Strategist

• Insight

How climate change impacts different asset classes

We believe the climate impact on asset returns is not yet priced-in, and that it will become more significant over time.

Authors

Head of Solutions Research

Summary

- Physical and transition risks can affect asset classes differently

- EM and HY bonds are asset classes most vulnerable to climate change risk

- Portfolio construction should take climate change risk into account

In our recent Expected Returns, ‘The Age of Confusion’, we included the impact of climate change in our estimated returns for each asset class for the second consecutive year. Our methodology is still developing but we are clear that climate change will have a growing impact on investment returns in the years and decades to come, and in this insight we share what we have learned so far about modeling this impact.

The first instinct of investors when considering a hugely significant global challenge like climate change has been an understandable one – to exclude obvious climate change contributors during portfolio construction. In a recent survey, 27% of global investors have made public pledges for net-zero portfolios in or before 2050. As part of this, institutional investors plan to divest 19% of their portfolios because they are too carbon intensive, mostly in the asset classes equities and corporate bonds. This may lead to negative price pressure on assets with a high carbon footprint, leading to lower returns on the medium term.

We believe it’s potentially illuminating to consider the impact on expected returns of the physical risks (like floods or droughts) and the impacts of transition risks (like changing investment patterns, regulations or taxes designed to mitigate against climate change) on all asset classes. In this way we will get a holistic picture of how investors can take climate change into account for portfolio construction and investment decision-making purposes. Using this framework and taking into account other variables where appropriate like the discount rate, economic growth, and the carbon price, we assessed how climate change is likely to impact different asset classes from 2023-2027.

Government debt

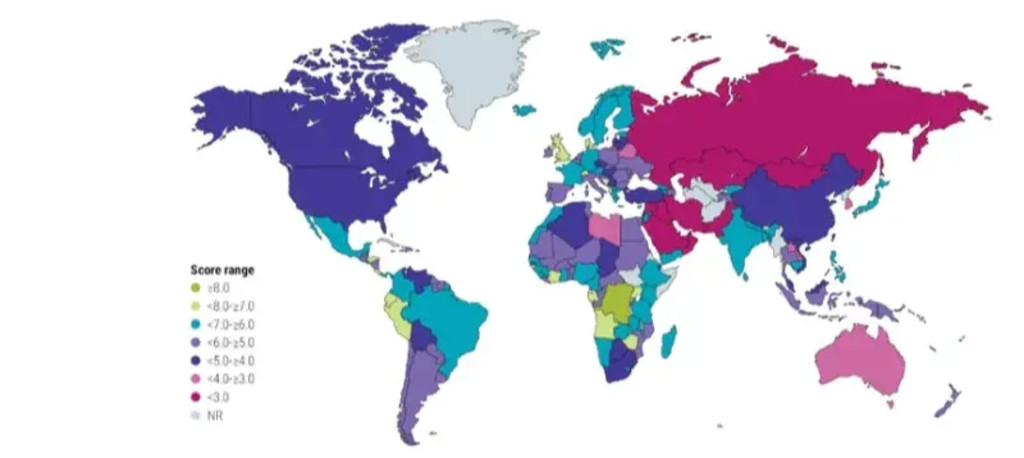

We started by noting not every government is equally vulnerable to climate change and the energy transition, so we have developed a Country Sustainability Ranking 1 which contains a climate and energy sub-score. This is based on indicators such as country carbon efficiency, the share of renewable energy, and climate risk indicators, and is shown in Figure 1.

Figure 1 | Robeco's country climate and energy score

Source: Robeco. Scores range from 1 (worst) to 10 (best). Scores as of April 2022.

Developed market government bonds

We assessed the climate change impact on developed market government bonds as neutral over the next five years. This is because government bond returns tend to be positively related to real economic growth, and negatively related to higher inflation. In the next five years the climate impact alone is likely to reduce growth below the previous trend level.

Penn2 (2022) surveys 55 academic studies on the effect of climate change and reports that the estimates vary considerably depending on the methodology used and geography examined. He finds an annual 0.3% lower global GDP a realistic synthesis versus a business-as-usual scenario. For inflation we believe the trend towards renewable energy is having an inflationary impact, an example of a transition cost. These two climate impacts, a lower GDP growth trajectory, and higher inflation due to transition costs, will cancel each other out from an expected returns perspective.

Emerging markets government debt

While the same dynamics apply as in the developed market assessment, there is a negative climate signal for investments in emerging markets debt over the next five years. We can identify at least two reasons why credit spreads of countries that are more vulnerable to climate change may be wider than comparable countries with less climate risk.

First, the physical risks are likely to be larger, leading to higher government expenses to repair damage resulting from climate-related disasters such as floods and storms. Second, energy in emerging markets is more likely generated cheaply but with low carbon efficiency, for example through coal-fired plants.

Large investments to change to more carbon-efficient technologies are required, and typically the government has to pick up part of the bill. In emerging markets this combination of physical risks and transition risks will lead to higher yields, and therefore be negative for bond returns in our assessment.

Corporate credit

For the corporate bond market we have access to data on climate risk in Figure 2. We found that carbon-emitting corporates are more prevalent in high yield indices than in investment grade. This may be due to climate change risk already materializing and carbon-intense companies becoming less creditworthy for long-run debt. However, it can also be due to the heavily fluctuating energy prices over the past couple of years, which materially affect the expected cash flows from operations from carbon-intense companies. All in all, investment grade receives a neutral climate signal, and high yield a negative climate signal.

Figure 2 | Climate change risk metrics for corporate bonds

Source: Robeco

Equities

We believe equity investors should consider how climate change will impact the cashflow generation abilities and the discount rate of the typical company in an assessment of net present value. Losses can be due to physical risk, for example when droughts or floods damage the production facilities, due to stranded assets related to new energy sources, or an increased price to emit carbon. Companies innovating for the energy transition may also benefit from climate change risk. In the next five years we expect more equity investors to start to scrutinize the risks that could result from climate change, leading to a larger discount rate on certain equity markets.

Emerging market equities more impacted

Applying the same method we used for corporate bonds, we assessed the climate risks of different sectors, both in developed market and emerging equities, in Figure 3. We evaluated carbon footprint, Climate Value at Risk, implied temperature rise, and this time also climate beta. This is a proprietary Robeco measure that indicates how sensitive the return of a stock is to the excess return of a polluting-minus-clean factor. Based on these variables we expect a negative but limited impact on overall expected developed market equity returns from the repricing of climate risk over the next five years.

These measures indicate emerging market equities are more vulnerable than developed market equities when it comes to climate change risk, mainly because of a much higher carbon footprint and projected temperature rises, so we give a negative climate signal.

Figure 3 | Climate change risk metrics for equities

Source: Robeco

Commodities

Climate change seems to be a double-edged sword when it comes to commodities. On the one hand, demand for commodities might decrease as global economic activity slows. On the other hand, increased physical risk resulting from climate change could see more frequent negative supply shocks hitting commodities, especially agricultural commodities. In the scenario of progress towards the Paris climate targets and the green energy transition, the commodity intensity of economic activity could increase due to increased demand for certain commodities like metals needed for electrification.

On balance, we give a positive climate signal to commodity markets, as we expect climate change will put upward pressure on commodity prices.

Conclusion

We have presented data modeling the climate change impact on asset class returns and, so far, for the largest asset classes like DM government bonds, that impact is limited. Nevertheless, it is clear that small changes in some variables like the carbon price could have an outsize effect on returns in the future. We expect more measurable climate impact each time we do our 5-year Expected Returns, and as the quality of data and our methodology improves.

Figure 4 | Climate signal for each asset class

Source: Robeco

Footnotes

1 Carbon Beta: A Market-Based Measure of Climate Risk by Joop Huij, Dries Laurs, Philip A. Stork, Remco C. J. Zwinkels: SSRN

2 Penn, M., 2022, “Assessing climate impacts on growth”, Absolute Strategy Research.

Important information

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.