Climate Data Scientist

Keep up with the latest sustainable insights

Join our newsletter to explore the trends shaping SI.

Investors rely on data to make decisions on climate strategy, but emissions data can have smoke coming out of the ears of frustrated investors. In the third of a new series of columns taking a more light-hearted look at the issue, Robeco data scientist Thijs Markwat makes the case for paying more attention to scope 2.

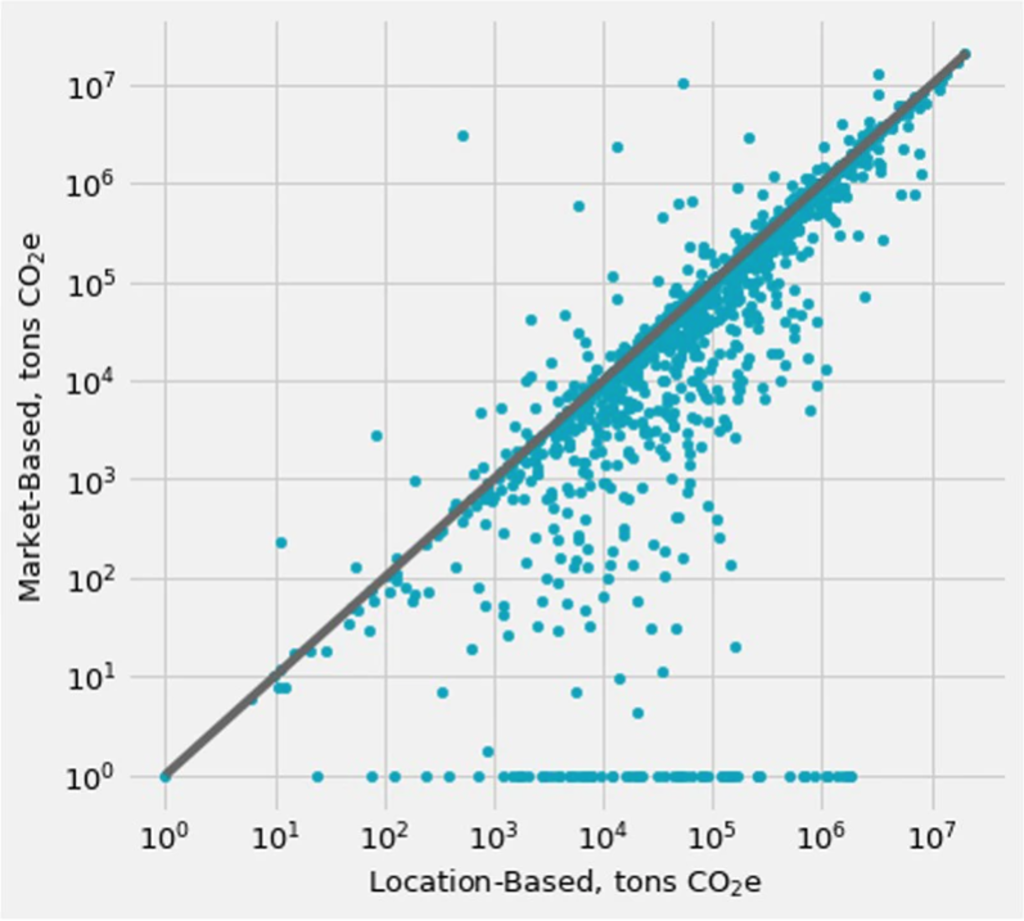

1Purchased steam, heat, or cooling are also scope 2, but for this note we focus on electricity.

2The chart shows 1 + emissions as we needed to plot zero emission values on a log scale.

Join our newsletter to explore the trends shaping SI.