Strategist

• Monthly outlook

The profits party peaks, but the aftermath looks benign

Corporate earnings which have soared in the Covid-19 recovery are now flattening out. But the future still looks bright for stocks, says strategist Peter van der Welle.

Authors

Summary

- Lower consumer confidence and elevated input costs set to dent Q3 profits

- Brighter outlook as labor market pressures ease and people return to work

- Past and future fiscal thrust to have positive effect on economic activity

It’s been a record-breaking period for the companies in the S&P 500 as vaccination success allowed business activity to recover from the lows of the lockdowns. Year-on-year earnings growth for the index constituents reached a record high of 97% in the second quarter, according to Refinitiv data.

Some 88% of S&P 500 members managed to beat prior earnings expectations, sending the index to a succession of record highs. The party is now over, though there remain plenty of tailwinds to keep stocks sweet, says Van der Welle, strategist with the Robeco multi-asset team.

“With the slowdown in macroeconomic momentum on the back of rising Covid-19 cases denting consumer confidence lately, the effect of supply-related production curbs in some sectors as well as rising input costs makes it likely that earnings growth will decelerate in the third quarter,” he says.

“An early-cyclical peak in global earnings growth is also suggested by the shape of the yield curve. The spread between the 10-year and 2-year US Treasury yield typically leads the earnings cycle. The recent flattening of the yield curve and declining term premium suggest the tailwinds for earnings growth will weaken in the medium term, with the early-cycle peak in EPS growth already behind us.”

“However, it is unlikely that this weakening from historically high levels in the coming quarters will culminate in a stalling of global corporate earnings growth on a 6-12-month horizon.”

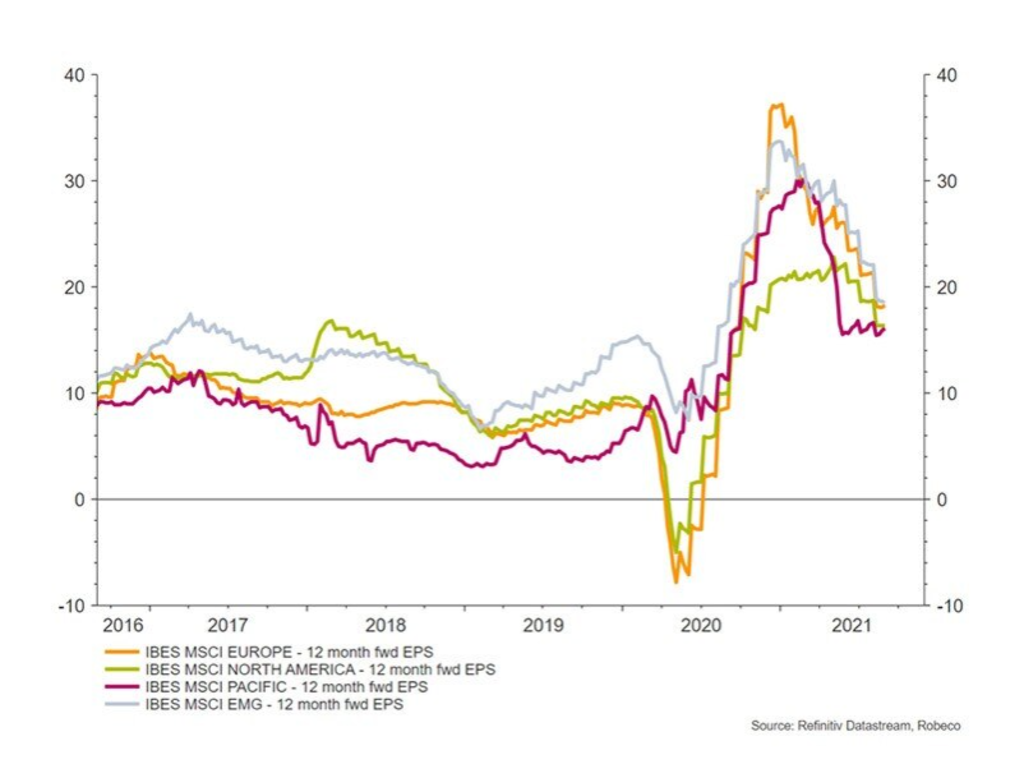

12-month forward earnings per share growth predicted for the world’s major markets.

Source: Refinitiv Datastream, Robeco, 2 September 2021.

Three reasons to cheer

Van der Welle says there are three reasons why earnings growth will flatten out, but won’t cause too many sleepless nights for investors.

“First, supply-related curbs to production will ease as labor supply increases, with furloughs and stimulus checks now being phased out in many countries,” he says. “This is lowering pressures on labor and recruiting costs as people start to look for jobs again.”

“In addition, some inputs in the commodity space such as lumber and copper have already dropped significantly from their peaks in the first half of 2021, benefitting the housing sector.”

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.

Spending power still strong

“Second, the recent decline in consumer confidence which could impact top-line growth in Q3 will likely prove to be temporary, as the Delta variant of Covid-19 proves to be manageable this winter, and as lockdown intensity is lowered again in early 2022.”

Consumer spending power is still strong as household savings ratios are still elevated from money that could not be spent during the lockdowns, he says. Affordability ratios – defined as the difference between interest owed as a proportion of net income – are also healthy.

“There is also a noticeable absence of a household deleveraging cycle – unlike what we saw following the global financial crisis – which means the spending power of consumers will prove resilient,” Van der Welle says.

Massive fiscal thrust

“Third, the massive fiscal thrust we have observed in major developed economies over the past year will still have positive lagged effects on economic activity.”

“In Europe, the first tranche of the EU Recovery Fund released in July will also stimulate regional economic growth in the medium term.”

“In short, from a macro point of view, it is likely that above-trend GDP growth in the next 12 months will persist in developed economies, leaving earnings growth well into the double digits.”

Global growth forecasts

Meanwhile, the IMF expects 4.9% global GDP growth for 2022, which would be consistent with decelerating EPS growth compared to what was achieved as the mass vaccination programs began in 2021, Van der Welle says.

“But it would still leave us at the upper range of the distribution from a historical perspective, with EPS growth in the 20%-30% bracket,” he says.

“This view is corroborated by our bottom-up analysis, as corporate analysts are expecting 12-month forward EPS growth in various regions to be close to but below 20% at this point in time. So, the profit party peaks, but the aftermath looks benign.”