Strategist

• Insight

Warsh's first Fed meeting: A new era for Fed communication?

Kevin Warsh wasted little time putting his stamp on the Federal Reserve.

Authors

Strategist

Strategist

Top keywords

Summary

- Committee split on whether to hike in 2026

- Expect the Fed to hold rates steady

- Labor market stabilizing

At his first FOMC meeting as Chair, the policy decision itself attracted less attention than the changes in how the Fed communicated it. The statement was cut roughly in half, forward guidance was removed, and Warsh chose not to publish his own interest rate projections. Together, the moves suggest a different communication philosophy may be emerging at the Fed.

What became clear at Warsh's debut meeting is that he is not a fan of extensive forward guidance. That philosophy was immediately reflected in a statement that was roughly half the length of previous ones and the removal of explicit guidance on the future path of policy.

The changes appear to be more than a stylistic preference. In our view, Warsh intends to fundamentally change how the Fed communicates. He sees little merit in forward guidance, believing it was one of the main reasons the Fed was slow to raise rates during the 2021-22 inflation shock. The shorter statement is a positive development, reducing the need for markets to scrutinize every word the Fed uses to describe the economy.

Providing less guidance could ultimately lead to more predictable policymaking

Warsh also chose not to publish his own interest rate projections, underlining his reservations about the current Summary of Economic Projections (SEP). We interpret this as another signal that he wants to change the current framework. Rather than relying on individual policymakers' point estimates, the Fed could move toward a more scenario-based approach, similar to that used by the ECB and the Bank of England. While this is still a form of forward guidance, it focuses less on predicting the exact path of rates and more on explaining how policy is likely to respond under different economic outcomes.

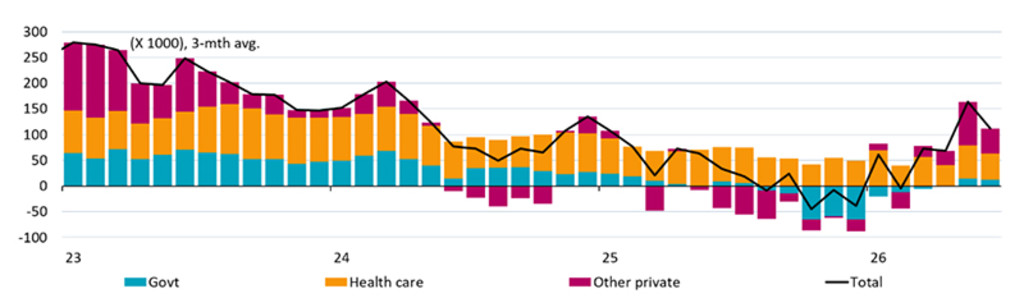

Monthly US Non-Farm Payrolls growth

Source: Bloomberg, Robeco, 6 July 2026

Credibility first

Warsh struck a distinctly hawkish tone throughout the press conference, repeatedly stressing that price stability remains the committee's primary objective. That emphasis appears to have been deliberate. In our view, the hawkish communication helped establish his inflation-fighting credentials while also demonstrating independence from the White House. Markets viewed that message as credible: inflation expectations implied by inflation-linked bonds declined following the press conference.

A Fed driven by data, not promises

Warsh also announced five committees to review aspects of Fed policymaking, ranging from communication to the data used in policy decisions. While these reviews suggest institutional change may lie ahead, they do not necessarily imply a different policy outlook.

Ultimately, the data will continue to drive decisions. We are paying particularly close attention to developments in the labor market, while lower energy prices and a softer June employment report reduce the immediate pressure to tighten policy further.

What it means for investors

For now, we continue to expect the Fed to remain on hold, even though markets have priced in at least one additional rate hike this year.

Removing forward guidance is likely to increase volatility at the front end of the Treasury curve, as every policy meeting effectively becomes live. However, Warsh has also emphasized that the Fed will not react to individual data releases, but instead focus on broader trends in the economy. Paradoxically, providing less guidance today could ultimately lead to a more predictable policy framework over time.

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.