Portfolio Manager

• Insight

Old World, new money: Are European equities making a comeback?

Could increasing exposure to European equities be beneficial for today’s investor? In a new paper, we examine the current landscape of European equities markets, introduce Robeco’s 3D ETF, and make the case for a European equities allocation.

Authors

Client Portfolio Manager

Top keywords

Summary

- European stocks have lagged significantly in the post-2008 US-driven bull market

- Allocating to Europe can make sense from a diversification & valuation perspective

- Our new 3D ETFs seek optimal balance between return, risk and sustainability

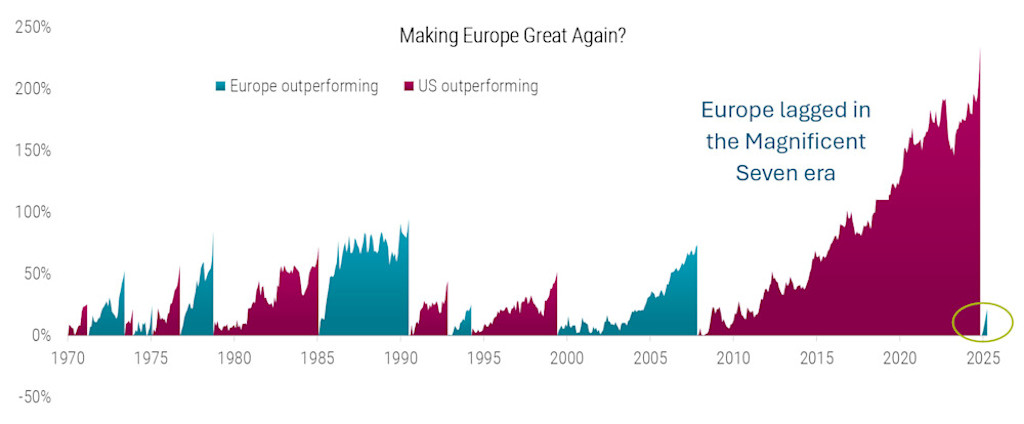

Figure 1 shows the historical ebb and flow of regional equity leadership. Since the global financial crisis, US stocks have delivered extraordinary returns. But this year marks a change. For the first time in over a decade, European equities have decisively outperformed their US peers – a potential signal that the era of US dominance has paused, if not ended.

Figure 1 I Has the extended market leadership for US equities come to an end for now?

Source: Robeco, LSEG, MSCI. The figure shows the relative performance of the MSCI USA Index versus the MSCI Europe Index. A new cycle begins after the peak of the previously outperforming market, once the previously underperforming market has outperformed by at least 20% from its preceding low. Performance is based on end-of-month total return indices in USD. The sample period spans from January 1970 to April 2025.

This figure is for illustrative purposes only and does not represent a particular investment product or strategy.

Why Europe? Three compelling reasons

Global exposure at attractive valuations

Large European stocks offer balanced, global exposure against attractive valuations. Companies in the MSCI Europe derive 60% of their revenues outside of Europe, and the index’s sector composition is more balanced than the tech-heavy S&P 500. In addition, European stocks are cheaper – from both a relative and historical perspective – than their US counterparts.Global benchmarks are now skewed

Today’s global benchmarks are no longer diversified in terms of country exposure: the MSCI ACWI has a 63% weight in US stocks versus only 17% in Western Europe – a stark contrast to 15 years ago, when the split was 40% US and 28% Europe. For investors seeking more diversified country exposure, equal-weighted indices and regional rebalancing deserve renewed attention.Europe is unloved and under-owned

Over the last ten years, active European equity strategies have seen a cumulative EUR 75 billion in outflows. Yet financial history tells us: the smaller the audience, the bigger the miracle. With sentiment at a low, new money flowing into European equities could trigger a multi-year trend reversal.

A timely entry point and a smarter way in

For investors considering a return to the Old World, Robeco offers a range of active strategies focused on European equities. Our latest addition is the 3D European Equities ETF, a forward-looking strategy designed to deliver a balanced mix of return, risk management, and sustainability integration. Priced at a competitive fee of just 0.25%, it offers investors a systematic and cost-effective way to gain exposure to European markets.

In our new paper, we detail the strategy’s design and its role within a diversified portfolio, while considering the broader investment landscape – and why it might just be Europe’s moment.

Get the latest insights

Subscribe to our newsletter for investment updates and expert analysis.