The Investment Engineers

Is it time to diversify beyond the US?

This article is part of a three-part investment series aimed at exploring regional alternatives to US-centric growth.

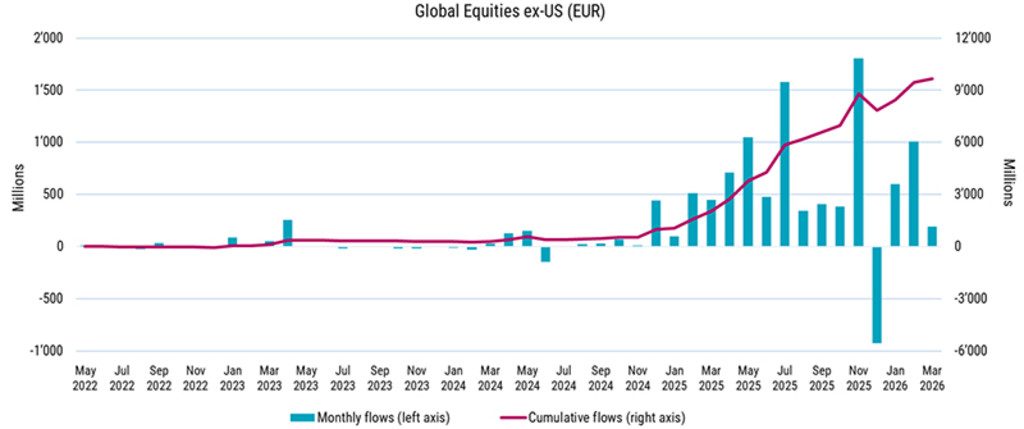

Over the past 12 months, a shift has begun to take shape among large asset allocators as they reassess the regional balance of their equity portfolios.

After more than a decade of US equity outperformance, capital is gradually rotating toward a broader opportunity set across global markets. This is not driven by a loss of confidence in the US, but the increasing attractiveness of opportunities elsewhere. Global markets are becoming more diverse in their drivers of returns. Differences in policy, economic structure and sector composition are creating a wider dispersion of outcomes across regions and companies. In this environment, leadership is less predictable and more fragmented, making access to a broader global universe increasingly important.

Source: Broadridge, Robeco, May 2026.

At the same time, the growing dominance of US asset managers means a significant share of global capital allocation is increasingly influenced by US-based institutions. This can reinforce home bias and crowding, leaving opportunities in other regions underexplored.*

For investors seeking to diversify beyond the US while maintaining exposure to regional and global growth, we highlight some of Robeco’s approaches for capturing this expanding opportunity set.

Robeco BP Global Premium Equities strategy is an unconstrained platform for finding investment opportunities anywhere in the world at attractive valuations. Throughout most of the strategy’s history, some of the most compelling opportunities have been found in European businesses. As a value strategy, it uses the Boston Partners’ time-tested ‘Three Circles’ approach. This seeks companies that are not only undervalued (mispriced) by the market but also have solid business fundamentals and strong forward momentum. This process guides portfolio construction, with the goal of targeting stocks that can generate alpha over time through both earnings growth and multiple expansion.

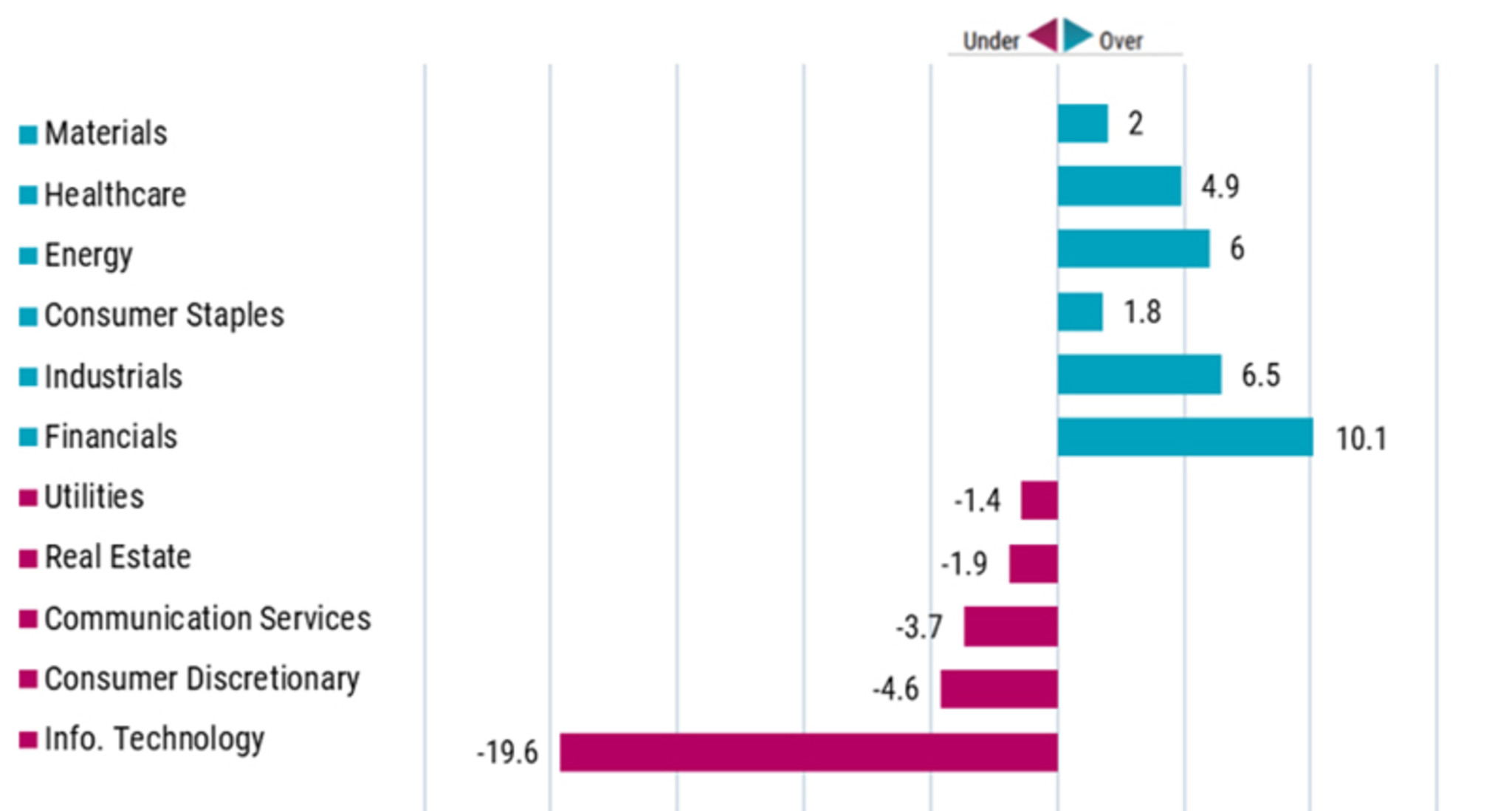

The strategy’s all-cap, global equity discipline allows it to invest across the world. In recent years, performance has been driven in part by European holdings, with two standout areas: banks and industrials. Once downtrodden, eurozone banks and other financial institutions, such as insurers, have enjoyed handsome margins amid rising interest rates and lower default/insurance claim rates compared with North American peers. Subsequently, European banks have outperformed the wider benchmark since rates first started rising from zero in 2022.** See Figure 2 for differences in the sector weightings between the strategy and the benchmark.

Source: Robeco BP Global Premium Equities strategy, reflecting where the strategy is overweight and underweight vs the benchmark (MSCI World) as of 31 March 2026. Cash and net other investments are excluded. For illustrative purposes only. This is the current overview as of the date stated above and not a guarantee of future developments. It should not be assumed that any investments in sectors identified were or will be profitable. GICS sector classification is used. All product characteristics and sector weightings are calculated using a representative account vs. the MSCI World.

Industrials tell a similar story, supported by rising government and corporate investment in real assets and capital expenditure, particularly in AI infrastructure and defense. The AI build-out is driving large-scale spending on new data centers and additional chip manufacturing capacity. At the same time, the EUR 800 billion ‘ReArm Europe Plan 2030’ initiative to counter Russia is accelerating investment across defense, from equipment such as tanks and weapons to ground infrastructure and cybersecurity. While this wave of spending has been a tailwind for industrial stocks in recent months, the Global Premium portfolio has been meaningfully overweight Europe and the UK for longer, reflecting the strategy’s focus on identifying mispriced businesses.

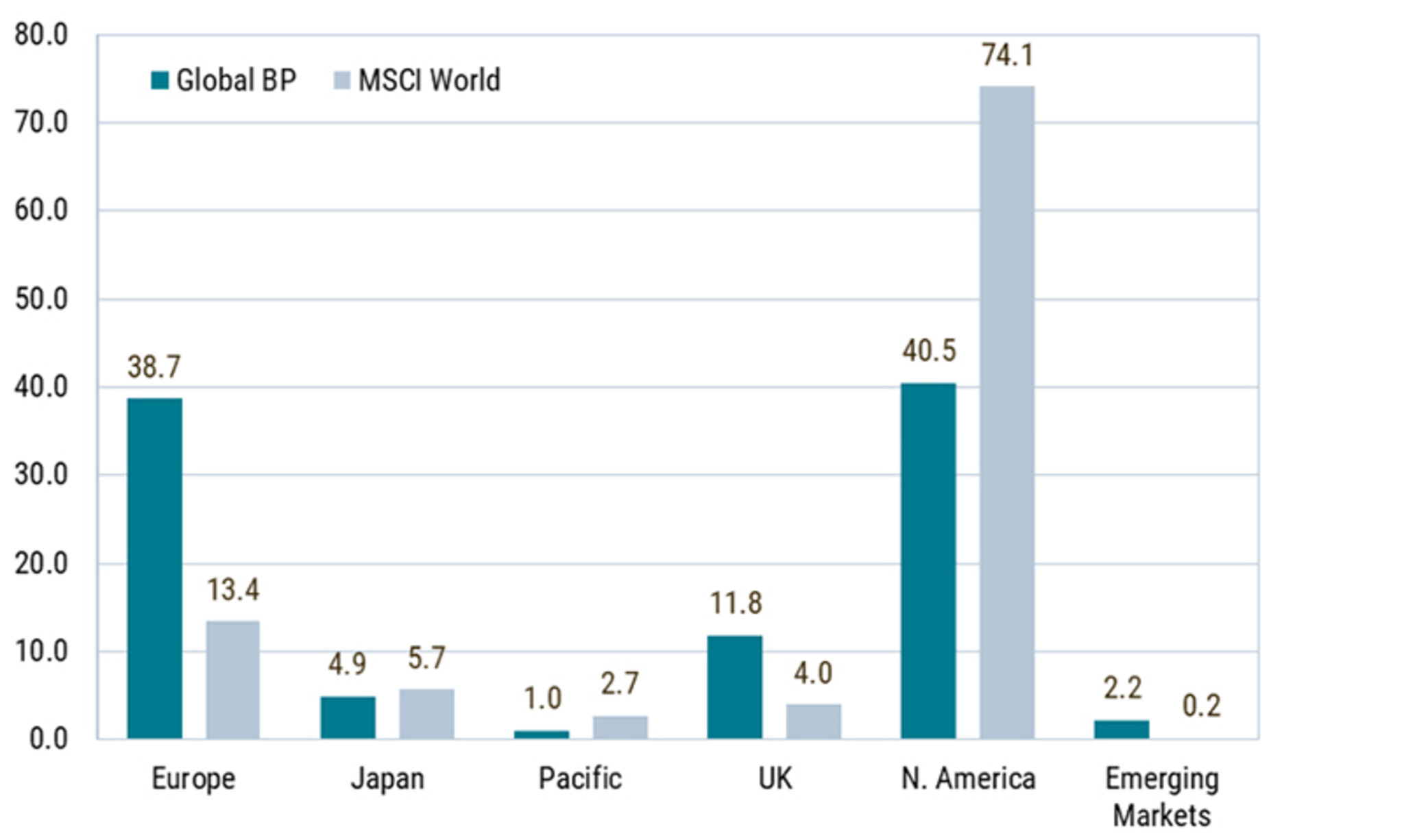

As a result, the Global Premium strategy’s exposure to assets in Europe has risen to 38.7% from 13.4%, and in the UK to 11.8% from 4.0%, while North American exposure has dropped from 74.1% to 40.5%. Differences in the regional allocations between the strategy and benchmark are reflected in Figure 3.

In all, the strategy offers a means of diversifying outside the US, while still keeping some exposure to the North American market, where some value opportunities do still reside.

Source: Robeco BP Global Premium Equities strategy’ regional exposure (%) as of 31 March 2026

Thematic equities are often perceived as narrow, growth-biased and US-heavy. However, Robeco’s thematic strategies have always been broadly constructed by design. They seek to capture the best opportunities from long-term trends that are evolving globally – in developed and emerging markets. Robeco’s ‘Smart’ strategies – which include Smart Materials, Smart Energy and Smart Mobility – perfectly illustrate our approach. They provide exposure to robust growth outside the US, as governments and private enterprise in regions worldwide seek to take advantage of the energy transition, the electrification of transport and other sectors as well as trends in AI and digital expansion.

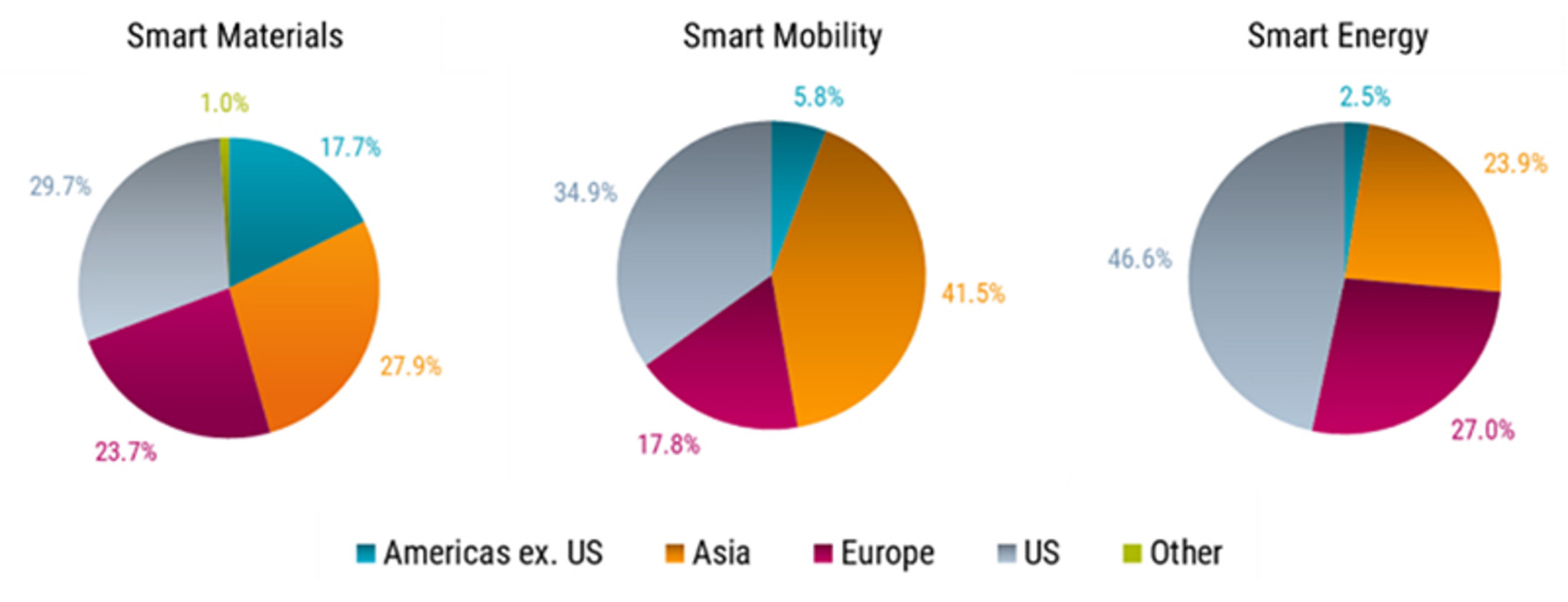

The Smart Materials strategy invests across advanced materials and industrial manufacturing value chains across the globe, all of which are being reshaped by AI, digitalization and next-generation technologies. It captures rising demand for transition metals and strategic minerals – essential inputs for semiconductors, infrared sensors, fiber-optic networks, power grids and high-performance magnets used in electric motors and turbines. Further downstream, the strategy captures growth through industrial manufacturers supplying components for advanced electronics, automation and robotics. Combined, its exposure spans mining and refining in the Americas, specialty processing and automation technologies in Europe, and component manufacturing and electronics infrastructure in Asia (see Figure 4 for regional allocations).

Source: Robeco. April 2026. For illustrative purposes only. This is the current regional allocation for each strategy as of 31 March 2026 and not a guarantee of future developments. It should not be assumed that any investments in regions identified will be profitable.

The Smart Energy strategy captures opportunities surrounding electrification and the broader energy transition that is playing out globally. That means investing in the entire ‘transition’ value chain, from power generation and grid infrastructure to downstream electrification and energy-efficiency solutions. Volatile energy prices and the drive for energy security are accelerating investment in renewables, while surging electricity demand from AI and data center buildout is driving grid expansion. Together, these forces are creating a broad investment cycle across the strategy’s key clusters including solar, wind, renewable power producers, battery storage, transmission infrastructure, electrical networks as well as energy-efficient semiconductors and power electronic components.

Smart Mobility strategy invests across the full fleet of technologies underpinning EVs and modern mobility, including chips, software, sensors, battery components, and charging stations. These segments are becoming more sophisticated and increasingly AI-driven, supporting growth in autonomous driving, robotics and related enabling technologies. Rising fuel costs, emission restrictions and lower cost of ownership are accelerating global adoption. The underlying value chains are global with European companies supplying vehicle engineering, safety and intelligence systems; LatAm and Asia supplying lithium, battery cells, semiconductors, sensors and scaled manufacturing; and North American companies supplying chip design, software, robotaxis and ride-sharing services.

In addition to diverse regional exposure, Robeco’s ‘Smart’ strategies also enjoy a strong mid-cap tilt, resulting in a high active share (typically 96-98%) versus the MSCI World. Whether from trend or stock selection, they can provide a differentiated alternative to US equities by accessing globally dispersed value chains that are strongly linked to structural growth.

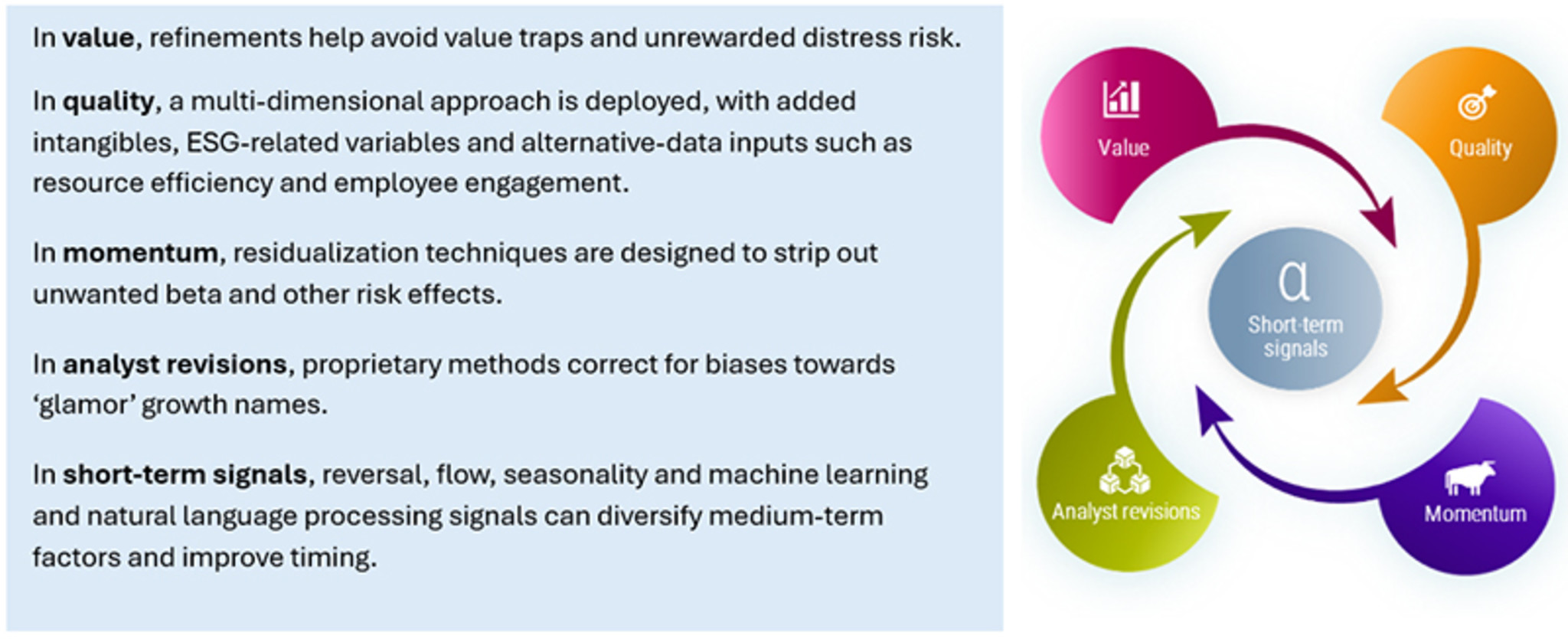

Robeco’s global quant strategies are designed to process large universes, identify patterns, and implement insights efficiently. At their heart lies the stock selection model, built around a diversified set of alpha signals that evolves over time (see Figure 5). By combining diverse signals, our model aims to systematically identify the most attractive opportunities while maintaining tight control over risk. Within this framework, investors can access global opportunities in different ways, depending on their objectives.

Enhanced Indexing is designed for investors who want to stay close to the benchmark in overall risk terms, while aiming to improve on passive exposure through disciplined stock selection and implementation. Global Enhanced Indexing operates within relatively constrained tracking error budgets and aims to deliver a stable edge after costs, with market-like absolute risk characteristics, making it particularly relevant for investors seeking a core global equity allocation that can fit naturally within existing policy portfolios and risk frameworks.

For investors willing to accept a broader tracking error budget in pursuit of higher alpha, our Active Quant approach to global equities remains benchmark-conscious and risk-aware but allows for broader deviations where the model identifies stronger opportunities. That creates greater scope for alpha generation while still maintaining a disciplined framework for risk control and implementation. This is important because investors increasingly do not want to choose between ‘hugging the benchmark’ and taking unconstrained active risk. They want strategies that can pursue differentiated alpha while remaining transparent, systematic and disciplined.

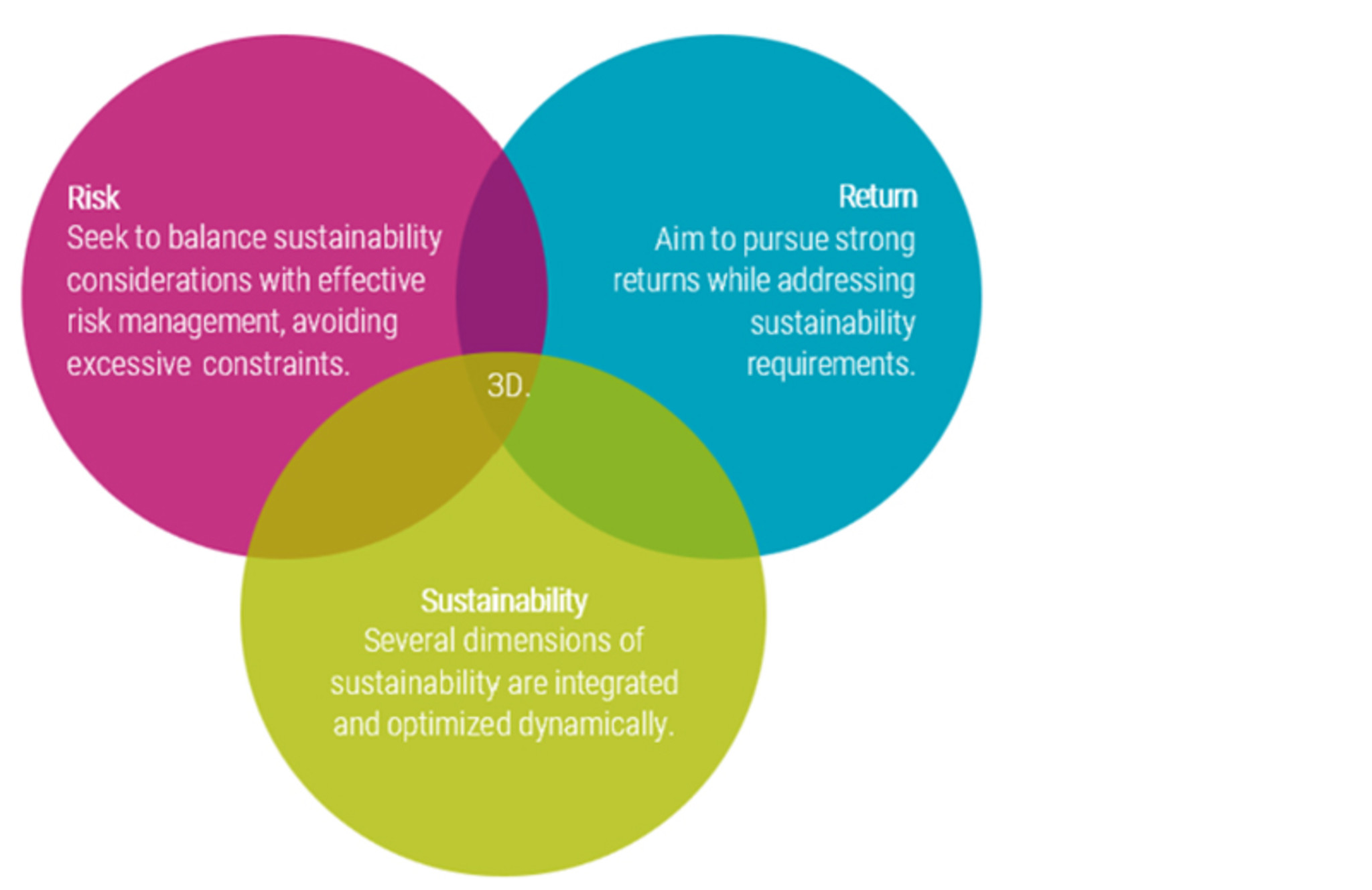

For investors prioritizing flexibility and implementation efficiency, this active ETF provides a modern way to access global equity markets. The 3D framework integrates risk, return and sustainability into a single portfolio construction process. Rather than treating these dimensions separately, they are considered jointly and optimized dynamically. Combined within an ETF structure, this results in a solution that offers transparency, liquidity and cost efficiency, while delivering a more balanced and forward-looking approach to global equity investing.

As equity market leadership shows signs of broadening, the case for looking beyond the US is becoming increasingly compelling. A global approach allows investors to access a wider, more dynamic opportunity set, shaped by differences in regions, sectors and economic regimes. As discussed here, whether through active value, focused themes, or systematic quant, investors have multiple ways to access this expanding landscape.

* See: https://www.bruegel.org/policy-brief/risks-europe-us-dominance-global-asset-management

** Past performance is no guarantee of future results. The value of your investments may fluctuate.

This article is part of a three-part investment series aimed at exploring regional alternatives to US-centric growth.