Portfolio Manager

• Insight

Embracing equality – Quotas are nice but C-suites are better

Though board quotas are highly visible tools for raising awareness and reducing gender bias, companies serious about embracing diversity and all its benefits must seat more women in the C-suite.

Authors

Top keywords

Summary

- EU quotas aim to reduce inequality and shatter glass ceilings for women in business

- Quotas effective at breaking open boards but gender ratios in management remain low

- Embracing diversity in C-suites strengthens companies and returns

Late last year the EU Parliament mandated all companies listed on EU stock exchanges to have either a minimum of 40% women on their governing boards or at least a third of women as directors by 2026.1 Companies that fail to comply must “disclose-and-explain” how the selection process is objective and non-discriminatory. If companies don’t meet targets and lack sufficient explanation, they could face fines and rejection of elected board candidates. Though some member states already have quotas in place, the new law represents the first unified and binding requirement in EU history.

The employment rate for working-age women in the EU stands at 66% and women represent 60% of its new university graduates.2 Yet despite overwhelming credentials and workforce presence, the share of women on publicly listed EU boards is only 31.5%.3 In some member states that figure sinks to single digits.

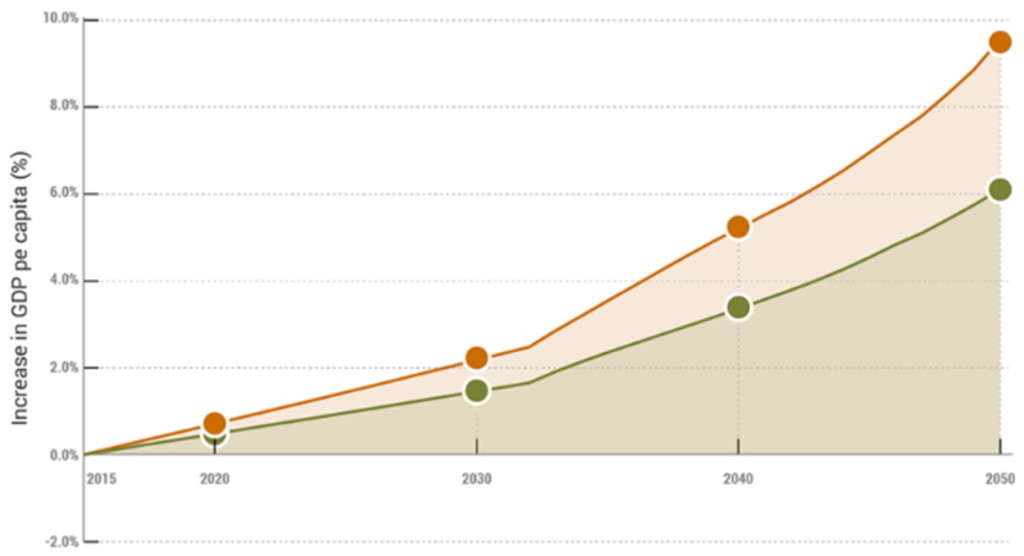

The law underscores the EU’s commitment to the “fundamental value” of equality between men and women. But it’s not just a question of social value: significant economic value is also at stake. Per the European Institute for Gender Policy, improving gender equality would add as much as 9.6% to EU GDP per capita (or EUR 3 trillion) by 2050 – contributing even more to per capita GDP than labor market and educational reforms (see Figure 1).4

Figure 1 Improving gender policies, boosts GDP

The figure illustrates the positive impact of gender equality on GDP per capita across the EU-bloc from a base year of 2015 through 2050. The green line tracks the increase in GDP with slower progress on gender reforms; the orange line tracks GDP increases with faster reforms.

Source: European Institute for Gender Equality, 2022

Board quotas – a powerful lever

Quotas have been a powerful lever for driving gender equality and improving diversity – on boards at least. Companies in EU countries with some form of gender mandate have greater female representation on boards than those without (30.4 % vs 16.6%).5 Moreover, stricter policies with sanctions for non-compliance work better than soft, voluntary measures. Norway, France and Italy – countries that combine higher quotas with binding sanctions – can boast women board seat shares of 45%, 44%, and 36% (up from 4%, 7% and 10%), respectively.6 The EU’s experience is echoed in developed markets globally – without quotas, boardrooms are largely off-limits to women.7

Gender quotas are also valued by investors. In the US, in the absence of federal mandates, investors have stepped in to demand more women on boards. Campaigns by its “Big Three” asset managers, Blackrock, Vanguard and State Street, helped increase female directors among US listed firms by a factor of 2.5 between 2016 and 2019.8 Even the tech-heavy Nasdaq instituted board diversity requirements for all companies listed on the exchange.9

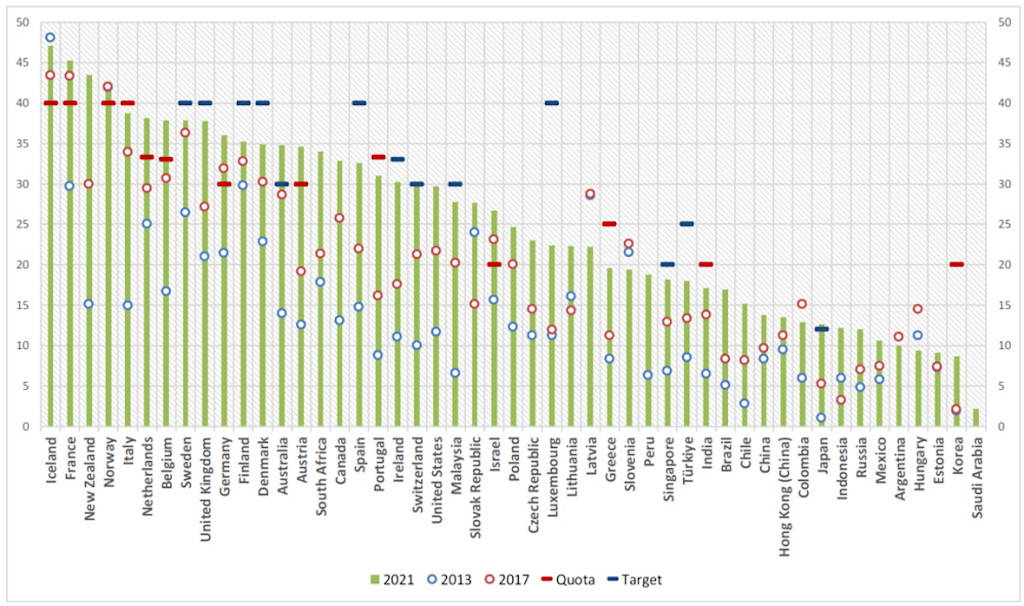

Figure 2: Regulated success – quotas are effective at putting women in board seats

The graphic illustrates the progress when countries take deliberate action to place women on boards either through quotas or targets. Quotas are hard legislative mandates whereas targets are softer recommendations to companies from regulators. Board-gender policies can significantly differ between countries. Please see the OECDs Gender Report for more details on country variations.

Source: OECD Gender Report 2022

Sobering statistics from the C-suite

EU lawmakers hope that giving women a unified voice at the top should also reduce inequalities in pay, compensation and advancement for women beyond the boardroom. But research thus far reveals that while quotas raise public awareness and improve board management and engagement, they do little to boost gender equality outside boardrooms.10 In Norway, the first country to enact sweeping national legislation, female share of boards jumped to 40%; yet senior management ratios and wages remain unchanged.11

That’s critical because to truly maximize the benefits of gender diversity, more women should be sitting in C-suites. McKinsey estimates that companies in the top 25% for C-suite gender diversity are 15% more likely to outperform. Credit Suisse research showed companies with 20% or more women executives generated a “gender dividend” driven by higher operating margins and higher cash flows.12 Other studies show a gender-diverse C-suite lowers financial risk, improves human capital management and stimulates innovation.13

Despite the benefits, the C-suite situation for women is sobering. In 2021 and 22, women represented around 5% of CEOs globally. EU figures were only slightly better at 7 to 8%.14

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Diving beyond board metrics

Since its launch in 2015, the RobecoSAM Global Gender Equality Strategy has always recognized that while women on boards is a good start, a company’s true commitment to equality is revealed in other characteristics beyond board seats. Our proprietary gender scoring system ranks thousands of companies within our investment universe across no fewer than 38 criteria which assess material metrics for equality and diversity including women in key management positions, pay parity, talent retention and work-life balance, in addition to board diversity and selection process.

Our stewardship efforts push companies to strive for best-in-class market practice. In most developed countries, boards should include at least 30% of the least represented gender. Moreover, we have a strong, consistent record supporting shareholder proposals for more disclosures on board nomination processes and diversity issues such as gender ratios and pay gaps across the organization’s rank and file. Recognizing the power of diversified human assets, we have broadened our engagement activities to protect the rights and promote the advancement of employees with different race/ethnicities, sexual orientations and identities, physical disabilities and mental health issues.

A bigger toolbox

Like hammers, quotas can shatter obstructing glass and bind sturdy structural beams, but more tools and materials are needed to build a resiliently diverse and optimally performing organization. Through its gender strategy and D&I engagement, Robeco promotes companies that are pounding out inequality on boards but also using other tools to fully leverage the power of women and other “marginalized” assets to build robust institutions and robust returns.

Footnotes

1 Council of the European Union, Gender balance on corporate boards. Women on Boards are non-executives directors. Women in executive management are categorized as executive directors.

2 Eurostat, March 2022

3 European Institute for Gender Equality: Survey of the largest publicly listed companies in the EU. June 2022.

4 European Institute for Gender Equality, Economic case for gender equality in the EU

5 2022 Report on Gender Equality in the EU

6 Latura, Audrey & Weeks A.C. “Corporate Board Quotas and Gender Equality Policies in the Workplace.” The American Journal of Political Science. 2022.

7 OECD 2022 Gender Report

8 “Big Investors are better than quotas at getting more women on boards.” Bloomberg. 22. November 2022.

9 “How Nasdaqs new board diversity requirements will move the market.” Factset. 20. October 2021.

10 “Do Quotas for Corporate Boards Help Women Advance?” University of Chicago, Booth School of Business Review. 15. June 2015.

11 Ibid.

12 Credit Suisse Research Institute, CS Gender 3000 in 2021 Report.

13 Less employee turnover and discrimination controversies when women are in senior management. Source: Morningstar. “Quotas for Women Aren’t Enough to Protect Against Human Capital Risks.” 28 February 2022. Diverse management linked to innovation and revenues. Source: BCG, “The Mix that Matters.” 26 April 2017.

14 Global 2021 statistics from S&P Global. “Women CEOs Leadership for a diverse future.” EU statistics from OECD 2022 Gender Report. As per a Catalyst report, women CEOs held 8.2% of CEO positions at S&P 500 companies in both 2021 and 2022. G20 data from UN Sustainable Stock Exchanges Policy Brief, “Gender Equality on Corporate Boards.” 2021.

Important information

The contents of this document have not been reviewed by the Securities and Futures Commission ("SFC") in Hong Kong. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. This document has been distributed by Robeco Hong Kong Limited (‘Robeco’). Robeco is regulated by the SFC in Hong Kong. This document has been prepared on a confidential basis solely for the recipient and is for information purposes only. Any reproduction or distribution of this documentation, in whole or in part, or the disclosure of its contents, without the prior written consent of Robeco, is prohibited. By accepting this documentation, the recipient agrees to the foregoing This document is intended to provide the reader with information on Robeco’s specific capabilities, but does not constitute a recommendation to buy or sell certain securities or investment products. Investment decisions should only be based on the relevant prospectus and on thorough financial, fiscal and legal advice. Please refer to the relevant offering documents for details including the risk factors before making any investment decisions. The contents of this document are based upon sources of information believed to be reliable. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Investment Involves risks. Historical returns are provided for illustrative purposes only and do not necessarily reflect Robeco’s expectations for the future. The value of your investments may fluctuate. Past performance is no indication of current or future performance.