9 questions about credit investing | Question 7

The 2023 US banking turmoil created the most significant upheaval in financial systems since the global financial crisis. This impacted risk perceptions, credit market valuations and regulatory dynamics. More importantly, it raised questions about the stability of the banking sector. Although much of this upheaval seems well and truly in the past, the question remains: Are European financials undervalued opportunities or value traps with hidden fundamental issues?

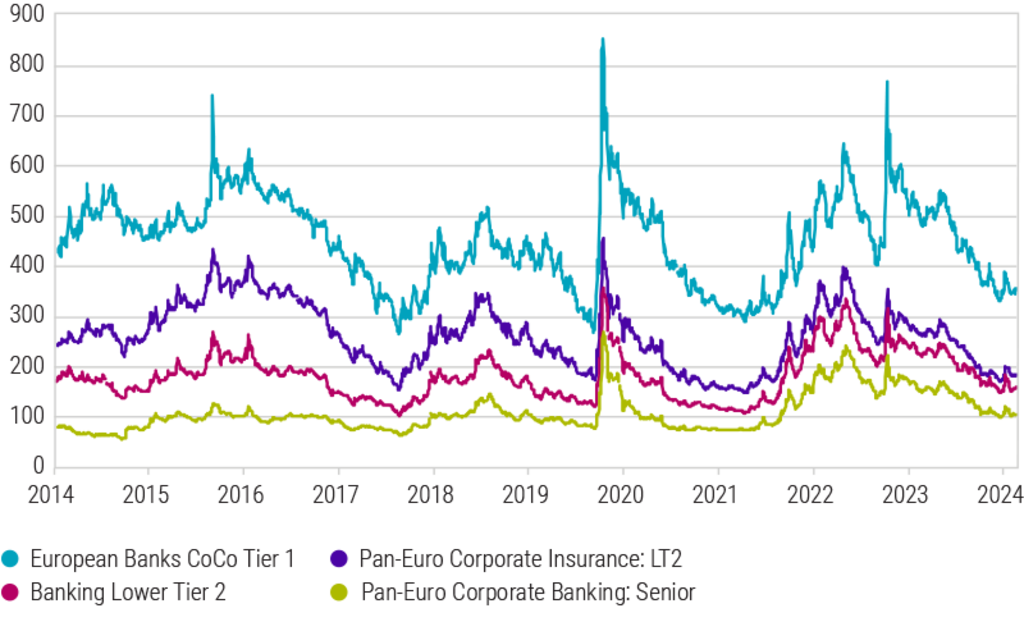

Although financial spreads have tightened since the concerns with US regional banks and the write-down of AT1 CoCos issued by Credit Suisse in March 2023, we believe European bank and insurance debt still provides an attractive premium over corporate debt. This is illustrated in the figure below that shows the credit spread for different types of subordinated bank and insurance bonds.

Despite the recent market rally, financial spreads are still trading wide compared to the sector's median levels, as well as to corporate spreads. Several factors contribute to this phenomenon. Firstly, the banking sector is a higher beta sector and therefore is more volatile and reacts more sensitively to market movements than the average industry. Consequently, concerns about the growth outlook in Europe tend to widen financial spreads, as investors worry about potential credit losses.

Additionally, the European growth outlook has been more sluggish compared to the US, further contributing to the expansion of financial spreads. Furthermore, specific concerns about individual banks, such as the case with Credit Suisse and the US regional banks last year, or banks overly exposed to commercial real estate, can lead to wider financial spreads. Lastly, the premium in bank debt is partly due to the substantial issuance of bank debt in recent years relative to corporate debt.

Financial spreads

Source: Robeco, Bloomberg. As of 31 July 2024. Indices used: Bloomberg European Bank AT coco index. Bloomberg European Bank LT 2 index. Bloomberg European Bank Senior Debt. Bloomberg European Insurance debt index.

The best risk-reward in financial institutions

Firstly, let’s examine the fundamentals of the European banking sector. Most European banks have benefited significantly from the recent rise in interest rates, resulting in increased earnings. While interest rates have come down somewhat, banks can still rely on other sources of income to support their earnings. European banks maintain robust capitalization levels, allowing them to absorb losses before capital ratios become critical. Overall, asset quality remains strong.

However, as credit investors, it is crucial to conduct thorough due diligence. We avoid banks that are overly exposed to commercial real estate, such as certain German specialist banks with concentrated CRE loan portfolios or less-regulated regional banks in the US. Our preference lies with larger European banks that have limited or manageable commercial real estate exposure.

In terms of the capital structure, we currently favor senior bank debt over lower Tier 2 debt and AT1 CoCos. The latter have performed well and recovered to pre-March 2023 levels, but we have become more selective in our investments in these instruments.

Aside from bank debt, we also find the fundamentals in the insurance sector favorable. Our exposure is concentrated on insurance companies with balanced business models, diversified earnings profiles, and robust capital positions. Despite the backdrop of gradually declining rates in 2024, insurers’ earnings are unlikely to be materially challenged, and most firms will maintain solid capital positions.

For insurers, we anticipate price discipline to support the sector’s top line. After two years of elevated claims inflation, the normalization of prices should contribute to the recovery in underwriting profitability. Additionally, the current high-interest rate environment remains favorable for investment income.

Looking ahead

As a credit investor, it is crucial to avoid falling into the value trap, as credits that appear cheap may have underlying reasons for their low valuation. However, we do not believe this is the case for European financials. Despite the lower growth outlook for the European economy compared to other parts of the world, the fundamentals for insurance and bank debt in Europe remain solid. In our view, current valuations still provide ample compensation for the risks associated with a slower-growth environment. Nevertheless, it is essential to recognize that not all financials are equal. As a credit investor, conducting thorough credit analysis before investing in bank and insurance debt is imperative.

Financial Institutions Bonds D EUR

- performance ytd (31-5)

- 0.75%

- Performance 3y (31-5)

- 6.98%

- morningstar (31-5)

- SFDR (31-5)

- Article 8

- Dividend Paying (31-5)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

See all articles in this series

Credit Investing opportunity

Seizing the opportunity in the credit market