Strategist

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

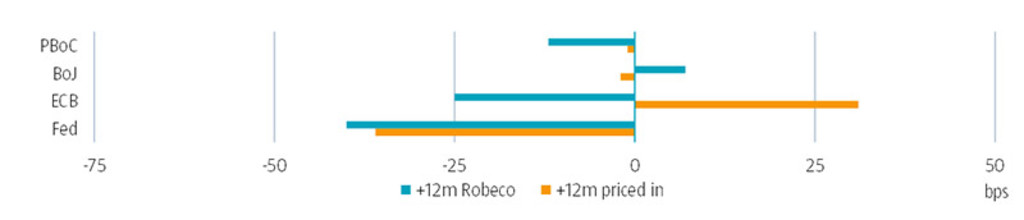

There’s no mountain high enough to bring inflation back under control. That’s the message from many of the main DM central banks, including the Fed and ECB. That message has been deemed credible if judged by the relative stability of the market’s medium to long-term inflation expectations. But it also comes at a cost.

By continuing to hike rates further into restrictive territory in an environment where overall inflation has already started to come down meaningfully, they deliberately run the risk of overtightening. This is seen as a risk worth taking, because rate hikes are more easily reversed than long-term inflation expectations. We expect the BoJ to join the camp of central banks’ tightening policy, but only slowly. This corresponds with the gradual pace with which Japanese inflation and wage data have been rising as of late.

While we see hiking cycles for many DM central banks being extended till the end of Q3, the PBoC is in an entirely different situation. Chinese growth is stagnating, despite the post-Covid reopening and policymakers having been easing conditions to stimulate the economy. Ain’t no mountain high enough indeed has a different meaning for individual central banks.

Subscribe to our newsletter for investment updates and expert analysis.

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.