Portfolio Manager

• Monthly outlook

The strange case of Dr Equity and Mr HY-de

A rare disconnect between the likely performance of equities and high yield bonds means stocks will be greatly preferred going into 2026, says multi-asset investor Mathieu van Roon.

Autoren/Autorinnen

Zusammenfassung

- Equities and high yield bonds are normally on the same side of the risk coin

- Stocks are expected to see robust earnings growth in a positive macro backdrop

- HY bonds face rising credit stress, a demand imbalance and super-tight spreads

He says the different sides offered by what is usually the same risk-on or risk-off trade draws a parallel with the gothic horror story ‘The Strange Case of Dr Jekyll and Mr Hyde’. In the 19th century tale, the mild-mannered scientist Dr Jekyll drinks a potion and turns into the monstrous Mr Hyde. Both are the same man, but with very different sides.

“As we near the end of the year and start to look ahead to 2026, we see a clear bifurcation in the downside versus the upside risks between equity and equity-like asset classes,” says Van Roon, Portfolio Manager with Robeco Investment Solutions.

“Whereas normally we expect high yield bonds and equities to be on the same side of the risk on/off coin, and to perform in the same type of circumstances, for 2026 we fear high yield could show its ugly side. You might call it the Strange Case of Dr Equity and Mr HY-de.”

Van Roon says the bifurcation lies in the macroeconomic factors facing each asset class that will turn out positive for Dr Equity and negative for poor Mr HY-de. “On the one hand, US and European equity markets and large investment grade corporates are full of optimism, fueled by robust earnings, aggressive buybacks and the promise of AI-driven productivity gains,” he says.

“On the other hand, the real economy – especially in the US – and leveraged high yield issuers are burdened by deteriorating fundamentals and increasing macro risks.”

“This dichotomy in views on the asset classes is striking, as historically, high yield bond and equity prices have had a strong correlation, with both dependent on positive economic and company growth expectations.”

“But in 2026, the macro and technical environment might worsen for high yield, whereas equity has a bigger chance to continue to ride the wave of earnings strength and technological optimism, similar to the last throes during the tech bubble of the late 1990s.”

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Growth from spending and AI

The giant economies of both the US and Europe are expected to grow in the coming year, though for different reasons. Europe’s growth is related to fiscal spending, including on defense and infrastructure, and pent-up savings. The growth expectation in the US is driven by AI-related capital expenditure, and potential productivity gains from AI and upper-income consumption. This is further aided by fiscal support from the One Big Beautiful Bill Act and bumper tax refunds.

“This growth is, however, not without tension,” Van Roon warns. “President Trump’s tariffs are expected to impact US growth and/or company earnings, while inflation is expected to remain sticky. The Fed is in a tough position to remain either too restrictive in an already fragile labor market, or to potentially start too soon with easing, which could un-anchor inflation expectations.”

“Add to that political uncertainty with mid-term elections coming up in November 2026, and a potential change at the Fed’s helm when Chairman Jerome Powell’s term ends in May. The aforementioned AI boom is also expected to continue to reshape the labor market, as fewer people are needed to produce the same output.”

“These developments can impact consumer spending negatively. Alternatively, efficiencies will lead to more leisure time; Henry Ford used the efficiency of car assembly lines to allow workers the concept of a ‘weekend’, in the belief that this would boost car usage and adoption.”

Dr Equity

Given this backdrop, Van Roon says US equities are expected to benefit from robust earnings growth, seen at about 14% for the S&P 500, with half of that coming from sectors outside the tech sector. EU companies stand to gain as well, due to fiscal stimulus and the broadening of growth beyond the US. The AI productivity gains are expected to broaden out over the other sectors, such as healthcare and retail, thus supporting the rally.

“Current valuations are high, but thanks to strong company fundamentals (margins, free cash flows, low leverage levels), they are not at extremes,” Van Roon says. “Last but not least, the flows into equities remain robust and diversified, with retail, passive and institutional investors across the spectrum continuing to buy stocks.”

Mr HY-de

This contrasts quite starkly with the high yield bond market. “Whereas the outlook for equities is rather optimistic, the outlook for high yield is much more cautious,” Van Roon says. “Compared to large investment grade companies, the lower-rated, smaller and more highly leveraged companies are struggling with tighter lending standards and rising refinancing rates.”

“The macro landscape with more political/tariff/inflation uncertainty and AI-related job cuts is expected to weaken consumer demand, which these types of companies rely on.”

“Supply-wise, a net increase is expected, driven by AI-related capex, M&A and refinancing, whereas it is expected that inflows are unlikely to keep pace with this supply. Recent worries about rising stress in private credit might spill over into public high yield markets, especially if sector-specific shocks (such as AI disruption in software) trigger a negative feedback loop, where bonds with lower ratings such as B or CCC are more vulnerable.”

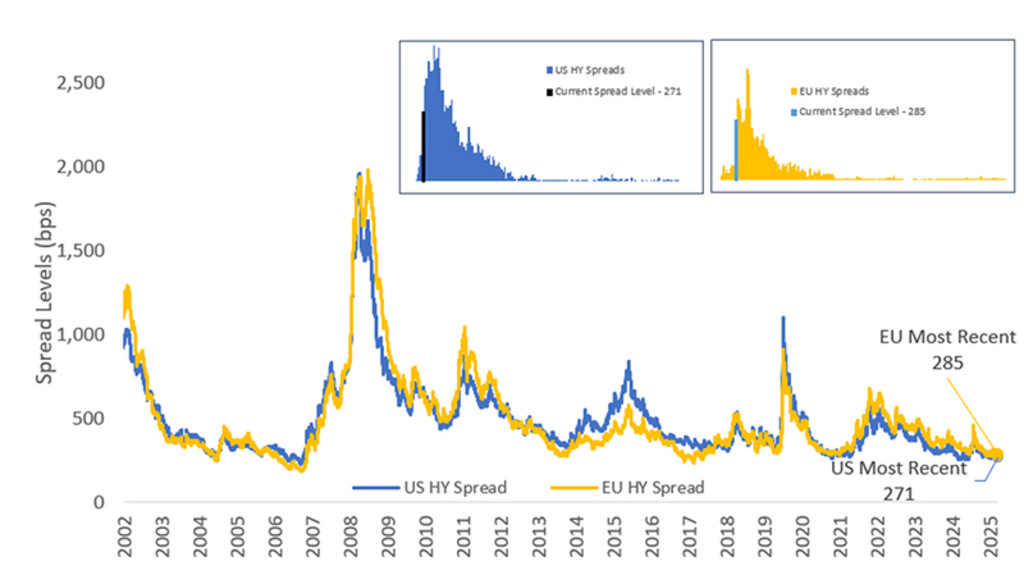

“Just as in equities, current valuations in high yield are rich, as spreads are hovering around historically low levels.” This can be seen in the chart below.

Figure 1 – Historic high yield spread development

Source: Bloomberg, Robeco

Brighter outlook for stocks

“Investors are not asking for much additional compensation to invest in high yield bonds. While further spread tightening is possible, it is relatively limited. The attractiveness of this asset class is thus mostly the sizeable carry returns gained from holding these bonds.”

In all, Van Roon says the trade-off between risk and returns is much more constructive for equities than for high yield. “The tight spreads, rising supply and challenging macro environment make us more cautious for high yield, but the asset class can still deliver attractive carry returns going forward, especially relative to other fixed income sectors,” he says.

“Equities stand to benefit from fiscal support, AI-driven earnings and robust flows, and have more upside. We thus take sides with ‘Dr Equity’.”