Objectives

Alignment with conventional benchmark returns: The solution should have a low tracking error versus the conventional benchmark, with similar return levels.

Low turnover to increase cost efficiency: This aimed to avoid active management costs and limit trading to fundamental credit risk, sustainability and tracking error considerations.

Avoiding high-risk names: All issuers in the portfolio were carefully selected based on in-depth fundamental analysis, aiming to add performance and avoid high-risk names.

The pension plan wanted to embed their specific sustainable investing objectives, with the tracking error budget mainly being used to meet these objectives:

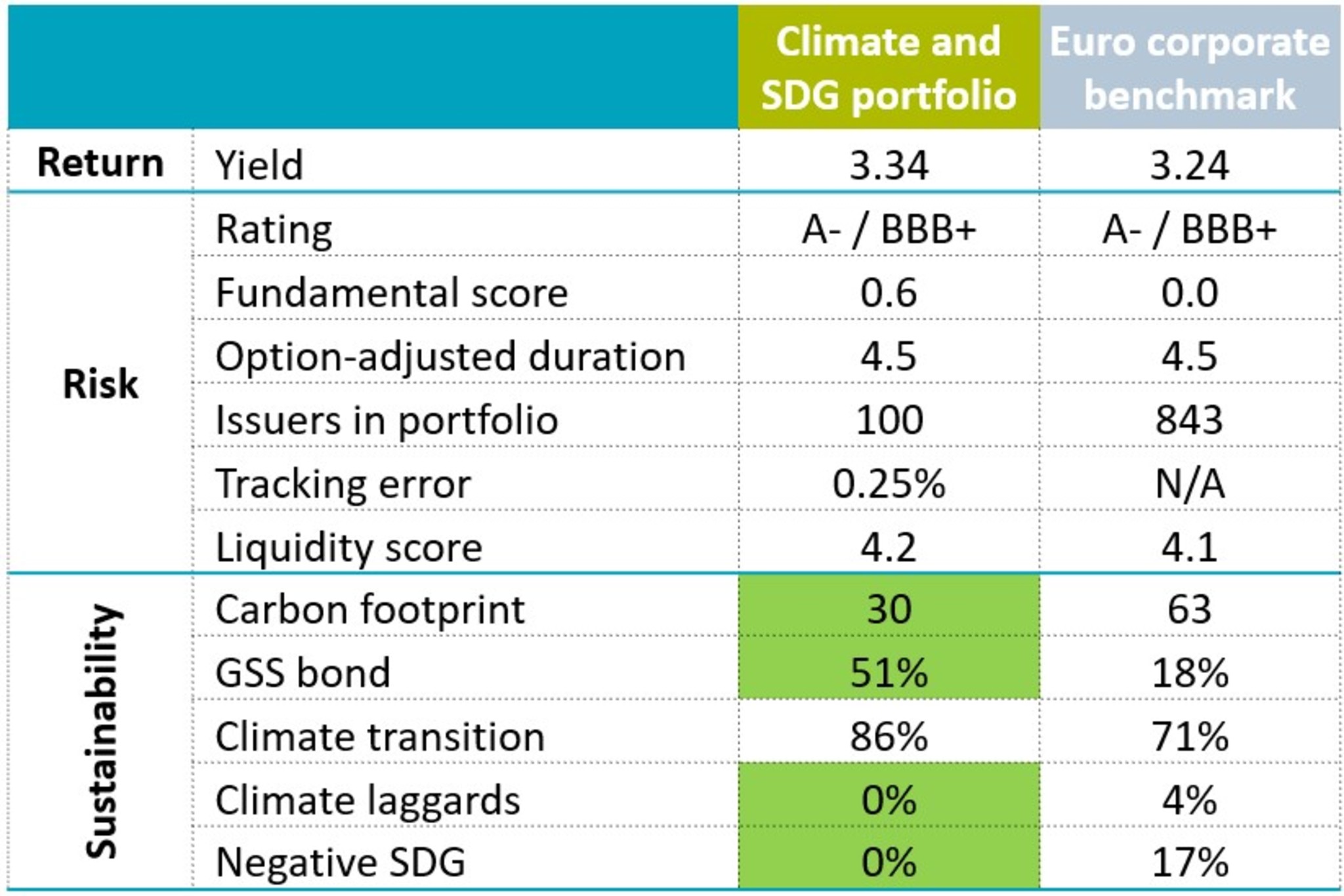

At least 50% GSS bonds: Making a material allocation to green, social and sustainable (GSS) bonds, promoting a positive environmental and social impact

CTB-aligned carbon footprint: Ensuring that the portfolio’s carbon footprint aligns with the European corporate bond Climate Transition Benchmark (CTB), supporting a low-carbon economy

Client exclusion list: Excluding specific industries or companies that do not align with the client’s ethical and environmental values

Exclusion of negative SDG scores: Only including bonds that have positive scores in Robeco’s SDG Framework to align with global sustainability objectives

No climate laggards: Excluding companies with a high carbon footprint and do not score aligned or aligning with Robeco’s Climate Traffic Light Assessment