Portfolio Manager

• Insight

Sustainability investing under threat? Not so fast

After riding the tailwinds from bullish markets for several years, sustainable investing seems to have been affected by the winds changing course more recently. Many long duration ESG darlings, particularly in the clean tech, electric vehicle and consumer segments, have been suffering for a while now. At the same time, conventional wisdom around the exclusion of particular sectors such as defense, tobacco and large parts of the oil and gas sector, is being challenged.

Authors

Portfolio Manager and Co-Head of Robeco’s Global Equity team

Top keywords

Summary

- Underperformance of sustainable indices has been a trend change

- Post-pandemic and with a war raging, the world does look different now

- Sustainable investing still very much intact, but needs to move to a next level

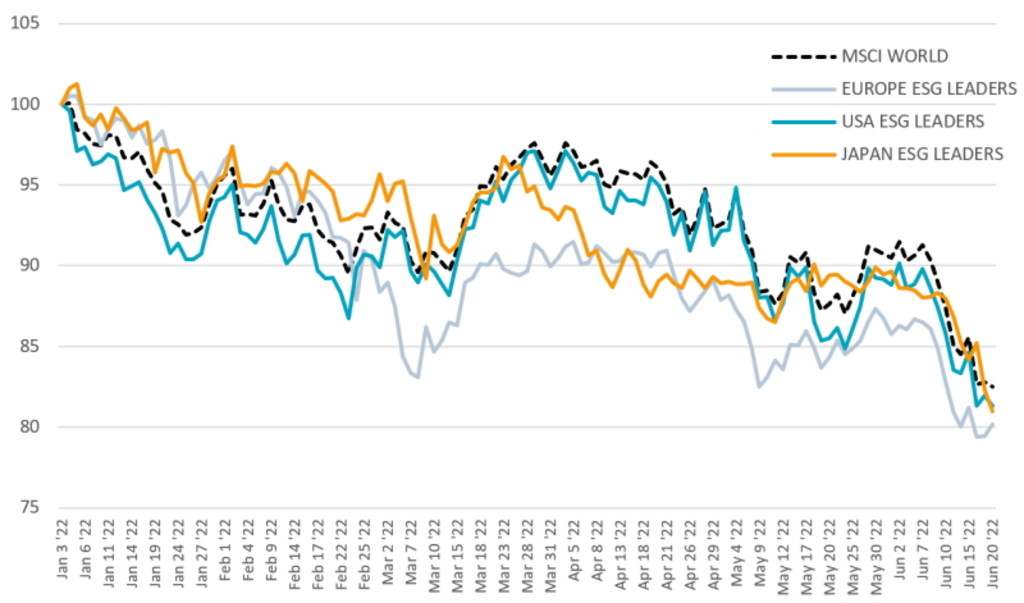

Figure 1 depicts the underperformance of the headline MSCI ESG Leaders indices across the major developed market regions compared to the MSCI World market index year-to-date in 20221. Even though severe geopolitical tensions, spiking inflation and recessions fears have hurt global equity markets as a whole, the underperformance of sustainability indices has clearly been a trend change compared to previous years2.

MSCI ESG Leaders performance 2022 YTD

Source: Bloomberg. Data from 3 January to 20 June 2022. Returns are in EUR.

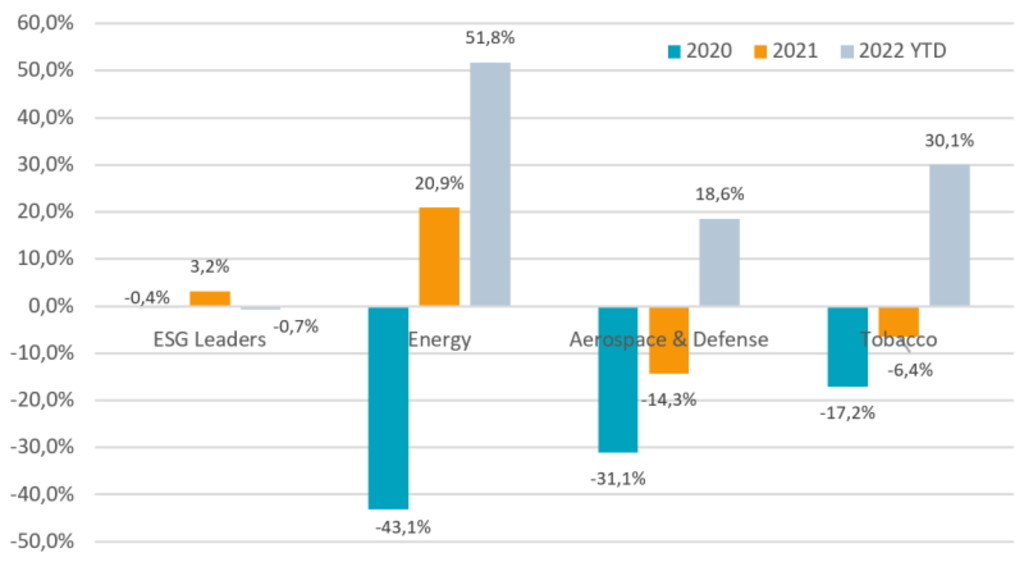

Market segments that have performed well, most notably fossil fuels, tobacco and defense, are commonly excluded by ESG investors, which probably explains a large part of today’s sustainability underperformance (Figures 2 and 3).

Excess performance vs. MSCI World (in EUR)

Source: Bloomberg, total return figures up 20 June 2022, in EUR.

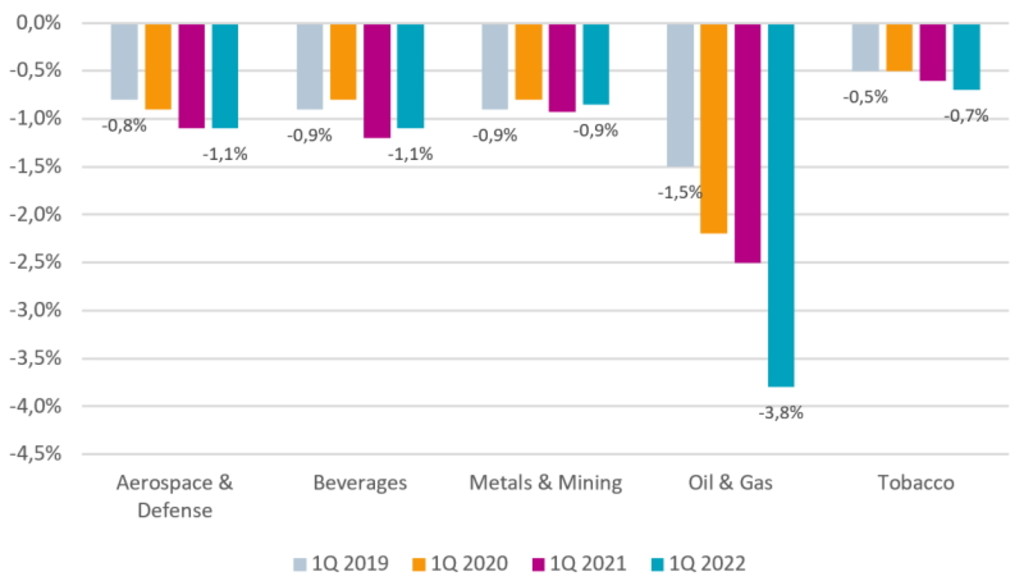

Global ESG fund positioning in commonly excluded sectors

Source: Bernstein research, June 2022.

Recent weaker sustainability performance has without question once again sparked the debate around whether ‘doing good’ equals ‘losing money’, implying there is a natural trade-off between the two. Ideally, we want to create both wealth and well-being, but obviously sustainability strategies sometimes have competing priorities. Examples include climate concerns versus the social costs of high energy prices, or investing in defense companies during geopolitical turmoil.

It is also clear that coming out of the Covid pandemic and with a war waging on the European continent, the world does look different this time – one in which sustainable investing has to evolve as well to better navigate increased market volatility.

As such, we could argue that sustainable investing is experiencing at least a ‘healthy’ reset in which mainstream assumptions about, for example, the effectiveness of strict exclusions but also ESG ratings are challenged. More sophisticated, practical approaches that apply more nuance and context will likely see increased market appetite.

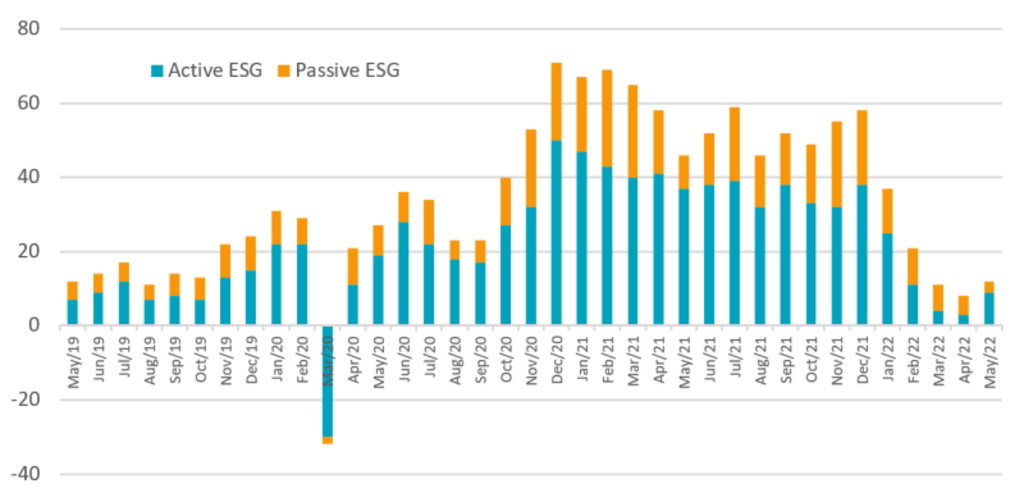

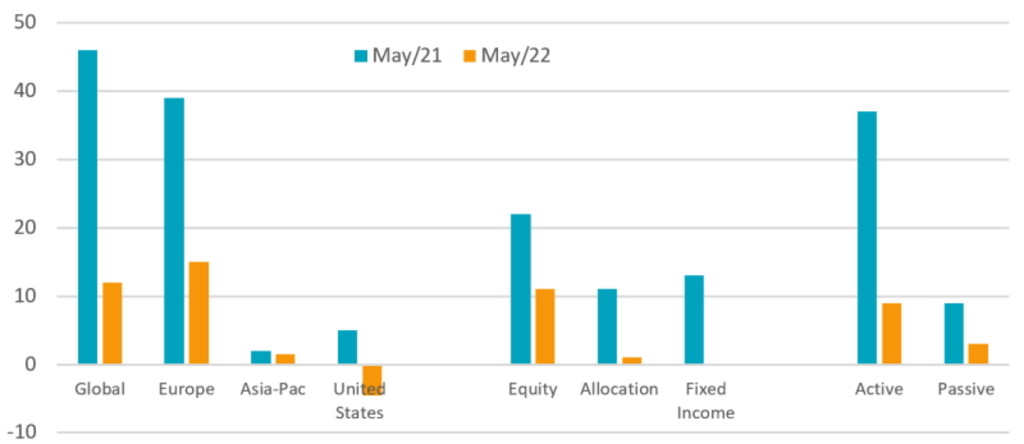

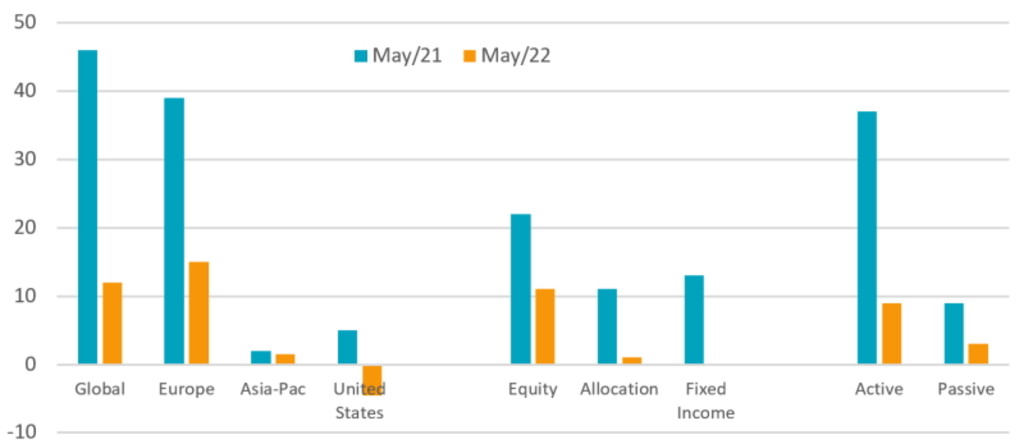

The recent dwindling market appetite for sustainable investing clearly shows in fund flows too. While sustainability has been the standout story of fund flows in recent years, that trend has arguably weakened in recent months (Figure 4). For example, inflows into ESG funds stood at USD 13 billion in May 2022, which is an over 70% decline compared to the USD 46 billion from a year ago.

Global monthly ESG flows (USD billion)

Source: Morningstar, Morgan Stanley ESG research, June 2022.

Figure 5 shows a further breakdown of the drop in ESG flows across regions, asset classes and investment strategies. That said, for the first time since late 2021, inflows are ticking up again slightly, in particular for active European ESG equity strategies.

ESG fund flows by region, asset class and strategy (USD billion)

Source: Morningstar, Morgan Stanley ESG research, June 2022.

So where to go from here? Given that ESG has different colors and flavors, sustainable investing, too, is not defined in one particular way. In practice, asset owners and investors can choose the sustainability strategy most suitable to reaching their specific objectives, whether that is more impact-oriented, best-in-class ESG, exclusion-based, or more mainstream ESG integration, to name just a few. And even within each of those categories, there’s often room to maneuver in which sustainability objectives do not necessarily have to bite investment returns. The question is how?

Keep up with the latest sustainable insights

Join our newsletter to explore the trends shaping SI.

A barbell approach

In today’s market environment, fund managers’ fear of misaligned exposure and, conversely, desire to mitigate volatility from crowded ESG positions is high. As such, a better balance between growth and value is required. To that end, we favor an approach of owning quality companies at a reasonable price on one hand and value exposure on the other hand as an inflation hedge. In other words, owning quality businesses underpinned by strong sustainability strategies, while getting exposure to ESG improvers on the value end of the spectrum, gives flexibility whereby sustainability is not necessarily ‘sacrificing’ returns, or vice versa.

In the context of sustainable investing such a barbell approach is often referred to as “ESG integration,” something successfully explored by, for example, the Robeco Sustainable Global Stars Equities fund3. Core to this strategy is the integration of financially material ESG factors into the investment process.

In other words, sustainability that directly impacts the valuation of a company, i.e., by altering its growth outlook, profitability, risk profile or overall competitive positioning. In practice this means the strategy not only looks for high positive impact companies, but also invests in companies that are riskier as far as ESG is concerned– as long as this is also reflected in the financial model and thoroughly addressed with company management through engagement.

ESG performance attribution Sustainable Global Stars Equities

Source: Robeco research, 2022.

Global Stars Equities D EUR

- performance ytd (31-3)

- -4.13%

- Performance 3y (31-3)

- 11.73%

- morningstar (31-3)

- SFDR (31-3)

- Article 8

- Dividend Paying (31-3)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

Sustainable investing has to evolve

Overall, every market environment brings new opportunities, also for sustainability investors. Within the wide range of sustainability strategies clearly some are more constrained than others, feeling the pain from sectors exclusions and factor exposures that until recently helped drive performance. Therefore, it becomes increasingly important to move sustainability beyond the stage of being a nice narrative alone and also stay valuation-disciplined by not overpaying for ‘good’; companies.

Going forward, we do not see the market appetite for sustainable investing suddenly disappearing. Despite seeing strong inflows for many years, still only a few percent of global assets under management are classified as ESG4, a number poised to go up over time given structural societal and regulatory support for sustainable investments5. Examples of the latter include the EU Taxonomy, a framework targeting environmentally sustainable activities, but also the EU’s more recent initiative to draft a Social Taxonomy, both of which are meant to re-direct and accelerate capital flows towards sustainable funds6. In short, despite weakening sentiment as of late, the structural underpinnings for sustainable investing still seem very much intact.

Today’s market environment, however, has taught us an important lesson; change is a constant. There is no free lunch – also sustainable investing has to advance to the next stage in its life cycle. Changing market dynamics demand a move away from simplistic, superficial sustainable approaches towards ones incorporating more forward-looking, nuanced insights and more thoughtful engagements. Ultimately, this should not only effect positive change with companies, but also make sustainable strategies more robust in navigating different, more complex market environments.

Footnotes

1 Data from 3 January to 20 June 2022.

2 Until Dec-2021, the MSCI World ESG Leaders outperformed MSCI World by 4.3% and 4.5% on a 3- and 5-year horizon, respectively. Source: Bloomberg.

3 As of end-May 2022, excess performance over a 1-year, 3-year and 5-year period are 1.2%, 4.1% and 2.9%, respectively. In measuring the impact of ESG on investment performance for the Sustainable Global Stars Equities fund, it turns out that between 2017 and 2021, around 20% of the fund’s excess returns can be attributed to the way the fund integrated ESG. Source: Robeco, June 2022.

4 Source: Barclays ESG research, ESG fund flow update, June 2022.

5 “Evolution in a Secular Story”, Morgan Stanley ESG research, June 2022.

6 Source: UNPRI, EU taxonomy, June 2022.