Strategist

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

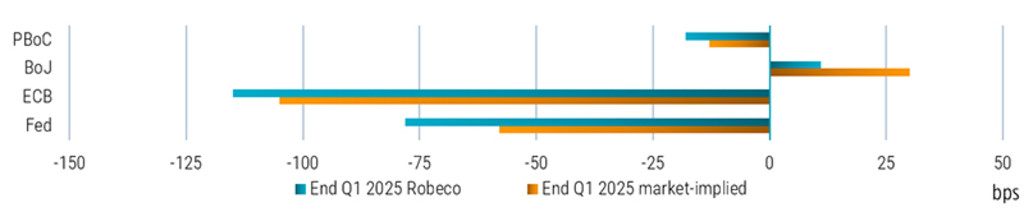

With the hump in US services inflation looking more protracted, markets seem to have concluded that the Fed won’t be among the first to reduce interest rates.

We concur that the ECB will ‘go its own way’ and begin easing monetary policy sooner, likely starting with a 25 bps reduction at the June meeting, which seems to be the current working assumption of the council. A more constructive stance on duration in the Eurozone hence makes sense. What is more, if history is any guide, yield curves in markets where central bank rate cuts are imminent, such as in Sweden, should show a steepening bias – with a spike in commodity prices arguably posing a risk to this.

The notion that the Fed’s next move will be a rate hike rather than a cut appears to be hasty from our perspective. We maintain that the Fed is capable of implementing cuts in the third and fourth quarters, but this is contingent upon receiving favorable inflation data shortly or observing signs of weakening in the US’s economic fortitude. A more immediate change is to be expected in the Fed’s balance sheet policy, where the pace of QT seems set to be reduced soon.

Elsewhere, both the PBoC and the BoJ will likely continue to also ‘go their own way’ in setting monetary policy. While foreign exchange pressures may postpone an additional reduction in the policy rate corridor until the third quarter, we anticipate that the PBoC will introduce further balance sheet expansion measures. As for the BoJ, we anticipate two additional rate hikes later in the year, with the timing of these increases dependent on the performance of the Japanese yen.

Source: Bloomberg, Robeco, change by end 2024, based on money market futures and forwards; 15 April 2024.

Subscribe to our newsletter for investment updates and expert analysis.

This information is for informational purposes only and should not be construed as an offer to sell or an invitation to buy any securities or products, nor as investment advice or recommendation. The contents of this document have not been reviewed by the Monetary Authority of Singapore (“MAS”). Robeco Singapore Private Limited holds a capital markets services license for fund management issued by the MAS and is subject to certain clientele restrictions under such license. An investment will involve a high degree of risk, and you should consider carefully whether an investment is suitable for you.