Impact Specialist

• Insight

Denmark continues to dominate country ESG rankings

In this update, we learn that emissions, renewables and water management were decisive for both top- and lower-tier performers. In addition, country case studies illustrate that poor ‘G’, amplifies poor ‘S’ and ‘E’. Finally, cyberattacks can cause enduring economic and social damage, posing serious risks to sovereigns.

Authors

ESG Analyst and Impact Specialist

Top keywords

Summary

- Environmental policies weigh on ESG leaders

- Country cases show bad governance is bad news for ESG performance

- There’s now a way to measure a country’s resilience to cyber threats

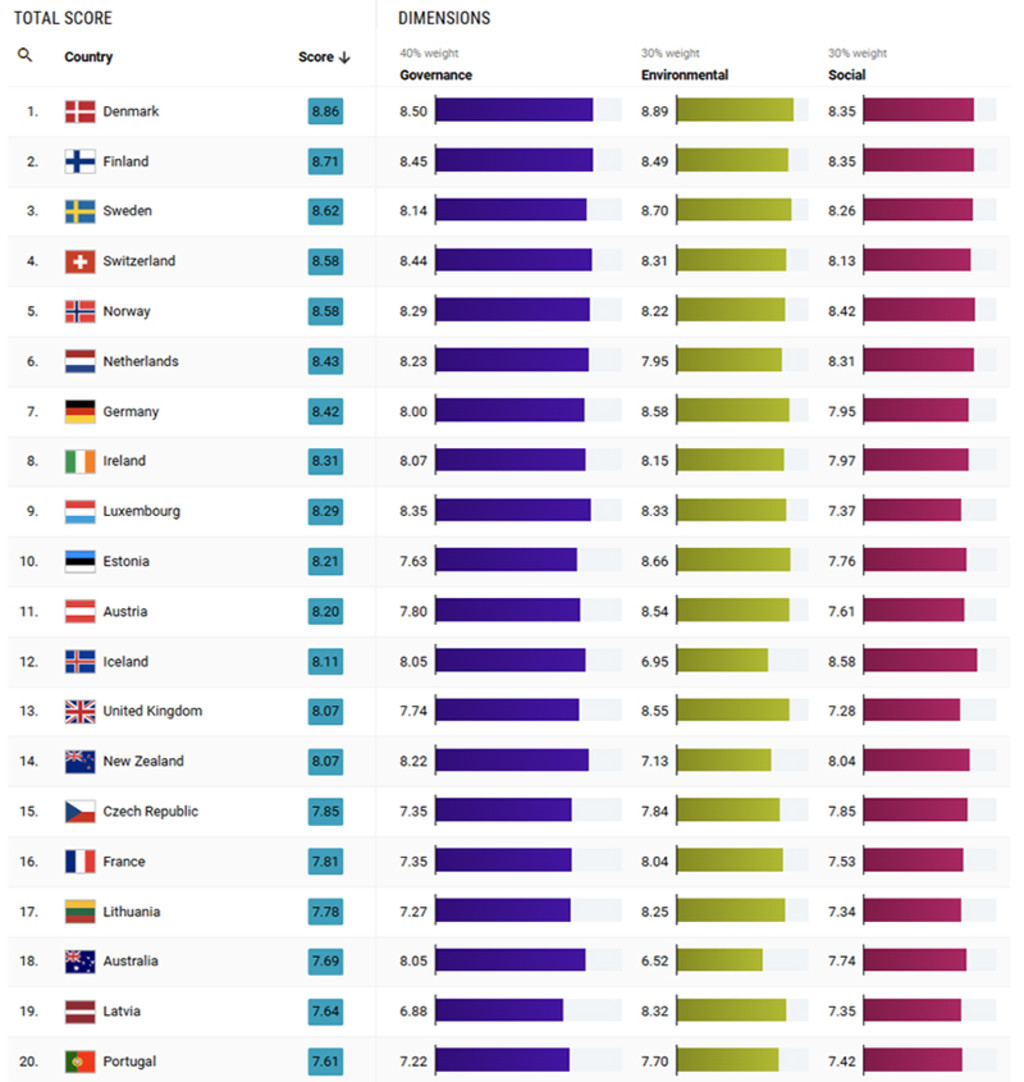

Denmark maintains its ESG leadership, topping Robeco’s Country ESG rankings (click link for complete rankings) for the fourth consecutive time in two years. As in the past, Scandinavian countries had a strong showing which (along with Switzerland) rounded out the top five slots.

ESG performance for those on the leaderboard was not off the charts, however, with most seeing declines in their environmental scores. Denmark and Sweden saw slowdowns in the uptake of renewables as a share of their overall energy mix. Norway lost ground on the management of water stress and climate risks. Runner-up Finland was the only country with a slight increase in environmental scores, due to higher renewable additions and better water use.

Figure 1 - Country ESG score leaders

Source: Robeco, April 2026.

Major govy issuers show mixed (and surprising) results

Scores among the world’s largest sovereign debt issuers continue to diverge. Japan’s ESG score (7.46 of 9.0) slightly declined, while the US score (6.61 of 9.0) remained largely stable. For Japan, reductions in climate and energy criteria were to blame.

Ironically, in the US, lower governance marks (from higher corruption and weaker institutions) were offset by higher environmental scores resulting from Liberation Day tariffs, which reduced CO2 emissions associated with the production of imported goods.

China’s ESG score improved slightly thanks to efforts to improve extinct species, an indicator of biodiversity health.

Scores around the globe

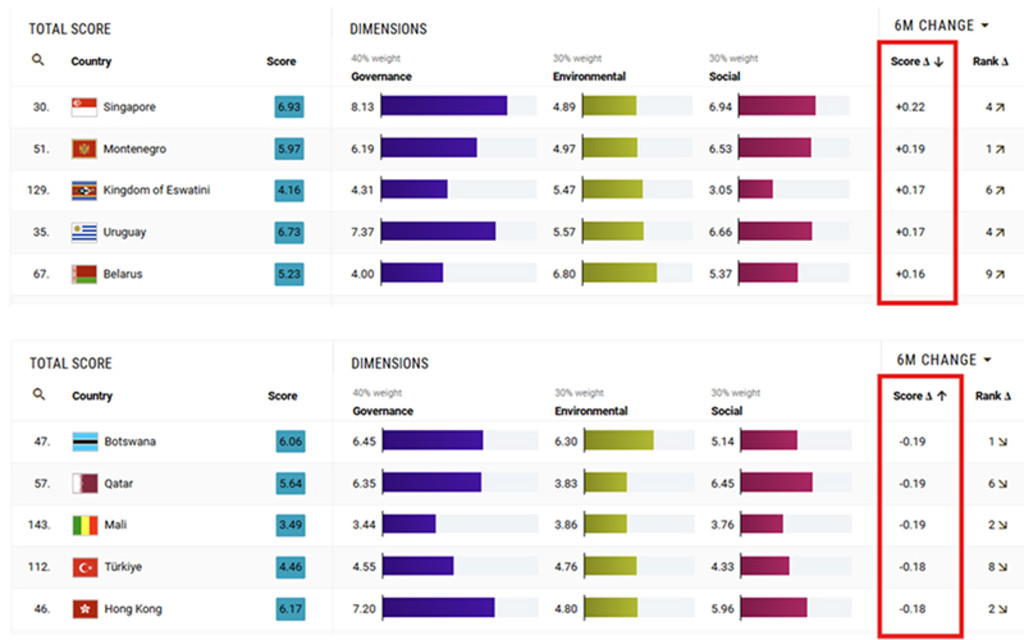

Several emerging markets recorded notable gains in the ranking. Singapore posted the largest absolute score increase due to better water management practices (see Figure 2). Conversely, weaker environmental scores weighed on countries with the largest score decreases including Botswana, Qatar, Mali, Türkiye and Hong Kong.

Figure 2 - Top five countries with the largest gains and losses

Source: Robeco, Country ESG scores, April 2026.

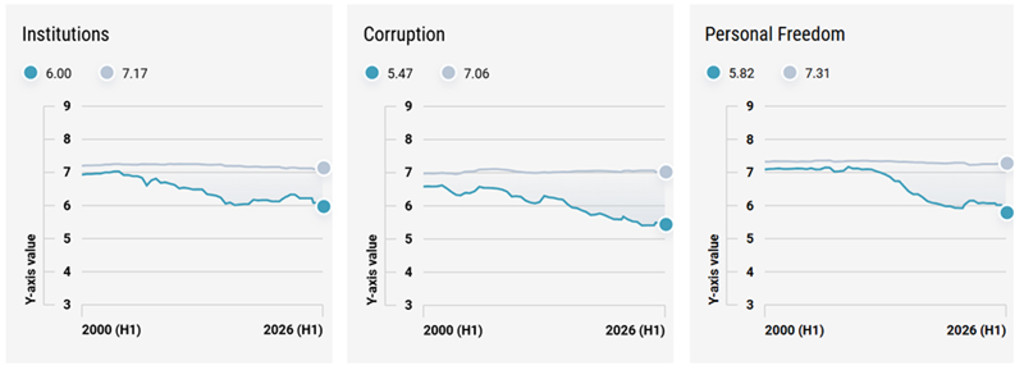

Obstructing Orban’s orbit

For nearly two decades, Viktor Orban and his Fidesz party dominated Hungary’s political scene. Once seen as a freedom fighter, championing Western ideas, his style became increasingly authoritarian, anti-democratic and corrupt with each passing year. His grip on power ended abruptly in early 2026, when he was voted out of office in spectacular style by Peter Magyar’s Tisza coalition.

However, desired reforms may not come as quickly as his fall, as Orban’s cronies still staff key institutions in the courts, media, and banking often with long-dated appointments. The people have spoken and a clear mandate has been delivered. With Orban out of orbit, progress may be slow, but at least things are now on a positive trajectory.

Figure 3 – Orban’s ESG legacy

Hungary’s Institutional, Corruption, and Personal Freedom scores 2000-2026. Hungary (blue) vs. EU peers (gray)

Source: Robeco, April 2026

Peru’s perilous plummet

Once a stable ESG performer in the LatAm region, Peru’s standings have slipped of late. The country’s social score has suffered due to widespread protest following chronic crisis of leadership. The country has cycled through several presidents, multiple cabinet reshuffles, and endless friction between branches of government. Corruption scandals of political elites and judges have stoked further distrust.

The chaos highlights deep seated societal tensions related to inequalities, exclusions, and access to basic services. Progress on poverty has stalled, informal work arrangements abound, and weak public services, especially in healthcare and education, are hampering human capital development.

The natural environment is also experiencing troubled waters. Peru is exposed to physical climate risks – including flooding, droughts, and El Niño related shocks – which threaten agricultural production and infrastructure. Weak governance has meant less enforcement of environmental protection, particularly in relation to illegal mining, deforestation, and water pollution. It’s a clear case of how weak governance at the top can intensify social and environmental problems on the ground (see Figure 4). Unfortunately, without some sort of immediate lifeline, Peru’s ESG performance is likely to keep sinking.

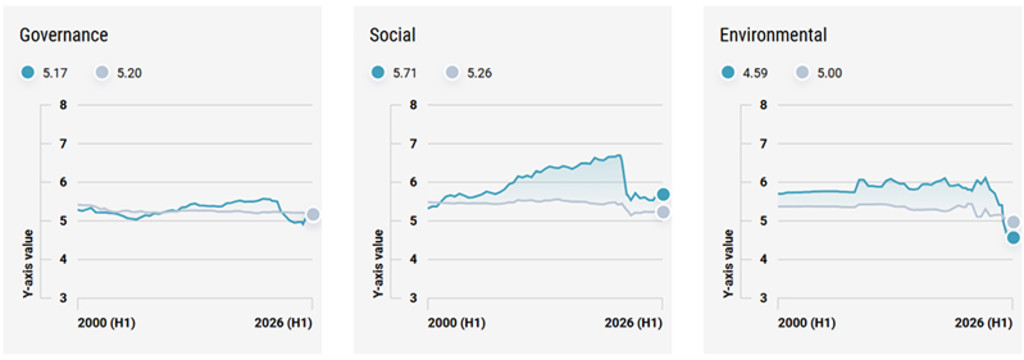

Figure 4 – A country in need of more ‘G’- force

Peru’s Governance, Social and Environmental scores, 2000-2026. Peru (blue) vs. Latin American peers (gray).

Source: Robeco, April 2026

Thematic focus – Cybersecurity

Cybersecurity has become an increasingly material component of sovereign ESG risk, reflecting the growing dependence of governments and economies on digital infrastructure. Large scale cyberattacks have resulted in multi billion dollar losses globally, with governments often bearing indirect fiscal costs through emergency response spending, system reconstruction, litigation, and lost productivity.

The 2017 ‘NotPetya’ cyberattack on Ukraine’s public and private sector systems is widely cited as one of the most destructive, with global damages exceeding USD 10 billion. Moreover, the ‘WannaCry’ ransomware attack in the UK showed attacks were also destructive to public health on a massive scale. It infected National Health Service’s (NHS) computer systems leading to canceled medical procedures and emergency service disruptions.

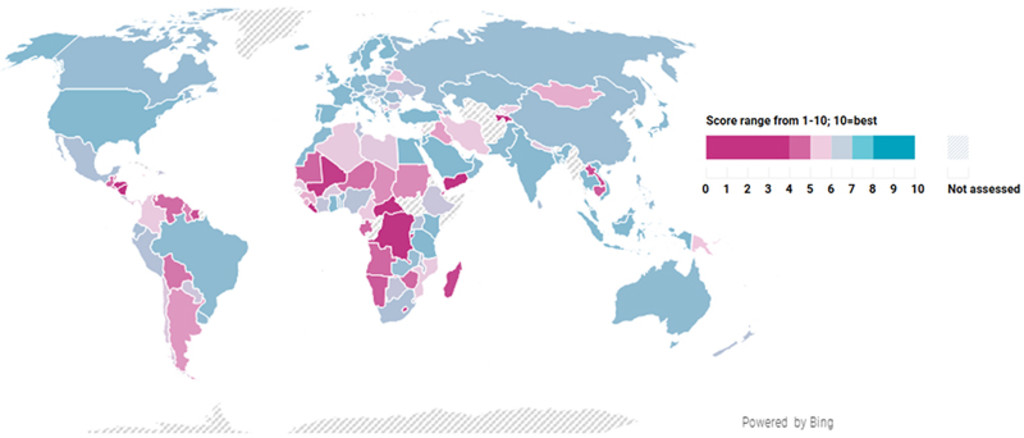

The Country ESG framework is now integrating cybersecurity as a factor in ESG performance using data from the Global Cybersecurity Index (GCI) developed by the International Telecommunication Union (ITU), a UN agency overseeing global digital networking standards.

Figure 5 – Global Cybersecurity Index world map

Lower scores (pink gradients) indicate that countries are more vulnerable and less prepared for cyber risks.

Source: Global Cybersecurity Index, International Telecommunication Union, April 2026.

Notably, cybersecurity isn’t directly correlated with high GDP. Advanced and emerging countries perform well, from Finland and Italy to Egypt and Indonesia. Though diverse in economy and culture, a characteristic common to them all is that they tend to exercise a whole of government approach, including dedicated cyber agencies, robust legal frameworks, mandatory incident reporting, and strong international cooperation.

Concerningly, many lower-tier performers have rapidly expanded digital services without commensurate investment in cybersecurity governance, leaving them dangerously exposed.

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.