Quantitative investing

Robeco examines existing investment portfolios' exposure to factor premiums using its own customized scanning system. This is known as the 'Robeco Factor Exposure Monitor'.

The scan shows the relative underweights or overweights per factor (relative to the market portfolio). This can form a first step in the decision-making process for implementing factor investing.

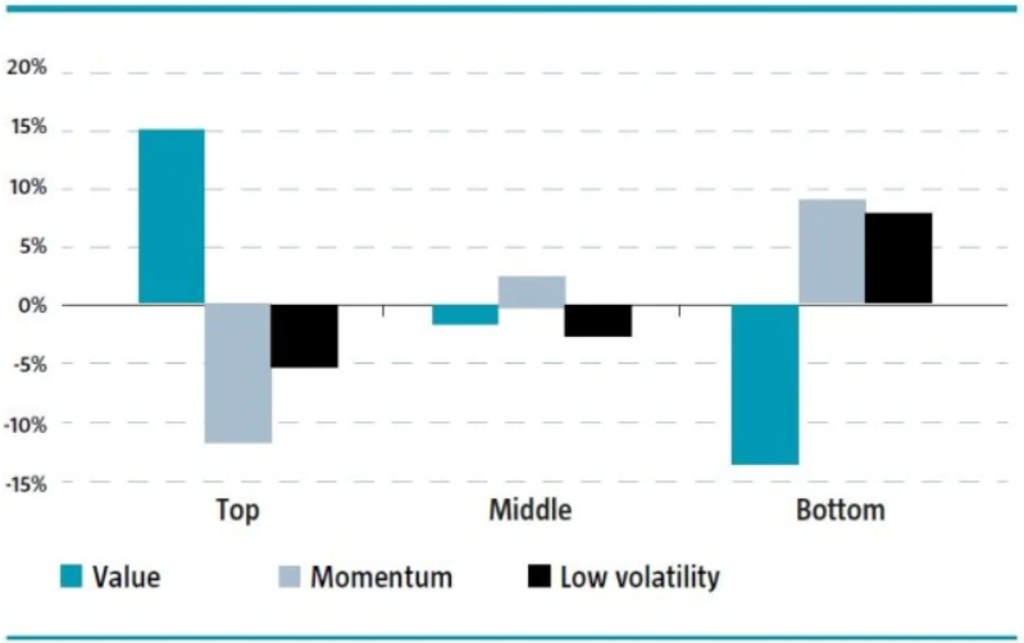

Figure 7. Relative factor exposures of portfolios

Source: Robeco, Quantitative Research, 2014

The chart shown above represents a portfolio that overweights the Value factor while underweighting the Momentum and Low-volatility factors.

See also