Portfolio Manager

• Insight

Using a circular economy lens to uncover value amid disruption

Persistent disruption is reshaping where value is created across the global economy. Whether from sudden commodity shocks or longer structural waves, the Circular Economy strategy is a broad but flexible strategy designed to not only survive but thrive amid disruptive change.

Authors

Summary

- Short-term shocks and long-term structural disruptions are now the norm

- Supply chains are shifting, as companies balance resilience and resource efficiency

- Circular principles and valuation discipline help detect where growth is moving

The global supply chain has absorbed a series of shocks in recent years – from the Covid pandemic and the war in Ukraine to escalating US-China tensions and conflict in the Middle East. These underscore that uncertainty and disruption are now the norm and can emerge from anywhere with unexpected consequences across sectors.

The Circular Economy strategy’s broadness was designed with change in mind. It is anchored around a core of stability but with the flexibility to dynamically shift to new areas where value and growth are accelerating. Investing through a circular lens helps narrow the focus to companies that produce more with less, optimizing resources and controlling costs. Companies that excel at doing this are able to create significant environmental, social and shareholder value in any environment, but particularly when input costs are rising and resources constrained.

In response to chronic upheaval and change, companies are duplicating segments of their supply chains to improve diversification and resilience. This is clearly illustrated in the ‘China plus N’ strategy whereby companies retain a manufacturing foot in China but also move capacity to other regions. This reduces dependence on any single country, policy regime or supplier. The shift is already redistributing demand for the AI build-out to upstream suppliers of critical inputs in the right places around the globe. Printed circuit boards (PCB) are a prime example. They are the foundational layers onto which chips, capacitors, resistors and other circuit components are fastened – providing literally the backbone of AI and modern electronics.

Global PCB output is projected to grow 12.5% to nearly USD 96 billion in 2026 alone, alongside demand for AI technologies,1 with many Circular Economy strategy holdings as clear beneficiaries.2 For example, Taiwan’s Compeq* and Japan’s Meiko*, which produce high-performance PCBs for servers and AI networking equipment, are gaining share as customers diversify production away from China and toward alternative Asian hubs with advanced know-how.

Diversifying beyond the US

The diversification wave is also hitting the US, where constant policy shifts, ‘on-off’ tariff switches and rising protectionism are encouraging some companies to co-locate production elsewhere. This is particularly evident across the AI and semiconductor value chain – from smartphones and laptops to data center servers and hardware – as firms seek to enlarge their vendor base as well as expand much-needed production capacity. 3

Eoptolink*, a supplier of high-performance optical transceivers critical for network communication between AI servers (and a holding), is a good example of how Chinese companies are capturing this branch of disruption. The company has seen significant year-on-year revenue increases and recently inked a deal with Nvidia* for next-generation optical modules. China’s neighbors are also benefiting from diversification waves. For instance, ASE*, the world’s largest provider of outsourcing for advanced semiconductor assembly and testing, is expanding manufacturing capacity outside of its home market of Taiwan toward Southeast Asia in order to offer customers geographic diversity. 4

Circular Economy D USD

- performance ytd (30-6)

- 31.05%

- Performance 3y (30-6)

- 23.05%

- morningstar (30-6)

- SFDR (30-6)

- Article 9

- Dividend Paying (30-6)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

Reshoring to the US

Reshoring is a reverse trend that is also gaining momentum, as US tariffs and protectionist policies raise the cost and risk of producing outside the US. In addition to punishing policies, the US is also offering sweet incentives in the form of subsidies and tax breaks in order to attract companies to the US. This wave of domestic investment is already feeding through to the strategy’s holdings. Applied Industrial Technologies* and Wesco* are industrial distributors and automation providers which are benefiting from increased factory build-outs and the need to modernize production systems. Similarly, engineering and construction firms such as Emcor* are seeing rising demand linked to new manufacturing capacity and facility upgrades.5

The forces of AI and digital expansion

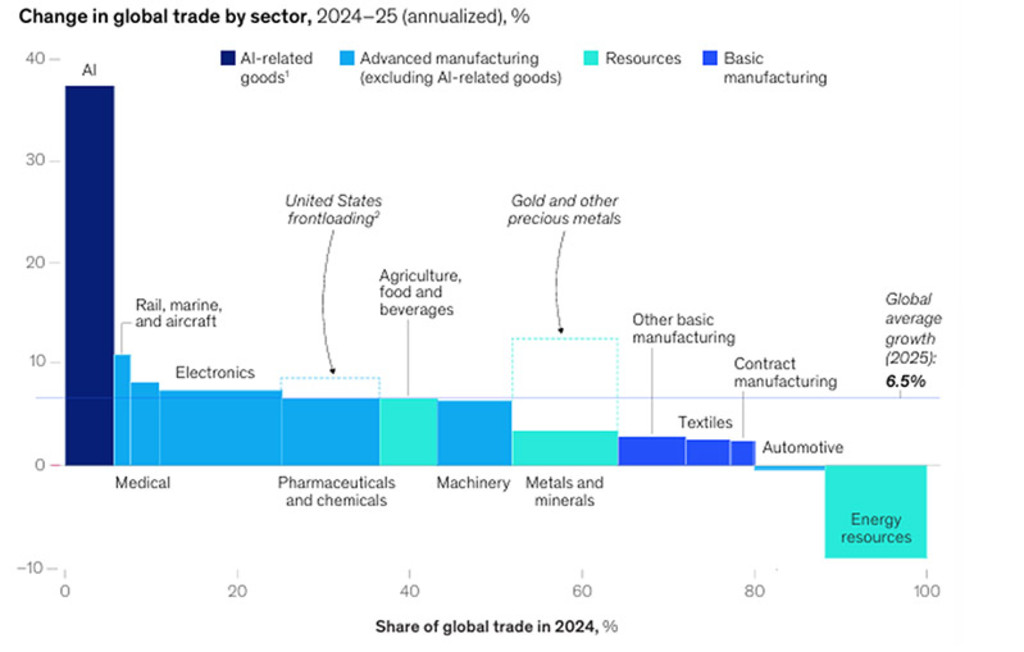

As seen through a circular economy lens, AI and automation are key sources of value creation as digital technologies enable more output with fewer material inputs (see Figure 1). As a result the strategy is discovering and benefiting from strong positions in companies across the AI ecosystem. The AI buildout requires highly advanced materials and specialized manufacturing – areas where Asia has built decades of know-how. Within this ecosystem, the Circular Economy portfolio is exposed to niche leaders of complex inputs located further upstream in the AI value chain.

Union Tool*, a Japanese leader in precision drilling for electronics, and Elite Material*, a Taiwanese maker of complex substrate coatings for PCBs, are illustrative of expert suppliers where bottlenecks are emerging. Backlogs are also building for Organo and Acter*, upstream suppliers of the ultra-pure water systems and cleanroom environments which are required for advanced AI manufacturing. 6

Figure 1 – AI’s share of global manufacturing trade is rapidly rising

Source: McKinsey Global Institute, Geopolitics and the geometry of global trade, 2026.

Discovering value amid structural shifts

The strategy’s edge lies in combining a top-down structural lens with bottom-up flexibility. Circularity provides a consistent framework – anchored in resource efficiency, system optimization and resilience – for identifying where long-term value will accrue. At the same time, active positioning allows the portfolio to adapt as macroeconomic and geopolitical forces reshape global supply chains in real time.

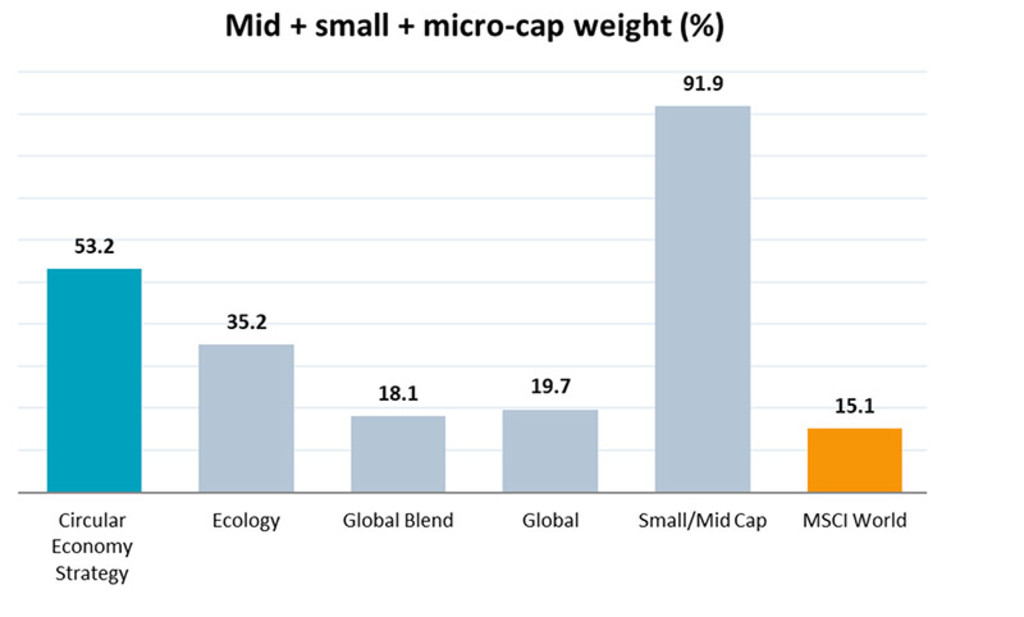

This flexibility is guided by a disciplined risk-return approach which aims to capture growth at a reasonable price while avoiding volatility and risks. In practice this means focusing on small and medium-sized companies embedded within value chains that offer robust growth and earnings potential but which may be under-researched and hence undervalued (see Figure 2).

Figure 2 – Differentiated market cap exposure

Over half of the Circular Economy strategy’s investments are in the mid- to micro-cap range, meaning it is significantly under-exposed to large- and mega-cap stocks relative to the benchmark as well as its Morningstar peer groups. The strategy’s mid-cap tilt enables it to capture the growth at lower valuations and risks thanks to the cost and resource-efficiency of niche players.

For illustrative purposes only. This is the current overview as of the date stated and not a guarantee of future developments.

Source: Morningstar, Robeco, 31 May 2026.

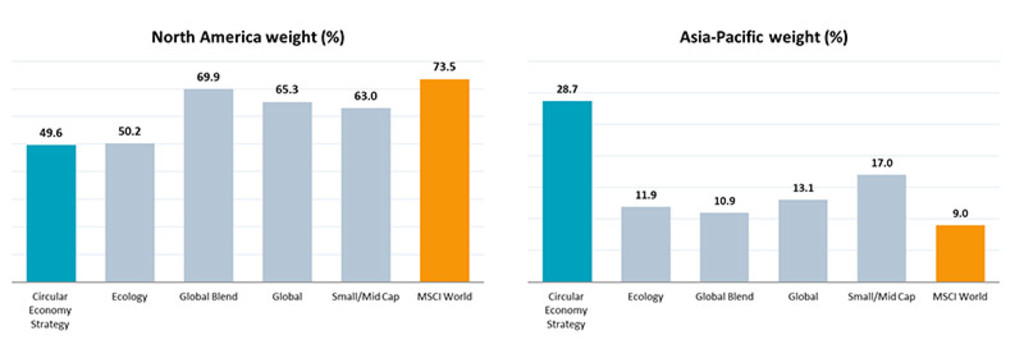

A similar logic means the strategy steers clear of the concentration risks of US markets and mega-caps and toward smaller firms whose margins demand more cost and resource efficiency. These are oftentimes small but leading companies in niche segments of value chains such as providers of PCBs, packaging and testing services, specialized engineering, or waste management services. These companies can be found globally, particularly in the Asia-Pacific which benefits from regional clustering effects associated with expertise in semiconductors and electronics industries (see Figure 3).

What’s trending?

All the latest thematic investing trends just one newsletter subscription away.

Figure 3 – Positively differentiated global exposure vs benchmark and peers

The Circular Economy strategy is significantly underweight in North America (49.6% vs 73.5%) and overweight in Asia relative to the benchmark (MSCI World) and Morningstar peer groups.

For illustrative purposes only. This is the current overview as of the date stated and not a guarantee of future developments.

Source: Morningstar, Robeco, 31 May 2026.

A triple advantage

Such an approach yields a ‘triple advantage’: exposure to structural growth at lower valuations and with lower concentration risks. This is particularly powerful as industries and manufacturing become more sophisticated and AI-driven, politics and trade trickier and resources more constrained.

The positioning also ensures the Circular Economy strategy remains highly adaptable in order to navigate the next wave of disruption wherever it arises. By staying focused on long-term themes of resource efficiency, while remaining flexible in short- and mid-term execution, it can shift with changing conditions and capture value as it migrates across regions, sectors and technologies.

*All companies referenced in this article are for illustrative purposes only in order to demonstrate the investment strategy on the date stated. The companies are not necessarily held by the strategy nor is future inclusion guaranteed. This is not a buy, sell or hold recommendation, nor should any inference be made on the future development of these companies.

Footnotes

1 Reuters, Iran war disrupts the circuit board supply chain, citing Goldman Sachs report. April 2026.

2 Taiwan Printed Circuit Association, March 2025.

3 TechCrunch, Microsoft, AWS and Google are trying to reduce China’s role in their supply chains, October 2025.

4 Taipei Times, ASE launches new Malaysia facility, February 2025.

5 Emcor’s full-year 2025 revenues saw strong double-digit percent growth (17%). Emcore press release, February 2026.

6 Organo’s order backlog rose 31% (through FY ending March 2026). Acter’s 2025 revenue rose 37% to USD 1.3-1.35 billion, while orders on hand exceeded USD 1.6 billion by early 2026.Acter revenues converted from New Taiwan Dollar (NT$) 41.48 billion and orders on hand from NT$ 50 bn using 1 USD = 31-32 NT$ spot range.