Fixed income

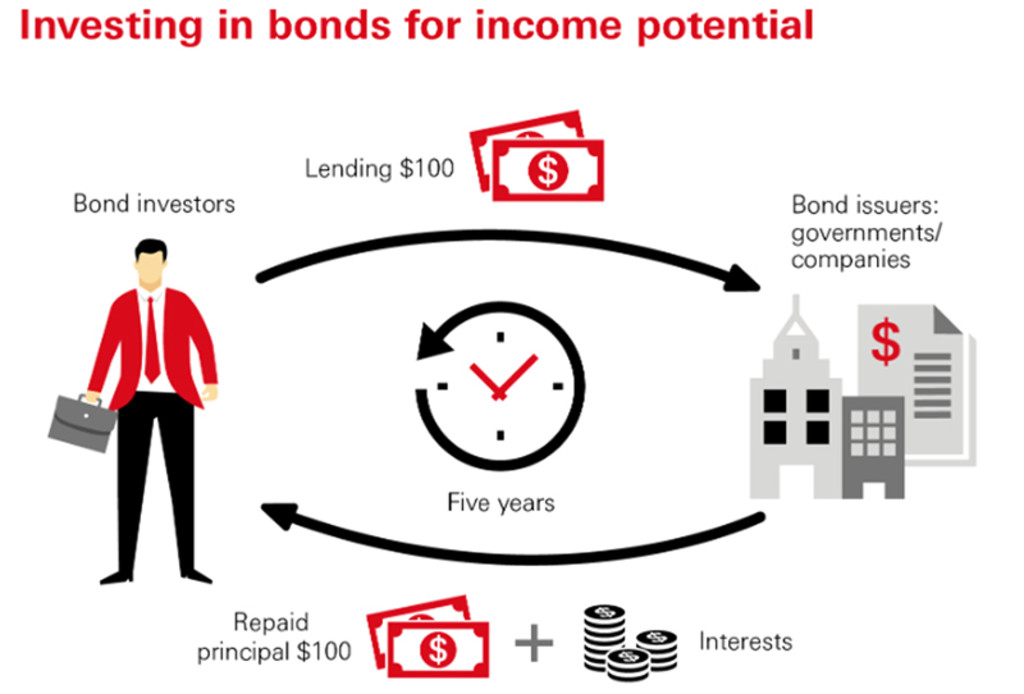

Credit income refers to the return generated from investing in credit instruments, such as corporate bonds, government bonds, and other fixed income securities. It typically comes from two main sources: coupon payments (interest paid by the issuer) and potential capital appreciation from price movements in the bonds.

Key characteristics

Income generation: Credit income provides regular interest payments, making it a key component of income-focused investment strategies.

Variety of credit instruments: Investors can generate credit income through a broad range of fixed income securities, including investment grade bonds, high yield bonds, and hybrid instruments like CoCo bonds.

Risk-return balance: Credit income strategies can be tailored to match an investor's risk tolerance, from stable investment grade bonds to higher yield opportunities in lower-rated securities.

Credit income plays a vital role in diversified portfolios:

Steady cash flow: It provides a predictable income stream, especially valuable in low-interest-rate environments.

Portfolio stability: Bonds and other credit instruments can help stabilize portfolios by offsetting the volatility of equity markets.

Yield enhancement: By taking on appropriate levels of credit risk, investors can enhance their portfolio's yield.

A long history of innovation

Who invests in credit income?

Credit income strategies are popular among income-focused investors, who prioritize regular cash flow and capital preservation. Active managers also seek opportunities in credit markets to capture additional yield and benefit from market inefficiencies.