Head of Quant Fixed Income and Lead Portfolio Manager

• Insight

Are credit factor premiums robust to rising inflation and interest rates?

Multi-factor credit strategies provide all-weather outperformance. This applies across inflation regimes, as well as in various interest rate environments.

Summary

- Individual factor premiums are influenced by macroeconomic regimes

- They display higher sensitivity to interest rates than to inflation

- Multi-factor strategies provide all-weather performance across regimes

Inflation worries and rates surges have afflicted markets over the last twelve months. Inflation has moved higher, driven to a large extent by the strong post-Covid economic recovery and the war in Ukraine. Developed market central banks have reacted firmly by, among others, implementing rate hikes not seen in decades. Market interest rates have surged in response.

In a previous article,1 we showed that multi-factor corporate bond strategies provide all-weather performance across inflation regimes. We use the recent extreme inflation developments to reassess the robustness of our findings. Given the sharp increase in interest rates over the same period, we extend our analysis to rates dynamics.

Overall, we reconfirm that multi-factor credit strategies provide all-weather outperformance, not only across inflation regimes, but also in various interest rate environments. Our conclusions are robust in the investment grade as well as high yield investment universes. As individual factors do show some sensitivities to the macro environment, we find that investors’ alpha is best protected against macro dynamics when combining factors in a multi-factor portfolio.

Inflation and rates changes over the past year have been extreme by historical standards and are in the top 5% of their respective historical distributions. Figure 1 shows that US headline CPI inflation has hovered around 2% for most of the sample period, in line with the Fed’s inflation target. However, it rose to 5.1% in June 2021 and then surged to 9.1% in June 2022, the highest level in 30 years. The US 10-year yield rose from below 1.5% in June 2021 to above 3% in June 2022, reaching one of the highest levels over the past 10 years, as the Fed hiked rates to contain inflation pressures.

Figure 1 | Inflation and interest rates dynamics

Source: Robeco, Bloomberg.

Period: January 1994-June 2022.

Over the past 12 months, our Robeco QI Global Multi-Factor Credits and Robeco QI Global Multi-Factor High Yield flagship funds (henceforth GMFC and MFHY) outperformed their benchmark by respectively 21 bps and 33 bps, in conditions that were difficult for credit markets – as evidenced by the fact that both benchmarks lost about 14% in total return terms.2

Investigating the macro sensitivity of factor premiums

We analyze the low-risk/quality, value, momentum and size factors, which are an integral part of our multi-factor investment process. These have been well documented in the academic literature and in numerous white papers.3 We use Robeco’s enhanced factor definitions and rely on data from January 1994 to June 2022, covering the global investment grade and global high yield universes separately.

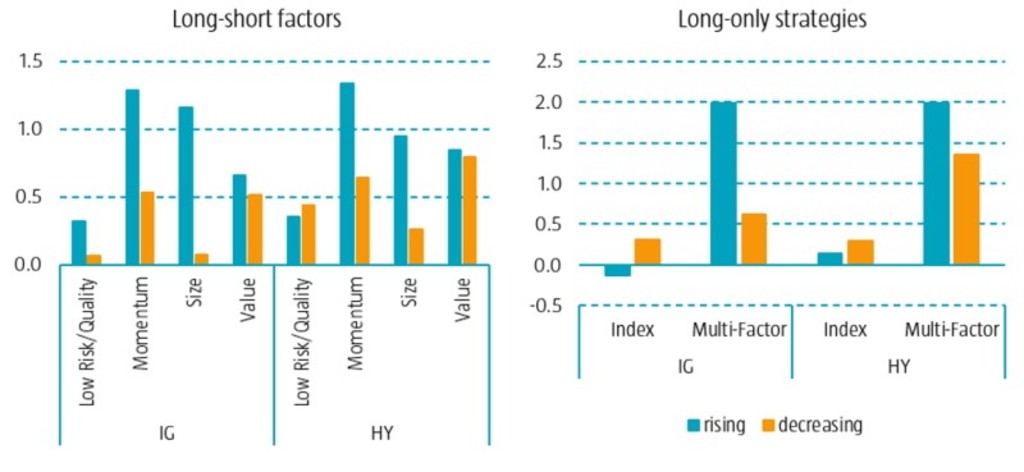

In Figure 2, we investigate the sensitivity of factor premiums to unexpected inflation changes. The chart on the left shows the Sharpe ratios of the individual long-short factor portfolios conditional on a rising or decreasing inflationary regime, for both investment grade and high yield. We see that the Sharpe ratios of the factors vary with the regime and are generally lower in regimes of decreasing inflation. Furthermore, we find that the Sharpe ratios are positive in all environments.

Figure 2 | Sensitivity of factor Sharpe and information ratios to unexpected inflation changes

Source: Robeco, Bloomberg.

Period: January 1994-June 2022.

In the chart on the right, we investigate the sensitivity of the Sharpe ratios of the market indices, and the information ratios of the multi-factor strategies. We find that the returns of the investment grade credit market are higher when inflation increases unexpectedly, while the Sharpe ratio of the high yield market seems insensitive to unexpected inflation changes. The long-only multi-factor strategies deliver highly significant information ratios in all environments, for both investment universes, that are higher when inflation surprises on the upside. The higher information ratios are mostly the result of lower tracking errors in inflationary regimes, while the outperformances are hardly affected.

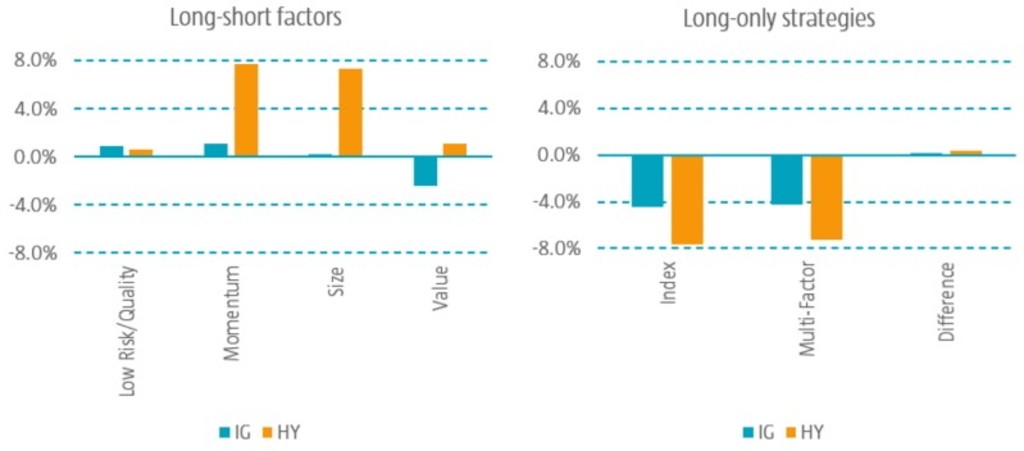

In Figure 3, we display the individual long-short factor premiums, the market returns and the outperformance of the multi-factor strategies over the last 12 months, in both investment grade and high yield markets. During that period, we experienced extreme inflationary pressures with nine months of rising inflation. As shown in the left chart, we find that, on the one hand, most of the factors exhibiting positive premiums in inflationary regimes in the full sample analysis also displayed positive performance out of sample, with the exception of the value factor in investment grade. On the other hand, the magnitude of the factor premiums was smaller than expected. One potential explanation for this behavior is that inflation was not the only dynamic at play and that other concerns (e.g. the risk of a recession) also influenced the factor premiums.

Figure 3 | Out-of-sample evidence on the factor premiums in inflationary regimes

Source: Robeco, Bloomberg.

Period: June 2021-June 2022.

In the right chart with the long-only results, we investigate the market returns and the outperformances of the multi-factor strategies. We see large negative credit returns of the investment grade and high yield markets, which were concentrated in months with unexpected inflation increases. The long-only multi-factor strategies delivered small positive outperformance in an inflationary environment for both investment universes.

Overall, we see from the above results that the very extreme unexpected inflation changes over the last year did not alter our conclusions. The outperformance over that period of our flagship products GMFC and MFHY provides further out-of-sample evidence of the ability of a multi-factor approach to deliver alpha in a rising-inflation environment.

Interest rate sensitivities

When considering changes in interest rates, we follow the same methodology as for the above analysis on inflation sensitivities. We are now interested in the coincident relationship between factor premiums and changes in interest rates, over the same measurement period.

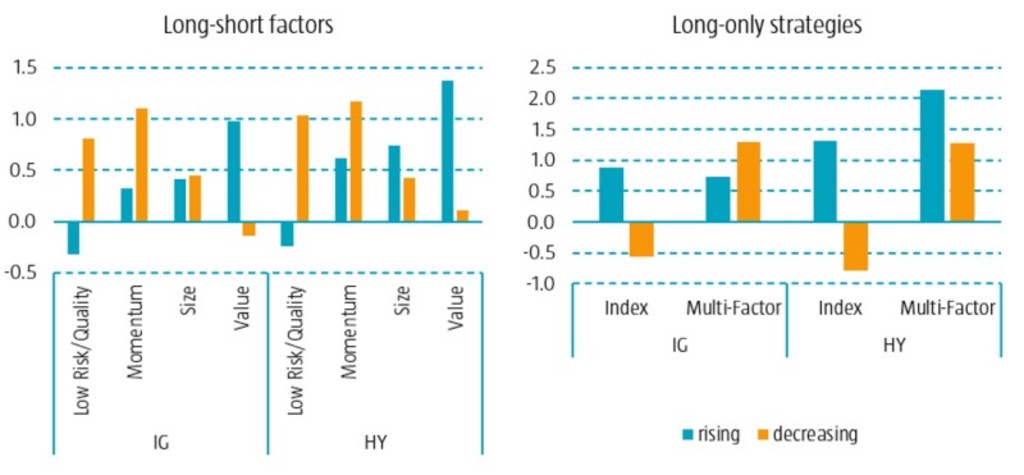

In Figure 4, the left graph again shows the Sharpe ratios of the individual long-short factor portfolios. We see this time that individual factor premiums are sensitive to the interest rate regime: when interest rates are rising, the low-risk/quality factor underperforms and the value factor performs strongly. Size, on the other hand, seems to be agnostic to changes in interest rates, while momentum earns a higher premium in a decreasing-rate environment. The performance differences between the factors suggest that combining factors in a multi-factor model might offer a more robust all-weather performance.

Figure 4 | Sensitivity of factor Sharpe and information ratios to interest rate changes

Source: Robeco, Bloomberg.

Period: January 1994-June 2022.

In the chart on the right, we show our findings on the sensitivity of the Sharpe ratios of the market indices and the information ratios of the multi-factor strategies. We find that the credit returns of the investment grade credit and high yield markets are markedly different across interest rate regimes. They are positively associated with rate changes, increasing (decreasing) when the interest rates are rising (falling). More importantly, the long-only multi-factor strategies deliver highly significant information ratios in all environments, for both investment universes. The differences in information ratios are mostly the result of tracking error variations across interest rate regimes, while the outperformances are hardly affected.

Conclusion

Overall, credit factors are more sensitive to changes in interest rates than to inflations dynamics. Nevertheless, multi-factor solutions offer consistent outperformance across regimes by exploiting the diversification in factor premiums across states. Ultimately, we find that investors’ alpha is best protected against changing macroeconomic conditions when combining factors in a multi-factor portfolio.

Foot notes

1 See “Are credit factor premiums robust to inflation?”, September 2021

2 Source: Robeco. Based on Robeco QI Global Multi-Factor Credits IH EUR share versus its benchmark the Bloomberg Global Aggregate Corporates index (hedged to EUR) and Robeco QI Global Multi-Factor High Yield IH EUR share versus its benchmark the Bloomberg Global High Yield Corporate ex Financials index (hedged to EUR) in the period July 2021 - June 2022. The currency in which the past performance is displayed may differ from the currency of your country of residence. Due to exchange rate fluctuations the performance shown may increase or decrease if converted into your local currency. The value of your investments may fluctuate. Past performance is no guarantee of future results. Returns gross of fees, based on gross asset value. In reality, costs (such as management fees and other costs) are charged. These have a negative effect on the returns shown.

3 For more information on these factors, see our white papers “The Low-Risk Anomaly in Credits” (2012), “Smart Credit Investing: The Size Premium” (2013), “Smart Credit Investing: Residual Equity Momentum” (2013), “Smart Credit Investing: The Value Premium” (2016), “The Quality of Low-Risk Credits” (2016) and “Factor investing in investment grade & high yield corporate bonds: an overview” (2018).

Important information

This information is for informational purposes only and should not be construed as an offer to sell or an invitation to buy any securities or products, nor as investment advice or recommendation. The contents of this document have not been reviewed by the Monetary Authority of Singapore (“MAS”). Robeco Singapore Private Limited holds a capital markets services license for fund management issued by the MAS and is subject to certain clientele restrictions under such license. An investment will involve a high degree of risk, and you should consider carefully whether an investment is suitable for you.