9 questions about credit investing | Question 8

Cash rates won't last forever, prompting investors to reconsider traditional holding strategies like savings accounts, money market funds, and other short-term liquid investments. A prudent asset allocation strategy, diversifying across various asset classes according to risk tolerance and investment horizon, becomes essential. How should investors position their portfolios in response to credit markets?

Before deciding on the optimal credit allocation in our multi-asset strategies, we must first consider what asset mix is most likely to offer the best risk-adjusted returns to investors. In all walks of life, we focus on value for money, and investments should be no different. More risk-sensitive investors will want to be sufficiently compensated in return terms for every additional unit of risk taken. This optimal allocation decision has three main drivers:

Expected risk and return for each asset class

Opportunities for active management in different asset classes

The diversification benefits of combining different asset classes

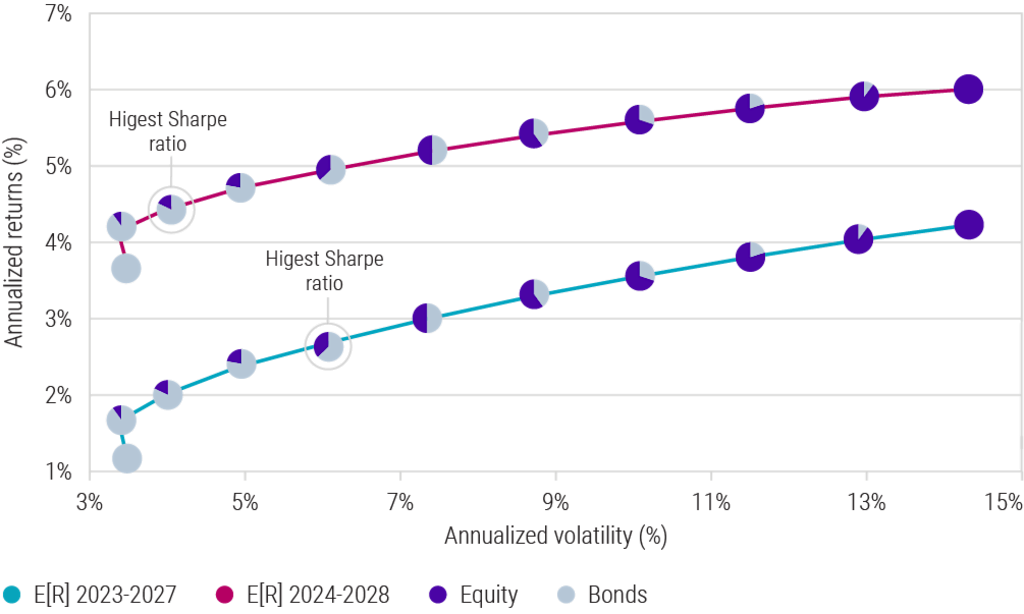

Each year, Robeco produces its 5-year Expected Returns publication for all major asset classes, considering valuations, macro scenarios and climate factors. The latest Robeco forecasts suggest that the best risk-adjusted returns over the next five years will come from a mix of 25% equity and 75% fixed income. This allocation is reflected in the bond and equity efficient frontier chart below. Another interesting observation is that this research advocates for a 20% increase in bond allocation at the expense of equities compared to last year. This in part reflects valuations for the most concentrated part of the equity markets closing in on historical peaks, and with it a more challenging upside/downside asymmetry versus credit right now. Credit spreads are well placed and not super tight and for the most part, investment grade companies should manage the refinancing risk, which for many will happen further down the track. So, for those investors looking to move from cash and back into the market, the 25% equity/75% fixed income asset allocation appears optimal.

Bond and equity efficient frontiers for Expected Returns 2023-27 vs 2024-28

Source: Robeco, as of September 2023. Note: volatility based on average historical data from October 2000 to September 2023. Equity is represented by MSCI AC World and Bonds is represented by Bloomberg Global Aggregate Corporate and Bloomberg Global Aggregate Treasury indices. In portfolio optimizations, we combine the 5-year Expected Returns with long-term steady state returns.

Opportunities for active management in different asset classes

When optimizing an asset allocation at a particular risk level within a multi-asset portfolio, we expect alpha for each active investment strategy we invest in. This reflects our conviction in the underlying investment team, culminating in a 1-5 rating based on a mix of quantitative and qualitative research. We then use that information in tandem with our view of the prospects for excess returns in each asset class. Our multi-asset strategy often operates within a finite overall risk and fee budget, necessitating a balance of these competing elements in the most efficient way possible. In our 2023 5-year Expected Returns we measured the percentage of active managers that beat their equivalent passive tracker in global credit (EUR-hedged) versus large-cap balanced US equity, the two largest asset class building blocks. The pronounced difference in the opportunity set reveals that the prospects for excess returns in global credit will positively impact the allocation size to global credit in our multi-asset strategy.

The diversification benefits of combining different asset classes

Historically mixing different asset classes has provided diversification, and with it improved risk-adjusted returns. However, there is an exception to the rule. During periods of elevated inflation, assets typically become correlated – just like we have witnessed over the past two years. However, looking forward, we expect those diversification benefits to make a comeback. We anticipate Core CPI inflation forecasts of circa 2.5%-3% for the next five years, and historically that level has supported diversification between bonds and equities. For lower-risk investors, a multi-asset portfolio with a majority allocation to bonds should stand to perform well.

Climate Global Credits DH EUR

- performance ytd (31-12)

- 4.28%

- Performance 3y (31-12)

- 3.44%

- morningstar (31-12)

- SFDR (31-12)

- Article 9

- Dividend Paying (31-12)

- No

Past performance is no guarantee of future results. The value of the investments may fluctuate. Annualized (for periods longer than one year). Performances are net of fees and based on transaction prices.

See all articles in this series

Credit Investing opportunity

Seizing the opportunity in the credit market