofrece escasas oportunidades de diversificación dentro de la misma clase de activos, ya que solo un puñado de las Siete Magníficas y otras compañías tecnológicas representan la mayor parte de la rentabilidad del mercado.

En su lugar, los inversores deberían fijarse en los segmentos menos populares del mercado, entre los que se incluyen las estrategias de réplica de capital privado, las materias primas, las small caps y la deuda de mercados emergentes, afirma Van Roon.

«Durante décadas, la inversión multiactivo consistía en equilibrar las acciones y los bonos en una cartera tradicional 60/40», afirma Van Roon. «Esto también resultó útil cuando las acciones y los bonos evolucionaban en direcciones opuestas: cuando las acciones bajaban, los bonos subían, y viceversa. Eso funcionaba cuando la diversificación era abundante y los regímenes económicos eran estables».

«Hoy en día, la incertidumbre geopolítica, la inflación y los cambios tecnológicos provocan que los inversores ya no puedan confiar en una cartera compuesta simplemente por dos activos. Aunque los mercados alcancen nuevos máximos, las carteras se han ido concentrando cada vez más en torno a un reducido conjunto de factores de riesgo».

«El sector tecnológico domina los mercados globales de renta variable. Un puñado de compañías mega caps generan una parte cada vez mayor de la rentabilidad de los mercados desarrollados, mientras que los mercados emergentes están cada vez más presentes a través de los semiconductores, la infraestructura de IA y las plataformas digitales. En consecuencia, es posible que muchos inversores tengan una cartera menos diversificada de lo que creen».

Avanzar juntos al unísono

No se ha observado ninguna correlación negativa entre las acciones y los bonos en los últimos años, especialmente desde que comenzó la guerra en Ucrania en 2022, y la correlación ha sido positiva hasta 2025. La correlación negativa se reanudó en 2025, pero en 2026 ha vuelto a ser positiva.

Gráfico 1: Relación entre la renta variable global y los bonos del Tesoro de EE.UU. desde el año 2000

Fuente: Robeco y Bloomberg, julio de 2026.

«Mientras tanto, la globalización está dando paso a la rivalidad geopolítica, al reshoring de las cadenas de suministro y a una mayor fragmentación de las políticas», afirma Van Roon. «Los diferenciales de crédito corporativo también se mantienen cerca de mínimos históricos, lo que deja a los inversores con una compensación limitada por asumir un riesgo de crédito adicional».

«No existe una solución milagrosa, pero los inversores pueden tomar medidas para reducir la concentración de sus carteras. Las asignaciones de crédito y renta variable core pueden aprovecharse mejor para obtener una rentabilidad más constante, en lugar de recurrir al método tradicional que se limita a combinar diversos estilos de inversión».

Acceda a las perspectivas más recientes

Suscríbase a nuestro newsletter para recibir información actualizada sobre inversiones y análisis de expertos.

Combinación de inversión cuantitativa y por fundamentales

En lugar de limitarse a combinar estilos de inversión en renta variable y crédito entre los enfoques value y growth, está surgiendo un nuevo paradigma, que aúna la inversión cuantitativa y por fundamentales, afirma Jonathan Arthur, Portfolio Manager de clientes del equipo.

«La inversión cuantitativa identifica oportunidades en grandes conjuntos de datos, mientras que la inversión por fundamentales aporta perspectivas de futuro y criterio económico», afirma. «En conjunto, permiten crear un perfil de rentabilidad/riesgo más equilibrado a lo largo de los ciclos de mercado, con un menor riesgo de cola. Este enfoque de "alfa dual" puede reforzar tanto las carteras de renta variable core como las de crédito core».

«Por otra parte, y ahora más que nunca, los inversores deben poner la vista más allá de las operaciones actuales de gran momentum y tener la convicción y la mentalidad abierta necesarias para buscar valores rentables a largo plazo. Naturalmente, esto expande el universo de inversión más allá de las asignaciones tradicionales en acciones y bonos, para incluir orientaciones regionales más marcadas, además de incorporar deuda de mercados emergentes, compañías small caps, materias primas y fuentes de rentabilidad alternativas».

Asignaciones core y satélite

El equipo multiactivo lleva a cabo esta tarea en las carteras de Robeco mediante la implementación de asignaciones satélite en torno a una estructura de cartera core. La parte core ofrece una amplia exposición al mercado y constituye la base a largo plazo de la cartera. En torno a esa base, las asignaciones satélite aportan fuentes de rentabilidad diferenciadas que pueden complementar las carteras tradicionales de acciones y bonos.

«Entre estas inversiones satélite se encuentran, por ejemplo, las estrategias de réplica de capital privado cotizadas, que pretenden aprovechar muchas de las características atractivas de los mercados privados, al tiempo que mantienen la liquidez y la transparencia de los mercados públicos», afirma Arthur.

«Las materias primas han resultado de gran ayuda durante los recientes periodos de sorpresas inflacionistas o de interrupciones en el suministro, y creemos que constituyen un pilar fundamental de las carteras a lo largo de los distintos ciclos de mercado. La deuda de mercados emergentes ofrece exposición a diferentes dinámicas de crecimiento y oportunidades de ingresos, con un perfil de riesgo mucho más similar al del crédito corporativo, pero con rentabilidades comparables a las de los títulos high yield».

Centrarse en temáticas a largo plazo

«Las small caps globales cotizan con valoraciones históricamente atractivas, y el reciente debilitamiento de las expectativas sobre la trayectoria de los tipos de interés podría actuar como catalizador de un mayor interés de los inversores en este segmento del mercado, que hasta ahora no ha sido muy popular».

Según afirma Van Roon, las inversiones satélite también pueden centrarse en temáticas estructurales a largo plazo. «Aunque la IA y la digitalización acaparan hoy en día la atención de los inversores, el liderazgo en las distintas temáticas no suele ser constante», afirma.

«Las tecnologías limpias, por ejemplo, han recobrado momentum gracias al apoyo político durante la reciente crisis de Irán, cuando se interrumpieron las rutas de suministro de petróleo. Además, la reducción de los costes de financiación y el aumento de la demanda de electricidad han mejorado sus perspectivas».

Búsqueda de varias fuentes de rentabilidad

«Es posible que surjan otras temáticas que se hayan pasado por alto. El sector de las infraestructuras hídricas se beneficia de la creciente escasez de agua y del hecho de que las redes son cada vez más antiguas, mientras que la innovación en el ámbito de la salud viene impulsada por las tendencias demográficas y los avances científicos. El objetivo es mantener la exposición a múltiples tendencias a largo plazo a medida que el liderazgo evoluciona con el tiempo».

«Es poco probable que los próximos años vengan determinados por una sola región, clase de activos o tendencia tecnológica», añade Arthur. «Por el contrario, los inversores se enfrentan a una mayor incertidumbre, a una mayor dispersión en la rentabilidad y a rotaciones de mercado más frecuentes».

«Es probable que las carteras con varias fuentes de rentabilidad estén mejor posicionadas para aprovechar las oportunidades y gestionar el riesgo. De cara al futuro, la diversificación podría convertirse en uno de los factores clave para el éxito de las inversiones».