Portfolio Manager

• Monthly outlook

Why markets are watching rising defense spending

Higher defense spending will be closely watched by markets for its impacts on government budgets and across asset classes, says multi-asset investor Aliki Rouffiac.

Auteurs

Samenvatting

- Wars in Ukraine and Iran put focus on the high cost of security independence

- Rising budget deficits will have repercussions for sovereign bonds and rates

- Equity markets in sectors such as cybersecurity and rare earths can benefit

As the cost of security independence in the West starts to run into the trillions, investors will be wary of their repercussions for budget deficits and future interest rate policy, putting a focus on future sovereign bond values, says Rouffiac, Portfolio Manager with Robeco’s Investor Solutions multi-asset team.

Many stock markets sectors can though continue to benefit, such as cybersecurity and rare earths, following a strong rise in the stocks of defense-related manufacturing companies in the past year, she says.

“After a year of tariff wars, geopolitical risks have risen again, as the start of the US-Iran war in February accelerated the focus back toward defense,” she says. “The great reset that is taking place has meant that countries are already adapting to numerous evolving trends.”

“Security independence remains high on the agenda, and more resilient supply chains are needed to navigate an uncertain economic landscape. Deglobalization and reshoring are reshaping the capacity potential of the manufacturing sector, which is absorbing this higher spending.”

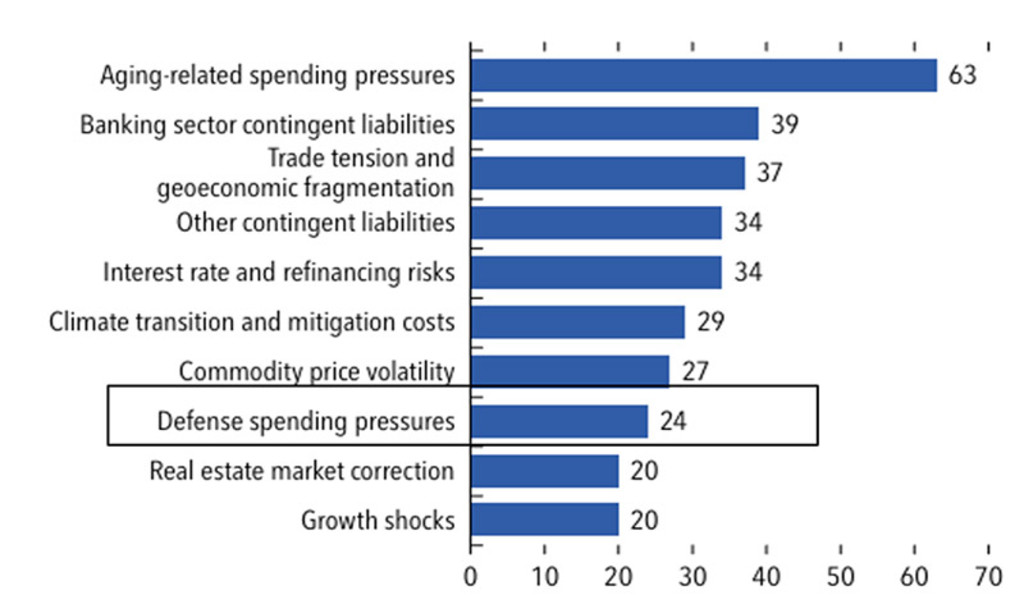

“Against this evolving backdrop, military spending by European allies and Canada (based on the NATO defense spending tracker) has outpaced previous expectations, increasing by 20% in 2025. Defense spending pressure is now one of the top ten fiscal risks identified for advanced economies, seen as a problem in 24% of countries.”

Figure 1: Top fiscal risks identified in advanced economies (percentage of countries)

Source: IMF Fiscal Monitor April 2026. IMF staff calculations are based on data from 32 IMF staff reports on advanced economies published in 2025 using the Fiscal Monitor AI Analyst, a custom large-language-model pipeline.

Much of the likely impact is country-specific, given that nations in eastern Europe closer to the border with Russia are spending far more than their counterparts further west, relative to GDP. Countries with a relatively strong domestic defense industry like France and the UK also tend to spend more.

“Notably, the fiscal expansion needed to accommodate higher spending is unlikely to be transitory in Europe, where defense expenditures tend to be rigid,” Rouffiac says. “For now, the activation of national escape clauses has provided some leeway to European countries to circumvent fiscal rules constraints, but the potential remains for structural increases in debt levels if the spending is not offset by other policies.”

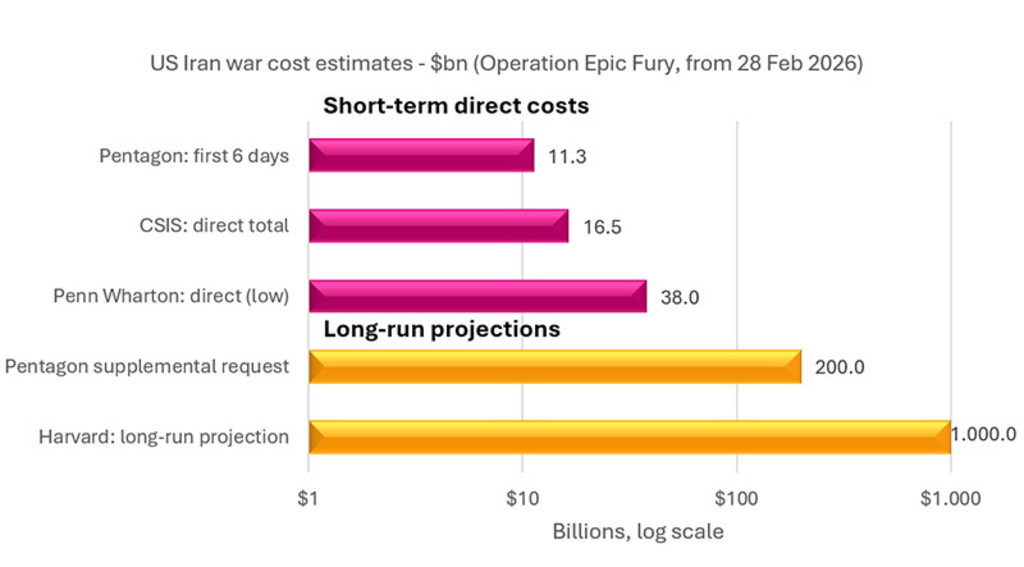

In the US, estimates for the cost of the war in Iran so far have been in the region of USD 30 billion and counting, while its latest proposed defense budget for 2027 is USD 1.5 trillion, which is higher than the GDP of most European economies.

Figure 2: The costs of the war in Iran are rising at a time when deficits are already high

Source: Pentagon, CSIS, Penn Wharton, Harvard, May 2026.

Implications for rates

“This level of spending constitutes an uplift from the previous years’ projections and increases the uncertainty around the future levels of deficit, which is likely not factored into current interest rates,” Rouffiac warns.

“Higher spending will have implications for inflation and rates expectations, where investors are likely to differentiate between countries that run higher fiscal deficits and those that don’t. In the same vein, the recent oil shock has added a headwind, though this may be seen as short-lived and transitory under a peace deal scenario.”

“In the meantime, the risk of higher-for-longer rates has supported higher premiums in government bonds, particularly for countries that are energy importers. This has brought to the fore an additional burden to government budgets, at a time when fiscal expansion is needed to support higher defense spending goals.”

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Boost for manufacturing

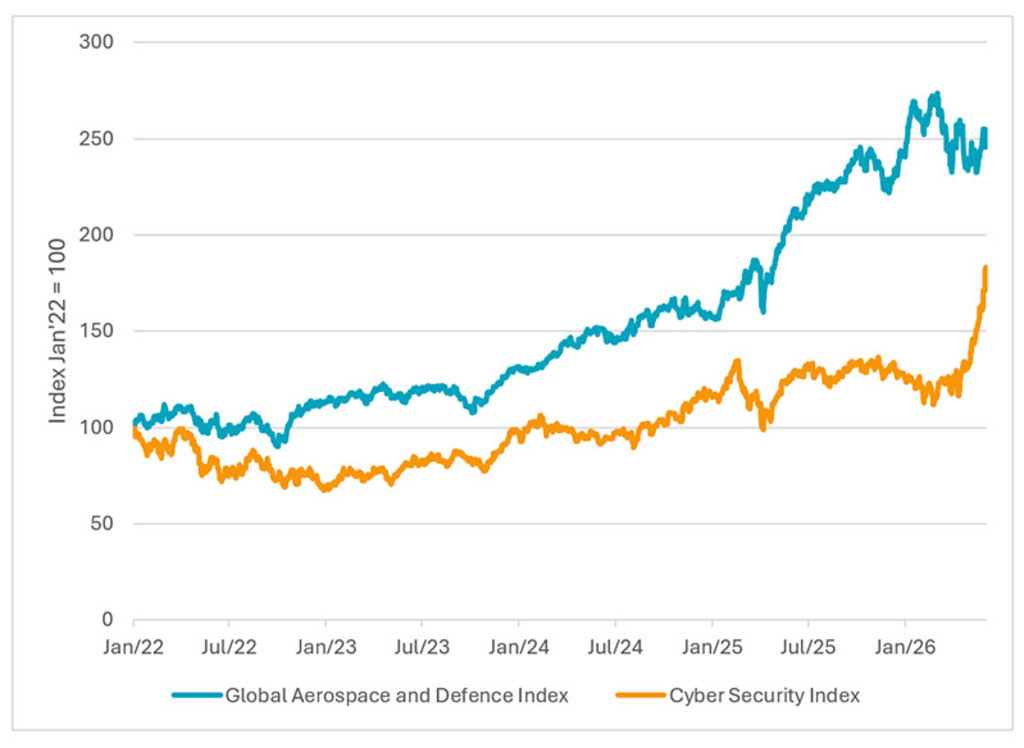

One of the beneficiaries of higher spending has been manufacturing, which has the potential to support future growth in the labour market across Europe and has led to a rally in aerospace and defense stocks since the start of 2025. Future growth areas can be seen in cybersecurity, critical minerals and rare earths, and energy self-sufficiency, Rouffiac says.

“More efficient and faster procurement processes – particularly in Europe – and innovations are needed to support higher demand and the modernization of the defense ecosystem,” she says.

“As such, tech innovation and private capital will be crucial in areas like artificial intelligence, quantum technologies and next-generation communication networks, that NATO has identified as having the greatest potential in transforming the future of warfare, in which cybersecurity takes a center stage.”

“Markets are already factoring in this trend, with the global cybersecurity stock index up 36% since the beginning of the year. On the other hand, global aerospace and defense equity returns have been muted after a very strong 2025, which saw them delivering performance in excess of 50%. Still, earnings growth projections continue to be supportive, despite higher valuations.”

Figure 3: Cybersecurity stocks have reaped the benefits

Past performance is no guarantee of future results. The value of your investments may fluctuate.

Source: Robeco, Bloomberg. Data as at June 2026.

Another beneficiary has been rare earth metals, due to their use in advanced defense systems, which has boosted their prices.

“But as we wrote on our previous theme, ‘Energy self-sufficiency in the age of shocks’, greater reliance on critical mineral sourcing and infrastructure expands the concept of security, and requires supply chain diversification to support future growth and investment opportunities,” Rouffiac concludes.