Head of Conservative Equities and Chief Quant Strategist

• Insight

Strong hands needed to unlock the potential of factor investing

The average investor is not good at timing. Adverse timing can completely wipe out the returns generated by factor investing strategies. Investors with ‘strong hands’ ─ patient long-term investors with persistent style exposures ─ are much more likely to make the most of factor investing.

Authors

Summary

- Investors lose up to 2% per year due to poor timing

- ‘Weak hands’ are driven by short-termism and emotions

- ‘Strong hands’ are needed to unlock the full potential of factors

Timing investments is tough and the average investor is unfortunately not good at it. When mutual fund investors start allocating massively to a certain style, their ‘buy’ signal is often more of a ‘sell’ signal, since on average they move in at the wrong moment. The reverse is also true: when mutual fund investors start avoiding that style, this can be seen as a contrarian signal.

This collective bad timing explains most of the difference between investment returns and investor returns, sometimes referred to as the ‘behavior gap’. Investor returns take into account the timing effects and cash flows of investors. For example, when a large fund has a loss, or when a small fund has a gain, the difference between fund return and investor return can be considerable.

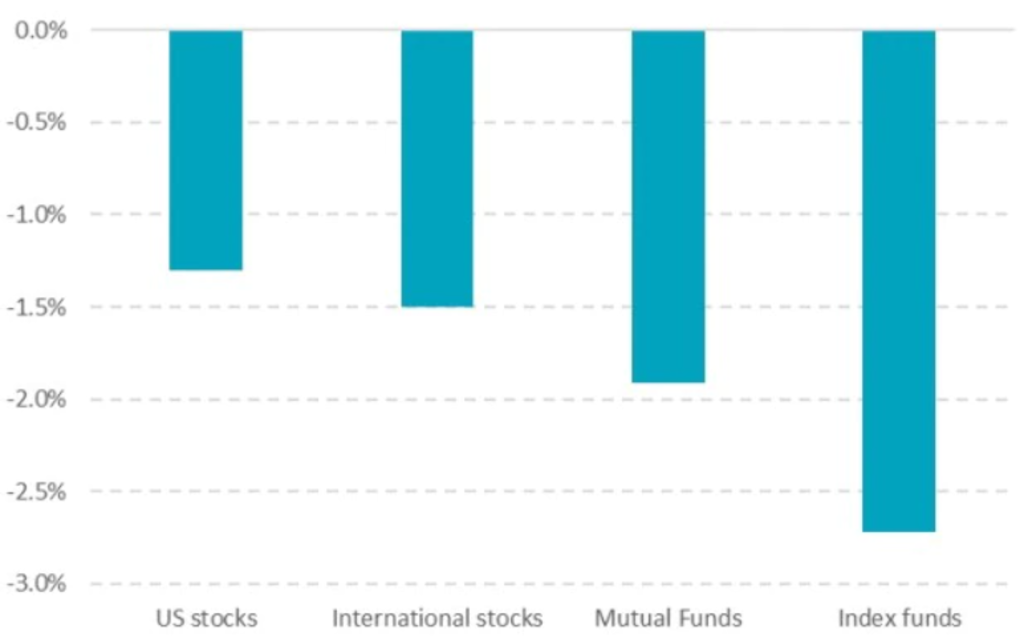

In a 2016 research paper1, Jason Hsu, Brett Myers and Ryan Whitby analyzed this interesting question using US mutual fund data, over the January 1991-June 2013 period. They found that the average mutual fund investor lagged a buy-and-hold strategy by 1.9%. This finding was persistent across different styles, varying from 1.3% for investors in value funds to 3.2% for investors in growth funds. Meanwhile, ‘passive’ investors, in market index funds, underperformed a buy-and-hold strategy by a whopping 2.7%.

What’s more, these results were all gross of fees and transaction costs. So, in practice, the gap between investor returns and fund performance is actually even larger. It is an established fact that the average mutual fund investor underperforms the index after costs, but the significant performance drag caused by poor timing is less well-known.

These findings are consistent with those reported by Ilia Dichev2, back in 2007, who showed that overall, US stock investors lag the buy-and-hold equity return by 1.3% (period 1926-2002, table 3 in the study). For international investors this figure is 1.5% (period 1973-2004, table 4). Figure 1 summarizes the findings from the literature.

Figure 1: Investor return minus investment return

Robeco Research; fund return gap from Hsu et al (2016) and stock return gap from Dichev (2007)

Having strong hands is difficult for the impatient

Patient long-term investors with persistent style exposures, in other words ‘strong hands’, are more likely to be able to harvest the factor premiums. The problem is that having such strong hands is difficult for the impatient. This usually requires years of practice.

Due to overconfidence, most investors think they have strong hands, which is by definition not possible. Everyone pays lip service to patience and a long-term vision. But these are meaningless concepts if they are not specified. It is crucial to make the investment horizon very concrete and translate ‘a long period’ into a specific number of years. The length of this horizon will depend on the risk or return objective.

Partnering is often a useful way to ensure you stick to your plans. For example, in sports, study, and work it helps if someone knows your plan and is willing to help you execute it. Many successful investors acknowledge that the biggest enemy is you. The best way to win this internal battle is to create a plan and seek allies in order to successfully execute it.

Finding the right partner might help to successfully reach long-term investment goals. In the case of factor-based investing, the first obstacle is to narrow the factors down to a limited set of the most robust and effective factor groups. This is needed since some factors will turn out to be fake.

A disciplined approach pays off and might help to avoid the average 2% booby trap. Education is key since teams change and investment horizons are often short. This continuing education fosters a successful investment culture, which leaves no room for harmful emotions or misaligned incentives. Deeper knowledge of weak hands and strong hands will help to increase humility and patience and limit harmful trading.

This is an updated version of the publication, now with the audio-paper added. Original publication is from December 2017.

Footnotes

1 J. Hsu, B. Myers and R. Whitby, ‘Timing Poorly: A Guide to Generating Poor Returns While Investing in Successful Strategies’, The Journal of Portfolio Management, 42(2), pp. 90-98.

2 I. Dichev, ‘What Are Stock Investors’ Actual Historical Returns? Evidence from Dollar-Weighted Returns’, American Economic Review, vol. 97, no. 1, March 2007 (pp. 386-401)