9 Questions about credit investing | Question 3

Historically, investors have allocated to bonds and more specifically to credits, for income and diversification against other (risky) asset classes, such as equities and commodities. However, during the 2022 market sell off, credit did not bring the portfolio diversification that investors sought. Global investment grade credit markets experienced significant drawdowns, alongside negative returns for equities. Investors began to question the diversification ability of bonds in general, and investment grade credit more specifically.

Now yields have risen, can investors rely on investment grade credit for diversification in the coming years or should they be more skeptical about its diversification merits?

To answer this question, we first need to look at how investment grade credit has performed compared to other asset classes over the last 25 years, especially in years when equities delivered a negative performance.

Equity markets (MSCI World Index) experienced negative returns in the years 2000-2002, 2008 and 2022. The sell-off in equity markets in 2001/2002 and 2008 coincided with a recession in the US and in 2000, equity markets sold off due to problems in the Technology, Media and Telecom sectors. The equity market sell-off in 2022 was the result of a fierce rate hike cycle imposed by central banks to stem the surge in inflation.

In the more challenging equity bear market of 2000-2002 global investment grade credits delivered positive returns. For example, in 2002 global equity markets declined by almost 20%, whereas global investment grade credits (Bloomberg Corporate Index USD-hedged) delivered a positive return of 14.8% and provided those investors that were holding global investment grade credits with diversification benefits.

The bear market of 2008 saw substantial drawdowns for most asset classes. Global equity markets dropped 40.7%, commodity and global high yield markets declined respectively by -46% and -27%. Global investment credit also delivered a negative return of -8.6%. However, this was a milder draw down compared to other asset classes.

The only bear market over this period in which global investment grade credits did not deliver diversification benefits was 2022, as drawdowns were -16.7%, almost as large as those in global equity markets. The sharp drawdown in global investment grade credits can be attributed to its higher duration sensitivity, which made it more vulnerable to the sharp rise in bond yields that year.

Looking back at the risk-off periods over the last 25 years we see that in most periods investment grade credit has delivered positive total returns, or in one instance (2008) delivered a milder draw down compared to equities and commodity markets, hence providing valuable diversification benefits to investors. In early August, as market volatility resurfaced in response to weaker US macro-economic data and geopolitical risks in the Middle East, investment grade credit provided diversification delivering positive returns while equity markets dropped.

Investment grade credit’s risk/return profile in a multi-asset context

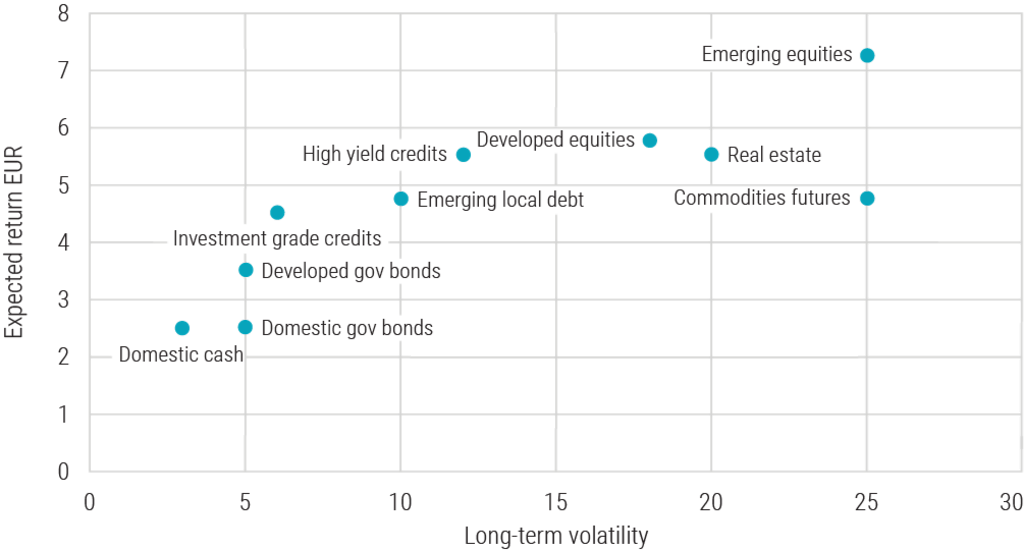

Let’s now take a more forward-looking approach to assess the diversification benefits of investment grade credits. Robeco’s multi-asset team recently published their 5-year expected return outlook where they calculate expected returns and long-term volatility for the various asset classes over the next five years. These return estimates and volatilities are based on both internal Robeco estimates and external studies. They utilize different market indices and incorporate a mix of historical data and forward-looking metrics. We have plotted the risk/return results in the figure below.

Asset class expected returns vs long-term volatility

Source: Robeco, 5-year expected returns publication. September 2023.

What becomes immediately clear from this chart is the superior risk/return profile of investment grade credit compared to other asset classes.

It has one of the lowest long-term volatility profiles, but provides higher return potential than government bonds and a long-term return potential that is not substantially lower than most riskier asset classes, with the exception of emerging market equities.

Based on this forward-looking analysis we can conclude that investment grade credit has a very appealing risk/return profile and is therefore deserving of its place in a balanced portfolio. It has the ability to substantially lower volatility, without a significant give-up in longer-term return potential.

The size of the exposure to investment grade credits in a balanced portfolio is also dependent on the short-term tactical view of the investor. If the view is that economies will see a significant slowdown or even hit a recession, then investment grade credit has the potential to outperform more riskier asset classes such as equities, commodities and even high yield, delivering the diversification benefits that investors will be seeking in such a market environment.